Last Update 28 Nov 25

Fair value Decreased 5.82%EH: Regulatory Progress Will Drive Upside As Global Demand Accelerates

The analyst consensus fair value estimate for EHang Holdings was revised downward from $23.71 to $22.33. Analysts cite a more gradual commercialization timeline and ongoing regulatory challenges affecting near-term growth projections.

Analyst Commentary

Analysts have provided updated insights following the recent revision in EHang Holdings' fair value estimate. Views remain divided on the company's near-term trajectory and long-term potential.

Bullish Takeaways

- Bullish analysts point to the enduring potential of electric vertical take-off and landing aircraft as a global trend, which positions EHang at the forefront of technological innovation.

- The company's integration into China's low-altitude economy plan is highlighted as a significant strategic advantage that could support longer-term growth.

- Despite regulatory headwinds, some expect that gradual commercialization may ultimately lead to more sustainable and disciplined expansion.

Bearish Takeaways

- Bearish analysts are cautious due to the slower pace of regulatory approvals, which continues to delay broader market entry and revenue acceleration.

- Recent industry immersion tours and discussions with management underscore a more measured commercialization phase, which may result in muted growth over the next 12 to 24 months.

- Downward revisions in price targets reflect concerns that execution risks and regulatory uncertainties could weigh on valuation in the near term.

What's in the News

- EHang conducted the first-ever urban human-carrying pilotless eVTOL flight event in Bangkok. Thailand's Civil Aviation Authority chief rode onboard as part of the AAM Sandbox Initiative, which aims to advance commercialization in Thailand. (Key Developments)

- The company completed historic point-to-point, human-carrying EH216-S eVTOL flights in Doha. This marked the first such urban operation in the Middle East and supports future commercial air taxi operations. (Key Developments)

- EHang introduced the new VT35 long-range pilotless eVTOL aircraft, expanding its urban-to-intercity offerings and securing its first platform purchase orders. (Key Developments)

- A proposed class action settlement relating to EHang ADSs is scheduled for a court hearing in January 2026. This could potentially resolve investor claims from March 2022 to November 2023. (Key Developments)

- EHang entered a global strategic partnership with China Road and Bridge Corporation. This partnership aims to boost international promotion, further aerial vehicle scenario applications, and expand EHang's operational network to Africa following debut flights. (Key Developments)

Valuation Changes

- Consensus Analyst Price Target: The fair value estimate has declined from $23.71 to $22.33, reflecting a more cautious outlook.

- Discount Rate: The discount rate decreased slightly from 8.29% to 8.21%. This indicates a modest reduction in perceived risk.

- Revenue Growth: Projected revenue growth has risen notably, from 63.41% to 71.11%.

- Net Profit Margin: The forecast net profit margin has increased from 15.47% to 16.73%.

- Future P/E: The estimated future price-to-earnings ratio has dropped significantly from 56.79x to 45.04x. This suggests expectations for improved future earnings relative to price.

Key Takeaways

- Expansion into urban air mobility and strong government partnerships enhance regulatory acceptance, infrastructure integration, and long-term revenue growth potential.

- Innovations in battery technology and a dual business model foster market differentiation, recurring revenue, and margin improvement through operational services and proven safety records.

- Heavy reliance on China, rising costs, and certification delays pose risks to growth and profitability as EHang prioritizes operational stability over aggressive expansion.

Catalysts

About EHang Holdings- Operates as an urban air mobility (UAM) technology platform company in the People’s Republic of China, East Asia, West Asia, North America, South America, West Africa, and Europe.

- The ongoing expansion of urban air mobility use cases-especially driven by government initiatives in smart cities, emergency response, and low-altitude economic ecosystems-positions EHang's autonomous aerial vehicles as foundational infrastructure, which is likely to sustain robust long-term demand and revenue growth as cities increasingly adopt eVTOL solutions.

- The company's deepening partnerships with municipal governments (such as Hefei's RMB 500 million support for the VT35 hub) and involvement in setting regulatory and safety standards enhances regulatory acceptance and ecosystem integration, supporting wider market entry, improved top-line growth, and improved long-term earnings visibility.

- Significant advancements in battery R&D-including solid-state battery integration and partnerships aimed at improving flight range, safety, and eco-friendliness-strengthen EHang's differentiation in green air mobility; this aligns with growing regulatory and societal demands for carbon reduction, which should drive both sales volumes and the ability to command higher margins due to performance leadership.

- Transitioning to a dual business model that combines eVTOL manufacturing with high-value operational services (maintenance, software, training, and operations management) is expected to unlock recurring revenue streams and meaningfully improve overall net margins and earnings resilience as the installed base scales.

- EHang's first-mover advantage in passenger-carrying pilotless eVTOL commercialization, validated by a proven safety record and accelerating order conversion, underpins sustained pricing power, competitive differentiation, and high customer switching costs, which should contribute to long-term margin expansion and earnings growth as volumes ramp.

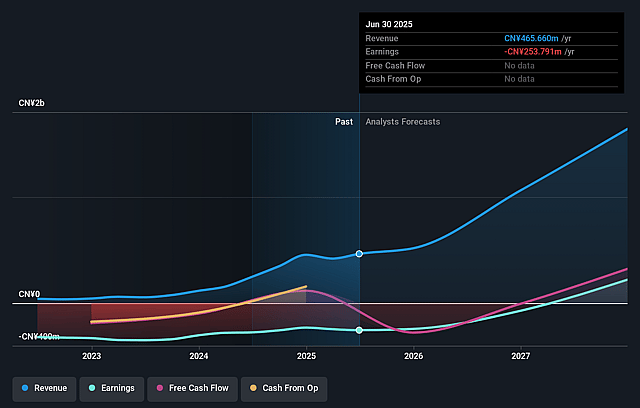

EHang Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming EHang Holdings's revenue will grow by 63.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -54.5% today to 15.5% in 3 years time.

- Analysts expect earnings to reach CN¥314.3 million (and earnings per share of CN¥3.82) by about September 2028, up from CN¥-253.8 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CN¥99.4 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 56.8x on those 2028 earnings, up from -32.2x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 34.4x.

- Analysts expect the number of shares outstanding to grow by 5.03% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.29%, as per the Simply Wall St company report.

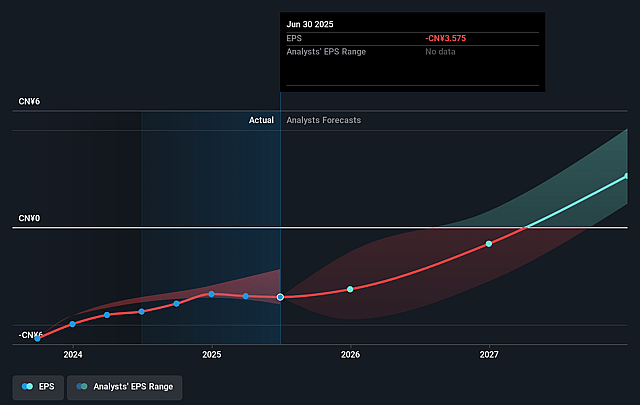

EHang Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- EHang's lowered revenue guidance for 2025 and its strategy to moderate the pace of order deliveries in favor of focusing on operational readiness and safety signal that the company is prioritizing long-term stability over short-term sales growth; this transition may lead to slower revenue growth and increases the risk that scaling will be delayed, impacting near-future top-line revenues.

- International expansion remains in early stages, with 90% of current sales and backlog concentrated in China; limited overseas certification and very modest overseas deliveries so far raise concerns about the company's ability to diversify revenue and increase its addressable market, making future earnings vulnerable to domestic regulatory or economic headwinds.

- EHang's continued high operating expenses-largely due to accelerated R&D investment and workforce expansion-are outpacing gross profit growth, which could put persistent pressure on net margins and profitability, particularly if operational ramp-up or commercial adoption is slower than anticipated.

- Heightened competition from larger, global aerospace and eVTOL players with more resources could erode EHang's technological lead, dampen pricing power, and compress both revenues and margins if multinational rivals gain certifications or market traction faster, both domestically and internationally.

- Delays or stricter standards in achieving large-scale regulatory certifications for new aircraft models, batteries, and international operations could impede commercial deployments, slow revenue recognition, and limit market expansion-exposing EHang's long-term growth to regulatory and operational execution risks.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $23.713 for EHang Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $27.77, and the most bearish reporting a price target of just $19.04.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥2.0 billion, earnings will come to CN¥314.3 million, and it would be trading on a PE ratio of 56.8x, assuming you use a discount rate of 8.3%.

- Given the current share price of $15.91, the analyst price target of $23.71 is 32.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.