Last Update 17 Jun 26

Fair value Increased 0.20%DE: Tariff Relief And Construction Strength Will Support Post Cycle Recovery Potential

Deere's analyst price target is revised modestly higher to $644.21 as analysts factor in updated agriculture fundamentals, tariff adjustments, and refined expectations for North America retail volumes and pricing.

Analyst Commentary

Recent research on Deere stock highlights a mix of optimism and caution as analysts reassess price targets, earnings drivers, and the impact of tariff changes on the company’s outlook.

Bullish Takeaways

- Bullish analysts point to Q2 results that were ahead of consensus and supported by tariff refunds as evidence that Deere is executing effectively despite a challenging backdrop in core markets, which they see as supportive of higher valuation ranges.

- Some research views Deere as well positioned for fiscal 2027 and beyond, citing an improved backdrop in Construction and Forestry and expectations for a modest growth environment as potential supports for earnings and cash flow over time.

- Updated Section 232 tariffs, with agricultural equipment rates adjusted down to 15% from 25%, are described by one major firm as an incremental positive that could add US$0.10 to US$0.15 of earnings per share in fiscal 2026, which, if realized, would modestly improve valuation metrics.

- JPMorgan’s revised model, which includes updated tariffs and North America retail volume expectations, still supports a higher price target of US$590, suggesting that even under tempered growth and pricing assumptions, Deere’s execution and balance of segments can justify constructive views.

Bearish Takeaways

- Bearish analysts and some neutral research highlight that Deere’s guidance was maintained despite an improved outlook for Construction and Forestry, which raises questions about how much of that segment’s strength can offset pressures in core agriculture when assessing valuation.

- Several firms have trimmed price targets, including cuts to the US$680 and US$685 areas, reflecting concerns that expectations for Large Ag remain key and that investor frustration around pricing trends in that segment could cap near term upside for Deere shares.

- Commentary that Deere shares may trade in a range over the coming weeks, with outcomes tied to seasonal weather and commodity developments, underscores the view that the stock’s near term path is closely linked to external factors rather than purely company specific execution.

- Wells Fargo describes the Section 232 tariff impact as net neutral for Deere, which tempers the more optimistic view that tariff relief alone could materially re rate the stock and suggests investors should be cautious about overestimating that particular tailwind.

What’s in the News for Deere

- Deere reported Q2 fiscal 2026 earnings of US$6.55 per share on US$11.78b in revenue, with a 5% year over year sales increase and US$1.773b in net income, as weakness in Production and Precision Agriculture was offset by stronger Small Agriculture & Turf and Construction & Forestry performance. Source: Q2 2026 earnings coverage.

- The company maintained fiscal 2026 net income guidance of US$4.5b to US$5.0b and described the current year as the bottom of the agricultural cycle. It also highlighted product innovation, digital solutions, inventory reductions and strong construction order backlogs. Source: Q2 2026 earnings coverage and corporate guidance.

- Deere received a US$272m tariff refund that supported recent quarterly margins, while also recovering tariffs that courts ruled were illegally collected. Management still expects around US$900m in net tariff costs for the fiscal year. Sources: Q2 2026 and Q1 CY2026 earnings coverage.

- U.S. tariff rates on imported agricultural and construction equipment were reduced from 25% to 15% through the end of 2027. Deere stock moved about 5.7% higher following the announcement, with analysts estimating a potential US$0.10 to US$0.15 earnings per share benefit. Source: tariff reduction news.

- Deere reached a settlement to resolve multidistrict “right to repair” litigation in the Northern District of Illinois, agreeing to fund a class settlement and continue providing tools, manuals and diagnostic software to support customer and third party repairs, subject to court approval. Source: legal settlement announcement.

Valuation Changes for Deere Stock

- Fair Value: The modeled fair value estimate moved slightly higher from $642.90 to $644.21.

- Discount Rate: The discount rate assumption declined modestly from 9.62% to 9.40%.

- Revenue Growth: The long-term revenue growth input was adjusted higher from 72.31% to 77.51%.

- Net Profit Margin: The profit margin assumption was kept essentially flat, remaining at 19.23%.

- Future P/E: The future P/E multiple edged slightly lower from 24.31x to 24.27x.

Key Takeaways

- Rapid adoption of advanced precision agriculture and automation tech is increasing higher-margin product sales and recurring software revenue for Deere.

- Global farm market improvements and disciplined inventory management position Deere for margin gains and accelerated earnings as agricultural demand rebounds.

- Rising tariffs, volatile demand, competitive pricing, and overreliance on incentives threaten Deere's profitability and margin sustainability amid cost pressures and market uncertainty.

Catalysts

About Deere- Engages in the manufacture and distribution of various equipment worldwide.

- Rapid adoption of Deere's precision agriculture and automation solutions (e.g., JDLink Boost, Precision Essentials bundles, See & Spray tech, and new automation features) is driving higher-value product sales and increased software engagement globally, positioning Deere to benefit from shifts toward high-efficiency, technology-enabled farming; this should lift both future revenue and net margins through higher-margin recurring software and data services.

- Global improvements in farm fundamentals outside North America-such as strong dairy profitability and crop yields in Europe, expanding acreage and profits in Brazil, and stable acreage with favorable credit in India-signal a demand recovery for advanced farm equipment, which could reaccelerate Deere's revenue and earnings as end markets inflect positively.

- Structural reductions in global inventory levels across all major product lines (e.g., 45% reduction in NA large tractor inventory, 50%+ down in Brazil) and a disciplined "build-to-retail" strategy allow Deere to respond rapidly to any upturn in demand, minimizing risk of production inefficiency and supporting margin improvement.

- Expansion and increased effectiveness of John Deere Financial, including innovative rate-buydown products for equipment purchasers even in a high-rate environment, are enabling customers to continue investing in equipment and supporting more resilient revenue streams and stable earnings in down cycles.

- Deere's continued investment in cost reductions, factory efficiency, and parts/service supports ongoing margin improvement, while announced price increases for 2026 models (2-4%) are expected to help offset tariff and input cost headwinds, supporting net margin and future earnings growth.

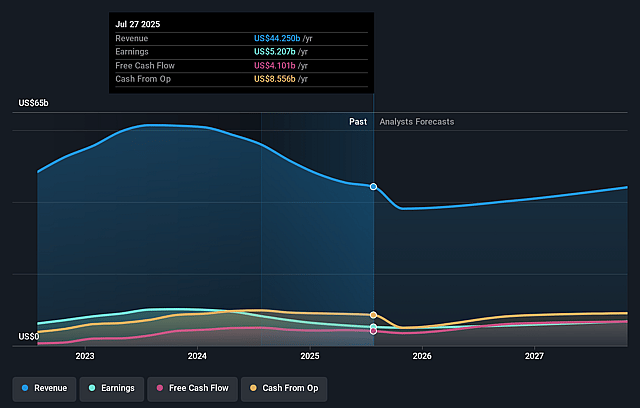

Deere Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Deere's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 10.1% today to 19.2% in 3 years time.

- Analysts expect earnings to reach $9.3 billion (and earnings per share of $36.75) by about June 2029, up from $4.8 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $10.7 billion in earnings, and the most bearish expecting $6.5 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 24.3x on those 2029 earnings, down from 33.0x today. This future PE is lower than the current PE for the US Machinery industry at 27.8x.

- Analysts expect the number of shares outstanding to decline by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.4%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Growing tariff and trade uncertainties, especially higher tariffs on Europe, India, and steel/aluminum, are materially increasing costs ($600 million forecast for FY25), which could compress operating margins and constrain future earnings if not fully offset by price realization.

- North America, Deere's largest market, is experiencing significant end-market volatility, marked by a projected 30% decline in large ag equipment sales for FY25, elevated used equipment inventories, high interest rates, and cautious sentiment-indicating risk of sustained pressure on revenue and market share if these headwinds persist.

- Aggressive competitive pricing, especially in construction and earthmoving equipment, is forcing Deere to deploy more incentives and accept negative price realization in segments; failure to reverse this trend could erode net margins and limit profitability over the long term.

- Over-reliance on incentives and financial services (e.g., John Deere Financial split rate tools and dealer pool funds) to stimulate demand in the face of high interest rates may prop up sales in the short-term but risks future revenue quality, credit losses, and margin sustainability if underlying demand does not recover.

- Growing costs from environmental, regulatory (tariff), and input inflation are requiring relentless execution on cost controls and supply chain adaptation; any misstep, inflation surprise, or inability to further reduce costs could materially impact net margins and ultimately earnings power.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $644.21 for Deere based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $759.0, and the most bearish reporting a price target of just $500.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $48.4 billion, earnings will come to $9.3 billion, and it would be trading on a PE ratio of 24.3x, assuming you use a discount rate of 9.4%.

- Given the current share price of $585.29, the analyst price target of $644.21 is 9.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Deere?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.