Last Update 04 Dec 25

Fair value Increased 36%IVVD: REVOLUTION Program Launch Will Drive Future Regulatory And Commercial Upside

Analysts have raised their price target on Invivyd to $10 from $5, citing the launch of the REVOLUTION program for VYD2311 as a key inflection point that improves the company's regulatory and commercial outlook.

Analyst Commentary

Analysts interpreting the updated price target see the REVOLUTION program as a pivotal moment for Invivyd, shifting expectations for both execution and long term growth potential.

Bullish Takeaways

- Bullish analysts view the higher price target as a reflection of improved visibility on VYD2311 as a differentiated, vaccine alternative monoclonal antibody for COVID 19 prevention, supporting a higher long term revenue trajectory.

- The formal launch of the REVOLUTION clinical program is seen as a key execution milestone that de risks the development path and could potentially accelerate timelines for regulatory submissions.

- Analysts highlight the strengthened regulatory narrative, noting that a clear program structure could support more constructive dialogue with health authorities and improve the odds of favorable labeling.

- The commercial story is seen as more compelling, with investors now assigning greater value to Invivyd’s ability to capture demand from high risk populations seeking alternatives to traditional vaccination.

Bearish Takeaways

- Bearish analysts remain cautious that, despite the program launch, clinical trial execution risk persists, and any delay or underwhelming data could quickly put pressure on the newly raised valuation.

- There is concern that the COVID 19 prevention market may be more limited or competitive than optimistic scenarios assume, which could constrain peak sales and justify only a modest premium to prior targets.

- Some observers question whether payers and healthcare systems will broadly reimburse a monoclonal antibody prevention product, creating uncertainty around pricing power and long term margin expansion.

- Investors are also reminded that Invivyd’s growth profile is still heavily concentrated in a single lead asset, leaving the story vulnerable to asset specific setbacks and future dilution if additional capital is needed.

What's in the News

- FDA cleared Invivyd's IND for VYD2311 and provided feedback to advance the REVOLUTION program, including the DECLARATION Phase 3 pivotal trial and LIBERTY head to head study versus mRNA COVID vaccines, with trial start targeted by year end 2025 and top line data mid 2026 (Key Developments).

- Invivyd completed a $124.9994 million follow on equity offering, issuing 44 million common shares and 6 million pre funded warrants at approximately $2.50 per security to support its pipeline and clinical programs (Key Developments).

- The company nominated VBY329, a potentially best in class RSV monoclonal antibody for neonates, infants, and children, aiming to move the candidate toward IND readiness in the second half of 2026 for a multibillion dollar pediatric RSV prophylaxis market (Key Developments).

- Multiple classes of Invivyd securities, including common stock, options, restricted stock units, and warrants, are subject to a lock up agreement running from November 17, 2025 to January 17, 2026, limiting insider share sales around the follow on offering period (Key Developments).

- H.C. Wainwright & Co., LLC was added as co lead underwriter on Invivyd's roughly $125 million follow on equity offering, signaling expanded banking support for the company's capital raising efforts (Key Developments).

Valuation Changes

- Fair Value: risen meaningfully, with the model-derived estimate increasing from 7.33 to 10.00. This implies a higher intrinsic valuation for Invivyd.

- Discount Rate: increased slightly from 6.98 percent to 7.01 percent, reflecting a modest uptick in perceived risk or required return.

- Revenue Growth: effectively unchanged at approximately 77.22 percent, indicating stable long term growth assumptions despite the updated program outlook.

- Net Profit Margin: essentially flat at roughly 2.72 percent, suggesting no material revision to long term profitability expectations.

- Future P/E: risen significantly from about 337.2x to 460.3x, indicating a higher multiple being applied to anticipated earnings in the valuation framework.

Key Takeaways

- Expansion of a skilled commercial team and new therapeutic programs positions Invivyd for broader market adoption, revenue growth, and reduced product concentration risk.

- Financial discipline and evolving regulatory support enhance sustainability, lower risk, and may fast-track product approvals and recurring revenue opportunities.

- Heavy reliance on a narrow COVID-19 product line, regulatory and competitive risks, and slow diversification threaten Invivyd's long-term revenue growth and financial stability.

Catalysts

About Invivyd- A biopharmaceutical company, focuses on the discovery, development, and commercialization of antibody-based solutions for infectious diseases in the United States.

- The transition to a fully internalized, best-in-class commercial sales team is driving broader adoption of PEMGARDA, as indicated by accelerating commercial metrics and institutional orders, which is likely to drive near-term revenue growth and improve efficiency, potentially expanding net margins as the commercial footprint matures.

- Invivyd’s proprietary antibody discovery platform is enabling the rapid addition of programs for RSV and measles, diversified beyond COVID-19, which positions the company to benefit from sustained global demand for innovative infectious disease therapies, supporting long-term top-line revenue growth and reducing concentration risk.

- Enhanced regulatory engagement and the shift in FDA and public health leadership toward accelerated and transparent approval pathways for critical infectious disease therapies may expedite time-to-market for Invivyd’s next-generation products, raising the probability of earlier revenue realization and improved earnings visibility.

- The global persistence and rising awareness of infectious diseases, alongside declining vaccination rates and ongoing threats such as COVID-19 and measles, ensure a large addressable patient population for Invivyd’s antibody therapeutics, underpinning recurring revenue opportunities and potential for market share expansion.

- Financial discipline, as evidenced by significant reductions in quarterly operating expenses and a focus on non-dilutive funding, improves the outlook for sustainable profitability and reduces dilution risk, which directly benefits potential future earnings and per-share value.

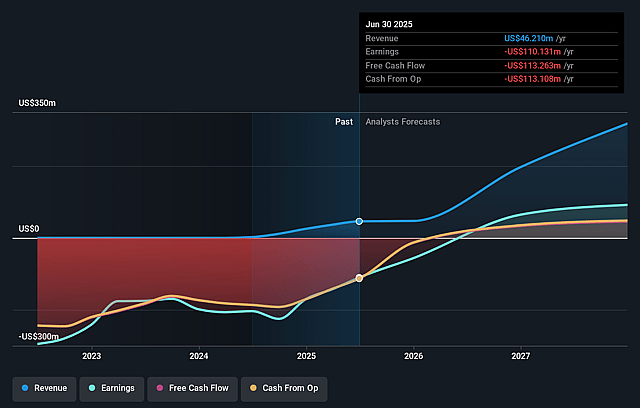

Invivyd Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Invivyd's revenue will grow by 96.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -238.3% today to 28.6% in 3 years time.

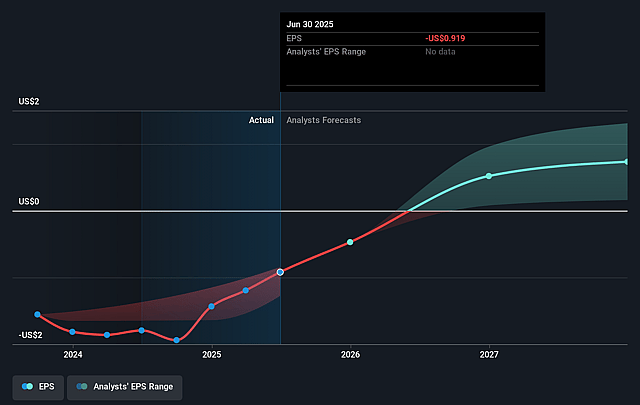

- Analysts expect earnings to reach $100.0 million (and earnings per share of $0.45) by about September 2028, up from $-110.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $158.4 million in earnings, and the most bearish expecting $19 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.2x on those 2028 earnings, up from -1.8x today. This future PE is lower than the current PE for the US Biotechs industry at 15.5x.

- Analysts expect the number of shares outstanding to grow by 0.44% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.78%, as per the Simply Wall St company report.

Invivyd Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Invivyd’s heavy current reliance on PEMGARDA and a limited COVID-19-focused product portfolio exposes it to significant product concentration risk; if demand for COVID-19 monoclonal antibodies declines due to improved public health measures, increasing vaccine uptake, or competing therapies, long-term revenues may fluctuate or shrink.

- Ongoing regulatory headwinds—exemplified by the FDA’s declining of an expanded EUA for treatment and persistent ambiguity around requirements for full product approvals—raise the risk of delayed or restricted market access for current and pipeline candidates, which could constrain revenue growth or delay margin improvement.

- Accelerating competition from large pharmaceutical companies and alternative modalities (such as evolving oral antivirals or mRNA vaccines for infectious diseases) may erode Invivyd’s ability to capture and maintain market share in both COVID-19 and future pipeline indications, negatively impacting long-term top-line growth and earnings.

- The company’s strategy of broadening into RSV and measles monoclonal antibodies remains very early stage; uncertain and potentially slow clinical development, coupled with reliance on disciplined capital deployment and outside partnerships, may limit the diversification of revenue streams and increase the risk of ongoing net losses or shareholder dilution if near-term commercial success is not achieved.

- Secular and industry trends toward increased governmental scrutiny around drug pricing and healthcare reimbursement—as well as the company’s recent price increases on PEMGARDA—may compress net profit margins and restrict Invivyd’s ability to fully capitalize on its current and future therapeutics.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $3.0 for Invivyd based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $5.0, and the most bearish reporting a price target of just $1.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $349.7 million, earnings will come to $100.0 million, and it would be trading on a PE ratio of 7.2x, assuming you use a discount rate of 6.8%.

- Given the current share price of $1.04, the analyst price target of $3.0 is 65.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.