Last Update 24 Jun 26

AZZ: Future Returns Will Depend On FY27 Cash And Acquisition Execution

Analysts raised their price targets on AZZ by $2 to $30 in recent updates, citing refreshed assumptions on discount rates, long term profit margins, and future P/E expectations to support the revised valuation range.

Analyst Commentary

Recent research updates on AZZ point to a tighter focus on how valuation, execution, and long term profit assumptions fit together, with several firms revisiting their models and adjusting price targets across a wide range.

Bullish Takeaways

- Bullish analysts raising price targets by amounts such as $15 and $30 indicate that some models are assigning higher value to AZZ under revised discount rate and P/E assumptions.

- Higher targets suggest increased confidence that AZZ can sustain profit margins closer to the upper end of prior expectations, which feeds directly into their valuation work.

- Some bullish views appear to lean on AZZ executing effectively against current plans, with the stock price seen as not fully reflecting these updated long term assumptions.

- The clustering of recent target increases signals that, within the current range, analysts see room for AZZ to better align its trading level with their refreshed valuation scenarios.

Bearish Takeaways

- Even with higher targets, bearish analysts are likely to highlight that the investment case for AZZ still depends on achieving the profit margins and P/E levels embedded in these models, which may be difficult if execution falls short.

- Caution may center on sensitivity to discount rate assumptions, with relatively small changes in these inputs having a meaningful impact on AZZ valuation outcomes.

- More conservative views may emphasize that, after recent target revisions, there is less room for error if AZZ underperforms the margin or growth profiles used in these updated frameworks.

- Some bearish perspectives could question whether the magnitude of certain target increases, such as a $30 move, runs ahead of currently observable fundamentals for AZZ.

What’s in the News for AZZ

- AZZ stock reached an all time high of US$153.04, following fourth quarter results that exceeded analysts’ expectations, a credit rating upgrade tied to debt repayment, and amendments to the credit agreement to extend maturity and reduce fees. Source: recent earnings coverage

- Analysts raised price targets on AZZ in response to strong reported demand and a positive outlook referenced in recent coverage, contributing to the share price strength. Source: recent earnings coverage

- Recent commentary highlighted mixed short term trading signals for AZZ, with one session showing a 2.71% share price decline and another closing up 1.18% at US$138.48. The stock holds a Zacks Rank #3 (Hold) and trades around 20x forward P/E at what is described as a valuation discount versus industry peers. Source: Zacks

- AZZ reiterated sales guidance of US$1.725b to US$1.775b for the fiscal year ending February 28, 2027, aligning this with confidence in its execution, operations, and market positioning. Source: Company guidance

- Management reported an active pipeline of potential bolt on acquisitions, mainly in the Metal Coatings segment with typical targets around US$15 million in sales and US$4 million to US$6 million in EBITDA, while indicating one deal in due diligence and several in discussions. Source: AZZ Q4 FY2026 earnings call

Valuation Changes for AZZ

- Fair Value: Model fair value remains unchanged at $161.67, indicating no shift in the base valuation output.

- Discount Rate: The discount rate has fallen slightly from 8.74% to 8.71%, a modest adjustment that can lift present value estimates for AZZ.

- Revenue Growth: The revenue growth assumption is effectively stable at about 5.18%, with only an immaterial change in the modeled rate.

- Net Profit Margin: The net profit margin input is essentially unchanged at roughly 11.20%, indicating no meaningful revision to AZZ profitability assumptions.

- Future P/E: The future P/E multiple has eased slightly from 28.03x to 28.01x, reflecting a very small moderation in the valuation multiple applied to AZZ earnings.

Key Takeaways

- Strategic investments in technology and infrastructure expansion are expected to boost operating efficiency, revenue growth, and elevate net margins.

- AZZ's focus on debt reduction, market share expansion, and infrastructure demand positions it for long-term value enhancement and income margin improvement.

- Adverse weather, tariff uncertainties, competition, new facility execution risks, and acquisition challenges could affect AZZ's operational reliability, margins, and market position.

Catalysts

About AZZ- Provides hot-dip galvanizing and coil coating solutions in North America.

- AZZ's new greenfield facility near St. Louis, Missouri is ramping up production, which could drive future revenue growth as it expands capacity and taps into strong local demand. This investment is expected to positively impact earnings as the facility becomes fully operational and contributes to higher sales volumes.

- AZZ plans to continue strengthening its balance sheet by paying down debt and improving capital allocation, which should reduce interest expenses and enhance net income margins over time as borrowing costs are minimized.

- The company's strategic investments in enterprise-wide technologies, such as enhancing the Digital Galvanizing System (DGS), aim to improve operating productivity and efficiency, which could lead to higher net margins through cost savings and improved operational performance.

- AZZ is actively pursuing bolt-on acquisitions and expanding market share, which are expected to drive revenue growth and operational synergies. This inorganic growth strategy, alongside organic expansion, positions the company to enhance long-term shareholder value and improve net margins.

- The anticipated continuation of infrastructure spending related to the AIIJA program and urbanization trends will likely boost demand for AZZ's services, supporting top-line growth. This sustained strong demand, especially in bridge, highway, transmission, and distribution projects, is expected to positively impact revenue.

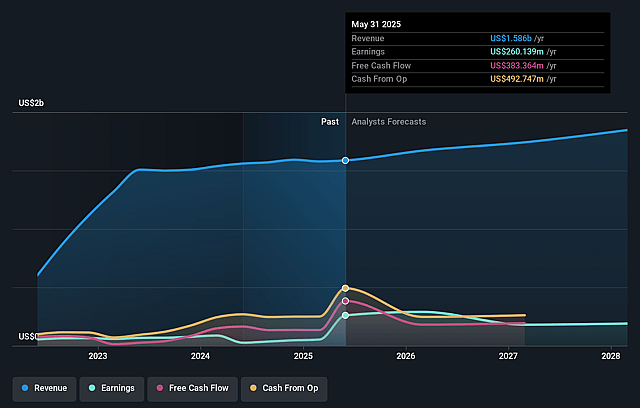

AZZ Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming AZZ's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 19.2% today to 11.2% in 3 years time.

- Analysts expect earnings to reach $215.1 million (and earnings per share of $5.41) by about June 2029, down from $317.3 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 28.5x on those 2029 earnings, up from 14.4x today. This future PE is greater than the current PE for the US Building industry at 20.8x.

- Analysts expect the number of shares outstanding to decline by 0.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.71%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The fourth quarter results were negatively impacted by adverse weather, leading to over 200 days of lost production, which could affect seasonal earnings reliability in future periods if such conditions persist.

- Uncertainty around tariffs could lead to volatility in the availability and cost of materials, which might impact margins if costs cannot be fully passed on to customers.

- There is potential for increased competition in the U.S. as reshoring trends may bring in new market participants, possibly affecting AZZ's revenue and market share.

- With the ramp-up of new facilities such as the Washington aluminum coil coating plant, there exists execution risk associated with achieving expected production efficiencies, which could impact net margins if delays or inefficiencies occur.

- While there is a focus on acquisitions, the successful integration of new businesses without disrupting current operations is necessary to maintain earnings growth, and there is always acquisition-related risk that could affect financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $161.67 for AZZ based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $200.0, and the most bearish reporting a price target of just $138.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.9 billion, earnings will come to $215.1 million, and it would be trading on a PE ratio of 28.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of $152.93, the analyst price target of $161.67 is 5.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AZZ?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.