Last Update17 Oct 25Fair value Decreased 5.46%

Shake Shack's average analyst price target has been modestly reduced, with analysts now valuing shares at approximately $125, down from about $132. Analysts cite a reset in expectations following recent margin performance and a more balanced risk/reward outlook in light of mixed same-store sales results.

Analyst Commentary

Recent Street research reveals a mix of optimism and caution among analysts regarding Shake Shack's outlook, reflecting shifts in price targets and ratings in response to recent financial performance.

Bullish Takeaways- Bullish analysts see margin improvement as a key positive, with margin and earnings upside helping offset modest sales shortfalls.

- Expectations have been reset after the recent pullback. As a result, some believe risk and reward are more balanced from current levels.

- Increased marketing investments are anticipated to bolster results in future quarters. This could drive traffic growth and support valuation.

- Several analysts have maintained or raised their price targets, citing the company’s ability to deliver strong margin performance despite softer comparable sales.

- Bearish analysts continue to highlight near-term risk to same-store sales, which could pressure top-line growth.

- There is caution around the sustainability of traffic gains. Questions remain about how much marketing and promotional spending will be necessary to achieve those results.

- Recent reductions in price targets reflect a more conservative stance on near-term execution and a recognition of ongoing volatility in comp sales.

- Some analysts have moved to more neutral ratings. This reflects hesitation around fully committing to the growth narrative until there is greater clarity on sales trends.

What's in the News

- Shake Shack will enter Hawaii for the first time in 2027, partnering with Union MAK Corporation to open a Shack on Oahu. The menu will feature locally inspired flavors and artwork, highlighting the company’s commitment to community and thoughtful expansion (Key Developments).

- Shake Shack and Maxim's Caterers Limited are expanding their partnership and plan to open 15 new locations in Vietnam by 2035, with the first debuting in 2026. The collaboration aims to reflect Vietnamese culture while maintaining Shake Shack’s signature quality and offerings (Key Developments).

Valuation Changes

- Consensus Analyst Price Target: Decreased from $132.48 to $125.24, reflecting a more cautious outlook.

- Discount Rate: Slightly decreased from 8.89 percent to 8.86 percent.

- Revenue Growth: Forecast reduced marginally from 14.80 percent to 14.67 percent annually.

- Net Profit Margin: Increased modestly from 5.39 percent to 5.41 percent.

- Future P/E: Lowered from 63.41x to 59.89x, indicating a more moderate growth expectation.

Key Takeaways

- Menu innovation, digital upgrades, and targeted marketing are fueling stronger sales growth, brand equity, and improved guest experiences, boosting margins and long-term earnings power.

- Strategic expansion into urban, international, and experiential formats, alongside operational improvements and sustainability efforts, positions Shake Shack for sustained, system-wide revenue and margin gains.

- Rising input costs, mixed traffic growth, elevated investments, operational complexity, and geographic concentration all threaten long-term profitability and sustainable growth.

Catalysts

About Shake Shack- Owns, operates, and licenses Shake Shack restaurants (Shacks) in the United States and internationally.

- Shake Shack is making significant investments in menu innovation and a robust culinary calendar, introducing new premium offerings (e.g., limited-time Dubai Shake, expanded menu for local tastes internationally) and leveraging paid media for the first time to drive higher guest frequency and attract new customers; this is poised to accelerate comp sales growth and support higher revenue and earnings power than currently captured in estimates.

- The company's strategic focus on urban expansion and accelerated domestic and international store openings-especially in untapped markets and through new formats such as drive-thru and licensed partnerships (e.g., casinos, Panama)-directly taps into growing urbanization and demand for experiential fast-casual dining, supporting long-term, system-wide revenue growth.

- Enhanced digital capabilities (including app-focused promotions and omni-channel marketing platforms) and the adoption of smarter operational tools (e.g., labor scheduling, digital kiosks, kitchen prototyping) are improving efficiency, guest experience, and speed of service, which is already translating into higher restaurant-level margins and should further boost net margins over time.

- Operational discipline via a standardized performance scorecard, leadership development, and supply chain optimization has delivered material improvements in labor productivity and cost control, helping to offset inflationary pressures on input costs-a structural margin tailwind that seems underappreciated and should help drive sustainable earnings growth.

- The shift to omnichannel sales and a culture of brand responsibility and sustainability (e.g., community engagement, eco-friendly packaging), combined with stepped-up top-of-funnel marketing, enhances Shake Shack's ability to capture incremental sales, build brand equity with younger, urban-centric consumers, and consolidate share as weaker competitors exit, supporting long-term revenue and margin expansion.

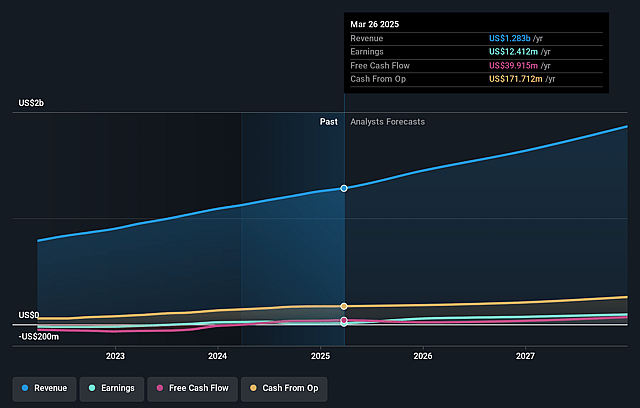

Shake Shack Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Shake Shack's revenue will grow by 14.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 5.4% in 3 years time.

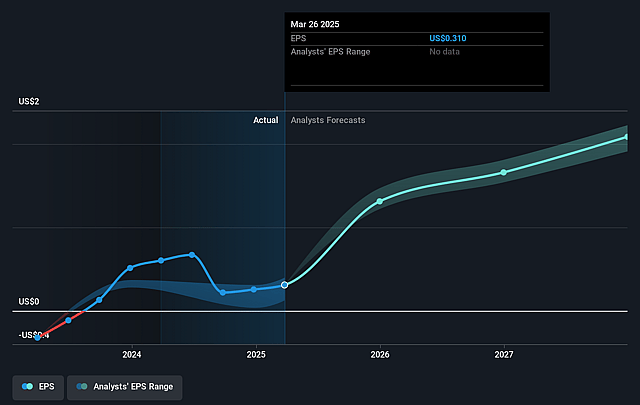

- Analysts expect earnings to reach $107.9 million (and earnings per share of $2.38) by about September 2028, up from $19.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 69.8x on those 2028 earnings, down from 199.0x today. This future PE is greater than the current PE for the US Hospitality industry at 23.9x.

- Analysts expect the number of shares outstanding to grow by 0.55% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.95%, as per the Simply Wall St company report.

Shake Shack Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising beef and commodity costs (with beef inflation in the mid

- to high-single digits) may not be fully offset by operational efficiencies or supply chain optimizations, potentially pressuring net margins and earnings over time.

- Despite positive same-store sales, traffic was down year-over-year for part of the year and only turned positive after heavy promotional activity, suggesting underlying demand or competitive pressures could limit sustainable revenue growth and impact future comp sales.

- Heavy investments in marketing, technology, and accelerated store builds increase G&A and CapEx as a percentage of revenue, which, if not matched by higher-than-expected sales and margin leverage, could weigh on free cash flow and profitability.

- Menu innovation and increased operational complexity risk slowing throughput or impacting guest experience if not perfectly executed, which could dampen frequency or lower average check, risking both revenue and restaurant-level margins.

- Geographic concentration risks remain, as New York City and the Northeast, while high-margin, are underperforming in comp contribution relative to other markets, exposing Shake Shack to regional economic or demographic downturns that could negatively impact overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $135.476 for Shake Shack based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $162.0, and the most bearish reporting a price target of just $110.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.0 billion, earnings will come to $107.9 million, and it would be trading on a PE ratio of 69.8x, assuming you use a discount rate of 8.9%.

- Given the current share price of $98.33, the analyst price target of $135.48 is 27.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.