Last Update 24 Jun 26

Fair value Increased 0.27%SCHW: AI Adoption And Platform Expansion Are Expected To Drive Future Upside

The analyst price target for Charles Schwab has been nudged higher by about $0.31 to $116.16, as analysts point to the company’s recent investor day guidance, updated financial outlook, and views on AI and client growth as support for modestly refining valuation assumptions.

Analyst Commentary

Recent research on Charles Schwab clusters around the company’s investor day, with several bullish and bearish analysts adjusting their valuation work based on updated revenue, expense, and earnings frameworks. For you as an investor, the key themes center on how credible Schwab’s growth plans look, how manageable costs appear, and how much risk AI and client cash behavior pose to the story.

Bullish Takeaways

- Bullish analysts point to Schwab’s investor day as giving clearer visibility into priorities such as organic client growth and key initiatives in advisor services, workplace services, and self-directed wealth. They view these priorities as supportive of stronger execution assumptions in their models.

- Several target increases are tied directly to the company’s updated financial outlook, including fiscal 2026 revenue and expense guidance that some analysts say sits ahead of their prior expectations. They interpret this as supportive for earnings estimates and valuation frameworks.

- One large brokerage highlights management’s commentary that AI is constructive for the business, and another states that the current bear case around AI could be unjustified. Bullish analysts therefore view AI more as a potential margin and client engagement tool than a headwind to Schwab’s cash economics.

- Some research updates reference stronger visibility into client engagement and organic growth as a reason to refine models higher. These updates include adjustments to revenue trajectories and profitability that underpin price target moves above US$120 for Charles Schwab stock.

Bearish Takeaways

- Not all analysts are raising targets. Several recent research items reference target cuts, reflecting caution around earnings power and valuation even after the investor day, and suggesting that some on the Street see risk that Schwab may fall short of the more optimistic assumptions in other models.

- Bearish analysts appear focused on prior concerns about client cash optimization and AI as potential pressures on Schwab’s net interest and sweep economics. This leads them to apply more conservative assumptions to medium term earnings estimates.

- The reaction around investor day, including a reported 2% decline in the stock on the day despite an improved revenue guide tied to net interest margin, illustrates that some investors and bearish analysts still question how durable the revenue mix will be and whether current valuation already reflects much of the expected improvement.

- Several target reductions from other firms earlier in the year, even if not fully detailed, signal that a portion of the Street continues to factor in execution risk around cost control, balance sheet mix, and the timing of any improvement in earnings. This, in turn, tempers the overall upside case for Charles Schwab.

What’s in the News for Charles Schwab

- Charles Schwab reported record core net new assets of US$49.9b in May 2026, a 43% year over year increase, with total client assets at US$13.14t and 461,000 new brokerage accounts opened, according to company disclosures.

- The company highlighted expanded trading and platform features, including nearly 24/7 cryptocurrency futures trading on thinkorswim, broader fractional share trading with a US$1 minimum, and new AI driven tools for traders and advisors, based on recent product announcements.

- Charles Schwab announced fee cuts on four equity index ETFs to 0.03% operating expense ratios, reinforcing its low cost positioning in U.S. and international equity and emerging markets ETF offerings, according to Schwab Asset Management.

- Schwab is partnering with Cboe Global Markets to roll out binary options tied to the S&P 500, giving clients access to yes or no style contracts on index levels and extending the firm’s listed options toolkit, according to recent news reports.

- The company continues to adjust its capital structure, including the planned redemption of all outstanding Series I preferred stock depositary shares at US$1,000 per share, as outlined in its latest capital actions.

Valuation Changes for Charles Schwab

- Fair Value: The model fair value estimate for Charles Schwab has risen slightly from $115.85 to $116.16.

- Discount Rate: The discount rate has moved marginally lower from 8.60% to about 8.55%, indicating a small adjustment in perceived risk or required return assumptions.

- Revenue Growth: The projected revenue growth rate remains effectively unchanged at around 9.15%.

- Net Profit Margin: The modeled net profit margin stays essentially flat at about 40.15%.

- Future P/E: The future P/E assumption has risen slightly from 17.52x to 17.54x, signaling a very modest change in how Charles Schwab’s earnings are being valued in the model.

Key Takeaways

- Expanding client base and digital adoption are driving sustained asset growth, deeper client engagement, and increasingly diversified revenue streams.

- Operational efficiencies, innovative product launches, and industry scale are enhancing margins, competitive position, and long-term earnings resilience.

- Rising competition, technology investments, regulatory pressures, interest rate exposure, and shifting client demographics pose challenges to Schwab's long-term profitability and organic growth.

Catalysts

About Charles Schwab- Operates as a savings and loan holding company that provides wealth management, securities brokerage, banking, asset management, custody, and financial advisory services in the United States and internationally.

- Continued robust growth in U.S. household wealth and generational wealth transfer is expanding Schwab's addressable client base, as evidenced by accelerated net new asset (NNA) growth (up 46% YoY in June) and strong new account openings, which are likely to support persistent AUM and revenue growth over the long term.

- Increasing adoption of digital platforms, self-directed investing, and demand from younger demographics-over 60% of new-to-firm clients are under 40-are leading to deepening client engagement and expansion of Schwab's solutions across wealth management, lending, and trading, supporting higher fee income and diversified revenue streams.

- Success in cross-selling advisory, banking, and lending products to existing and newly integrated Ameritrade clients is driving higher engagement, utilization, and non-transactional fee income, with pledged asset line originations and bank lending balances both up over 100% YoY, supporting improved net margins and earnings durability.

- Ongoing digital transformation and operational enhancements (e.g., AI-powered efficiency and automation) are expected to sustainably reduce cost-to-serve and improve client experience at scale, underpinning long-term operating margin expansion.

- Schwab's industry-leading scale, continued penetration with independent advisors via its custody platform, and launch of new offerings (such as retail alternatives and digital asset products) are expected to enhance recurring fee-based revenues and cement competitive positioning, supporting earnings resilience and long-term profitability.

Charles Schwab Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

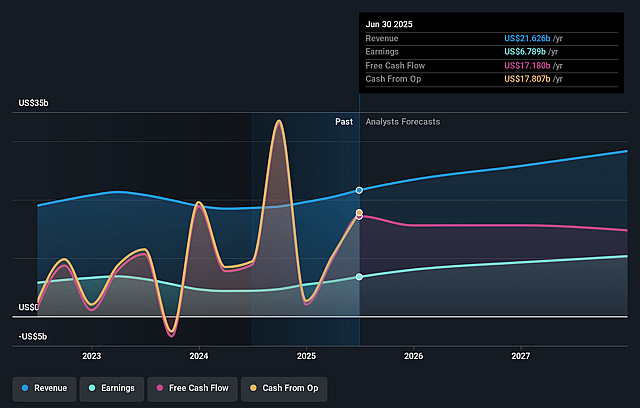

- Analysts are assuming Charles Schwab's revenue will grow by 9.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 36.4% today to 40.1% in 3 years time.

- Analysts expect earnings to reach $12.9 billion (and earnings per share of $7.73) by about June 2029, up from $9.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.5x on those 2029 earnings, down from 18.0x today. This future PE is lower than the current PE for the US Capital Markets industry at 40.5x.

- Analysts expect the number of shares outstanding to decline by 4.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.55%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition from low-cost and digital-first brokerage platforms such as Robinhood and Webull, coupled with ongoing industry fee compression and the rise of passive investing, may erode Schwab's ability to capture trading-related revenues and threaten long-term net margin expansion.

- Schwab's increasing investments in technology, digital infrastructure (including artificial intelligence), and new product capabilities to keep pace with fintech disruption could drive up expenses faster than revenue growth, putting sustained pressure on net margins even as the firm touts near-term operating leverage.

- Heavy reliance on net interest income-bolstered recently by high interest rates and favorable client cash trends-exposes Schwab to significant earnings volatility in the event of adverse shifts in the interest rate environment or yield curve inversion, despite recently enhanced hedging programs.

- Regulatory risks remain elevated, especially regarding Schwab's cash management practices and future reforms around payment for order flow, which could increase compliance costs or restrict lucrative practices, thereby directly impacting profitability and operating margins.

- Demographic shifts, such as the slower accumulation of assets among younger generations or preferences for alternative digital platforms for investment, may moderate Schwab's long-term organic asset growth rate and limit the expansion of assets under management, thereby constraining revenue and earnings growth in the years ahead.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $116.16 for Charles Schwab based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $137.0, and the most bearish reporting a price target of just $84.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $32.3 billion, earnings will come to $12.9 billion, and it would be trading on a PE ratio of 17.5x, assuming you use a discount rate of 8.5%.

- Given the current share price of $93.17, the analyst price target of $116.16 is 19.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Charles Schwab?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.