Last Update 16 Jun 26

Fair value Decreased 6.99%TTD: Future Upside Will Depend On Fox Roku And Publicis Partnerships

The Trade Desk price target has been revised modestly lower to $24.45 from $26.29 as analysts factor in recent cuts from multiple firms, a mix of cautious views on growth and margins, and ongoing debate around competition, agency relationships, and the impact of key partnerships with Fox, Roku, and Publicis.

Analyst Commentary

Analysts remain divided on Trade Desk stock, with recent commentary highlighting both supportive factors around key partnerships and agency relationships, and pointed concerns about competition, take-rate pressure, and leadership changes. For you as an investor, the debate centers on how these factors could influence execution quality and the valuation investors are willing to pay.

Bullish Takeaways

- Bullish analysts view Trade Desk's partnerships with Fox and Roku as central to demand flows for connected TV inventory. They see this as important for sustaining scale and keeping the stock's premium multiple in play.

- Some see Trade Desk as a meaningful technology partner for Fox, with expectations that the role could continue within the combined Fox and Roku entity. They argue that this supports the case that Trade Desk remains embedded in major TV and streaming workflows.

- The recent joint statement with Publicis is seen by bullish analysts as a clearing event after a period of paused ad spend. They interpret this as a positive for Trade Desk's agency relationships and revenue visibility.

- Supportive research commentary around earlier agency audits has framed Trade Desk as gaining negotiating leverage with large holding companies. Bullish analysts argue that this can help defend pricing and justify higher long term expectations within current targets.

Bearish Takeaways

- Bearish analysts focus on competition from large media and commerce platforms, highlighting that some programmatic buying tools are offered at zero cost. They argue that this could pressure Trade Desk's roughly 20% take-rate and compress margins over time.

- Some research argues that consensus expectations need to be reset lower to reflect a "new reality" of slower gross spending growth and lower take-rate. In their view, this supports lower target prices and a less generous valuation multiple.

- The exit of the Chief Revenue Officer after seven months, with no immediate plan to backfill the role, has raised questions among more cautious analysts about leadership stability in the commercial organization and execution risk under the current management structure.

- The cluster of target cuts and downgrades from multiple firms signals that a portion of the Street is reassessing Trade Desk's competitive position and growth outlook. Bearish analysts argue that this may cap upside until there is clearer evidence of reaccelerating demand or improved pricing power.

What’s in the News for The Trade Desk

- The Trade Desk reported Q1 2026 revenue of US$688.9m, which modestly beat analyst expectations. Adjusted EPS of US$0.28 came in below the US$0.32 consensus, and Q2 revenue guidance of at least US$750m was below Wall Street forecasts. Management cited macro pressures in CPG and autos and highlighted continued spend on AI, retail media, and international expansion (source: earnings coverage).

- The Trade Desk stock moved sharply lower, with shares reported to be trading near eight year lows after a year to date decline of about 44%. The Q1 earnings reaction saw the stock fall between 13% and 16% in after hours trading, alongside analyst downgrades and target cuts from firms including HSBC, Oppenheimer, William Blair, KeyBanc, and others (source: market and analyst commentary).

- Publicis and The Trade Desk have settled their months long dispute over ad tech fees, with Publicis again recommending The Trade Desk’s platform to clients. This followed earlier tensions around audits and fee stacking that had weighed on the relationship and on investor sentiment (sources: Publicis dispute articles, Ad Age).

- The Trade Desk has seen executive turnover and governance headlines, including the departure of multiple senior leaders such as several CFOs and the Chief Revenue Officer. The company announced the appointment of Nate Olmstead as CFO effective July 9, 2026, and a separate investigation by Halper Sadeh LLC into whether certain officers and directors may have breached fiduciary duties to shareholders (sources: executive turnover reports, governance inquiry).

- Alongside headwinds, The Trade Desk continues to announce new partnerships and integrations. These include agreements with Agoda in APAC travel media, DramaBox for short drama content, and retail media integrations with Pacvue and Skai, which expand how advertisers can use The Trade Desk’s platform across connected TV, retail media, and other channels (sources: partnership and client announcement releases).

Valuation Changes for Trade Desk Stock

- Fair Value: revised modestly lower from $26.29 to $24.45 per share, reflecting slightly more conservative inputs.

- Discount Rate: effectively unchanged at 7.11%, indicating no material shift in the assumed risk profile.

- Revenue Growth: trimmed slightly from 9.21% to 8.87%, pointing to a more cautious view on the pace of future sales expansion for The Trade Desk.

- Net Profit Margin: eased from 16.92% to 16.44%, suggesting a small adjustment to expected profitability levels.

- Future P/E: reduced from 20.29x to 19.89x, implying a slightly lower multiple on projected earnings for The Trade Desk stock.

Key Takeaways

- Trade Desk benefits from the shift toward connected TV and data-driven, measurable advertising, leveraging strong partner relationships and advanced AI platforms for higher growth and margins.

- Global and channel expansion, along with a focus on transparency and independence, position Trade Desk to gain market share as industry trends favor open, objective platforms.

- Heavy reliance on large clients, competition from walled gardens, dependence on CTV, high innovation costs, and limited geographic diversification create significant growth and earnings risks.

Catalysts

About Trade Desk- Operates as a technology company in the United States and internationally.

- The continued rapid shift of ad spend from linear TV to connected TV (CTV) is driving significantly faster growth for Trade Desk's highest-margin channel; deepened relationships with leading CTV and streaming content partners (Disney, Netflix, Roku, LG, etc.) position Trade Desk to capture an outsized share of the expanding premium digital video ad market, which should accelerate revenue and earnings growth as CTV penetration increases globally.

- There is rising demand among brands and agencies for data-driven, measurable advertising with transparent ROI, and Trade Desk's platform (especially with advanced AI/ML features in Kokai and partnerships in retail media and measurement) is uniquely positioned to take share as advertisers prioritize analytics, measurable outcomes, and performance over brand-based, IO-driven spend; this should structurally support revenue growth and improve gross margin as advertisers migrate spend for higher ROI.

- The full rollout and high adoption of the new AI-powered Kokai platform, including new tools like Deal Desk and supply chain innovation (OpenPath, Sincera integration), is already leading to >20% better campaign performance and causing existing clients to increase spend at a much faster rate; as the remaining clients transition and the product matures, this should drive step function increases in platform efficiency, gross margin, and average revenue per client.

- Trade Desk is still early in its global expansion and its push into nontraditional channels (retail media, digital out-of-home, digital audio), with international growth outpacing North America and new partnerships accelerating; this geographic and channel diversification expands TAM and reduces concentration risk, providing strong multi-year support for top-line revenue growth.

- The growing regulatory, advertiser, and consumer push for transparency, privacy, and independence-combined with the pullback of Google and Facebook from open Internet programmatic and increased scrutiny of walled gardens-favor independent, objective platforms like Trade Desk. This competitive positioning is driving a structural shift of ad budgets to Trade Desk, which should translate into durable revenue and margin expansion over the long term.

Trade Desk Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Trade Desk's revenue will grow by 8.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.6% today to 16.4% in 3 years time.

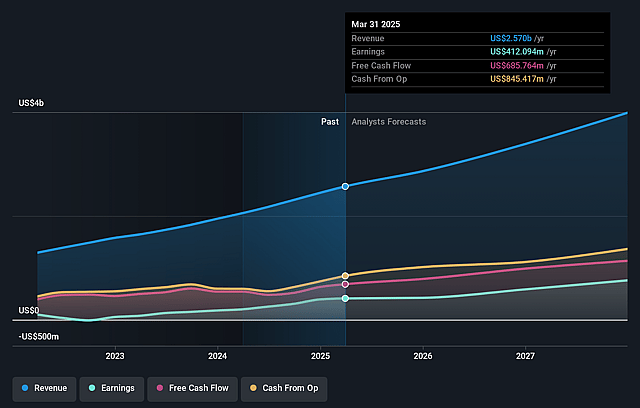

- Analysts expect earnings to reach $629.8 million (and earnings per share of $1.36) by about June 2029, up from $432.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $855.8 million in earnings, and the most bearish expecting $334.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.9x on those 2029 earnings, down from 20.9x today. This future PE is lower than the current PE for the US Media industry at 25.4x.

- Analysts expect the number of shares outstanding to decline by 3.85% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's exceptionally high reliance on large, global brands and enterprises exposes it to concentrated revenue risk; ongoing macro headwinds such as tariffs, inflation, and volatility in the auto and CPG sectors could lead to cuts in ad spend from these clients, materially impacting near-term and potentially long-term revenue growth and earnings stability.

- Despite a bullish narrative around the open Internet, Trade Desk is facing a persistent risk that walled gardens (e.g., Meta, Amazon, Google) continue to take digital ad market share at a faster pace due to their control of inventory, integrated data, and simplified measurement, limiting Trade Desk's share gains and dampening overall revenue growth prospects.

- While CTV is highlighted as the fastest-growing segment, Trade Desk's substantial dependence on CTV as a growth driver creates exposure to any future saturation, competitive disruption, or cyclical swings in streaming ad inventory, which could lead to earnings volatility and slow overall top-line growth.

- Although management emphasizes innovation in AI and supply chain transparency (e.g., Kokai, OpenPath, Deal Desk), the escalating industry-wide costs to develop and maintain cutting-edge AI-driven solutions may compress operational margins if revenue growth and pricing power do not keep pace.

- Trade Desk's current customer mix is heavily skewed toward North America (~86% of spend), indicating long-term geographic concentration and limited international scale; failure to accelerate global expansion could constrain addressable market growth and leave revenues vulnerable to North American economic cycles.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $24.45 for Trade Desk based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $38.0, and the most bearish reporting a price target of just $11.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.8 billion, earnings will come to $629.8 million, and it would be trading on a PE ratio of 19.9x, assuming you use a discount rate of 7.1%.

- Given the current share price of $19.27, the analyst price target of $24.45 is 21.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Trade Desk?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.