Last Update 20 Mar 26

Fair value Increased 0.96%The Post-Earnings Tantrum, The $6B "Dilution" Myth, and The Unstoppable Neocloud

G'day fellow investors. The post-earnings reaction to IREN is textbook volatility: shares tanked on no new hyperscaler announcements and an EPS miss from the mining-heavy Q4 P&L.

But if you’re panicking over a backward-looking, non-cash accounting loss driven by a transition from ASICs to GPUs, you are missing the forest for the trees. Algorithms and surface-level analysts are still pricing IREN as a legacy Bitcoin miner.

Let's dismantle the panic, look at the reality of the recent $6B ATM announcement, and review why this period of choppiness is nothing to be worried about in the long term.

The Elephant in the Room: Misunderstanding the $6B ATM

The biggest boogeyman spooking retail recently has been the new $6 billion ATM (At-The-Market) offering.

Don’t get me wrong; a $6b ATM looks ridiculous relative to IREN’s current market cap of ~$13.5b. If they tapped the entire amount at today’s levels, the share count could increase by >40%. But that’s a massive “IF”, and most people are treating it like a certainty.

Let’s apply some logic. Why would IREN need to tap this ATM today? They don’t. They are fully funded for the Microsoft deal, having raised over $3b through converts, ~$1.93b of prepayments, and secured $3.6b of GPU financing at an incredible <6% interest rate. They don’t need a single additional dollar to execute the MSFT buildout.

Okay, what about the new ~$3.5b GPU order for 50k B300 units? First, those costs come due gradually through H2, on terms that are 30 days post-shipment. Second, management explicitly stated these will be financed primarily through the same sources they’ve used over the past quarters: prepayments, converts, and GPU financing.

So what’s the actual purpose of this $6b ATM? It is primarily a backstop. It establishes ultimate confidence for prospective hyperscalers that IREN can deliver on massive, multi-gigawatt deployments, strengthening their negotiating position by eliminating any doubts around capital availability.

So will IREN tap it eventually? Almost certainly at some point, but likely when the share price is materially higher. Net dilution from this ATM will most likely come in well below 20%, and could even be closer to ~8–12% (or less) if management stays conservative. Relative to the growth opportunity in sight, that’s a remarkably small price to pay.

Competition Heating Up: The Structural Moat (IREN vs. NBIS)

Competition is undeniably heating up across the sector (as seen with recent deals like NBIS / Meta), but it's crucial to distinguish between real structural profits and empty revenue hype.

https://www.cnbc.com/2026/03/16/meta-nebius-ai-infrastructure.html

Take Nebius (NBIS), for example. NBIS is bleeding cash structurally: gross expenses and depreciation consumed 110% of their quarterly revenues ($249.2m costs vs $227.7m revenue). Even adjusting their aggressive 4-year depreciation to an industry-standard 5 years, costs still eat 93.5% of revenue. These aren't one-off hits, they're structural costs that scale directly with revenue growth. You can't "grow out" of GPU depreciation or gross expenses; they stick like glue. Worse, NBIS allocates its pipeline to low-margin "bare metal" hyperscaler deals, commoditised bulk compute with zero pricing power. They have no moat and no path to profits.

Contrast this with IREN. The full hyperscaler contract transparency unlocks precise, bankable modeling. For the Microsoft deal, management discloses everything: $9.7B total value, $1.94B ARR, 85% EBITDA margins, $1.93B prepays, and sub-6% GPU debt terms. There is no black box. This visibility confirms IREN prints structural profits as a neo-hyperscaler (scaling to billions in net income), while peers like NBIS chase ARR hype with costs eating their revenue. IREN is the profitable one today.

Execution: The April Microsoft Deadline & Sweetwater

While Wall Street cries over EPS and potential dilution, the real story is operational execution.

IREN's Horizon 1-4 construction remains entirely on track to meet Microsoft's GPU deployment timelines. We are fast approaching the critical April/Q2 window where these clusters will begin coming online. At the same time, Sweetwater 1 (1,400 MW) remains on track to connect to the grid in Q2. Civil works for liquid-cooled data centers are already underway.

IREN is actively transforming its 810MW of operating data centers into a revenue engine that targets $3.4 billion in AI Cloud ARR by the end of CY26.

The Math: Wall Street’s Broken Spreadsheets

To understand how fundamentally mispriced this stock is, look no further than the valuation models. My Fair Value estimate on Simply Wall St remains at $95 per share, indicating the stock is 56% undervalued.

But here is the incredible part about that valuation: it is based on an ultra-conservative base case.

- The "Base Case" Model: To arrive at the $95.75 Fair Value, the valuator assumes IREN hits $8.7B in revenue and $2.9B in earnings by the year 2031 (representing a 63% p.a. growth rate), with a 10% discount rate, 33% profit margin, and a future PE of 25x.

- The Realistic Upside: However, based on the ramp of Childress, BC, and Sweetwater 1, IREN could very well hit $8.3B in revenue by 2027 and $12.7B by 2028.

Even if we assume it takes them 5 full years to reach $8.7B in revenue, the Fair Value still spits out $95.75. If they execute anywhere near my more bullish 2028 estimates, the upside is almost incalculable...

Risks

Dilution risk

While I remain highly convicted, we have to remain objective. If I am wrong and management taps into that $6B ATM sooner and heavier than expected, it will definitively impact the share price in the short-to-medium term. Ongoing dilution is a legitimate long-term risk for this stock. However, in an aggressive land grab for AI infrastructure, this capital is exactly what allows the company to keep scaling, secure massive power blocks, and capture market share while peers stall. It is a calculated tradeoff. This is why we've seen the more short term oriented investors and traders locking in profits in the past weeks.

Macro Uncertainty & The Energy Crisis

We can't analyse a power-hungry infrastructure play without addressing the macro environment. With the escalating war in Iran and the broader Middle East, the threat of a severe global energy crisis is very real. While IREN has deeply advantaged, contracted power, a prolonged structural spike in energy markets could impact underlying grid costs and temporarily squeeze operational profitability. Energy is their primary input, and global shocks matter.

Embracing the Volatility

Between the ATM headline fears, the anticipation of the next hyperscaler deal, and severe macro/geopolitical instability, the rest of this year is guaranteed to be highly volatile. But volatility is the price of admission for multi-bagger returns. If macro fears drag the broader market down and create strong dips in IREN's share price, I won't be panicking. Instead, I’ll be ready to buy more.

The Takeaway

IREN’s lead in secured power capacity continues to widen, punctuated by their massive new 1.6GW site in Oklahoma. Over time, the latent value of this >4.5GW portfolio will become obvious, even if it doesn't feel that way today amid the post-earnings volatility.

With Sweetwater energising in just a couple of months, it’s likely that IREN will sign a new hyperscaler deal in the next 3-6 months. When that happens, expect a massive re-rate as Wall Street scrambles to upgrade their idiotic projections.

Still holding, ignoring short-term noise, focused on the long term.

A Note to New Readers:

Welcome. What you are about to read is my original narrative for IREN, first published in September 2024.

I have left it completely unchanged.

When I wrote this, I viewed IREN as a best-in-class Bitcoin miner, and I was quite skeptical of its "pivot" to AI. You'll see I even called it a "PR effort." I was focused on mining efficiency, energy contracts, and Bitcoin cycles.

I was wrong.

Over the past year, that "PR effort" proved to be the single most important, high-conviction part of the thesis. I watched IREN's management execute relentlessly, moving light-years ahead of its mining competitors. Many of them (like WULF, RIOT and CIFR) have only woken up to the AI transition in the last few months, while others still haven't even committed to buying GPUs (CLSK).

I invite you to read this original narrative to understand my starting point. Then, read the updates that follow to see the journey of how this company proved its skeptics wrong and became a core AI infrastructure play.

-----------------------------------------------------------------------------------------------------------------------------------

"Investing in a bitcoin miner?! How dare you!"

Summary

- IREN owns and operates 4 Bitcoin mining sites in North America, powered by 100% renewable energy, leveraging 'stranded energy' from hydro and solar power plants.

- IREN's goal is to capitalise on excess renewable energy and support energy networks. Bitcoin mining is just an effective way to do so.

- The company is also exploring HPC and AI services to diversify revenue, with initial successes but still early in development.

- IREN stands out among other miners for its energy efficiency. It aims to improve it further to 16 J/TH by deploying a new fleet of Bitmain S21 PRO miners this year.

- Unlike competitors, IREN sells 100% of its mined Bitcoin daily, ensuring better cash flow management.

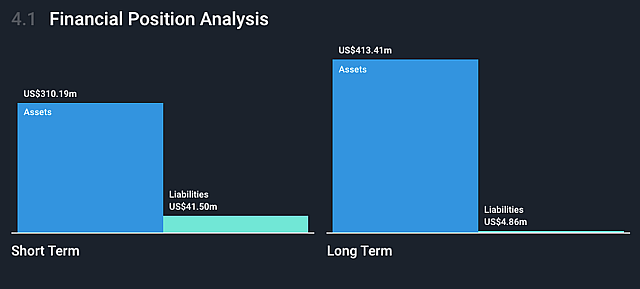

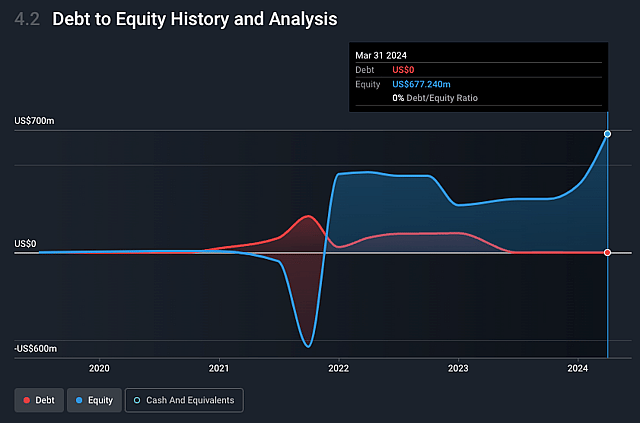

- The company is in good shape financially after large share dilutions, holding $425.3 million in cash reserves, has no debt, and became profitable in Q1 2024 with $8.6 million net profit.

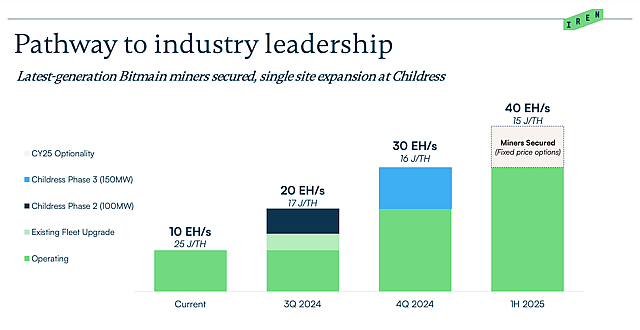

- IREN has recently expanded its mining capacity to 10 EH/s, 2 months earlier than expected. It's planning to increase it to 30 EH/s by the end of the year, with further potential growth to 40 EH/s in 2025.

- Estimated fair value per share is $16, with significant upside potential, though dependent on Bitcoin price increases and successful strategic execution.

The company

IREN is an Australian Bitcoin miner powered by 100% renewable energy. It owns and operates 4 sites in North America, strategically located next to hydro and solar power plants for key energy partnerships.

- Canal Flats, British Columbia (Canada) 30MW

- Childress County, Texas (USA) reacently increased to 750MW operating capacity 24th July 2024 update

- Mackenzie, British Columbia (Canada) 80MW

- Prince George, British Columbia (Canada) 50MW

The company was founded by two Australian brothers, Dan and Will Roberts. Dan’s experience lies in building wind and solar farms across Europe and Australia at Macquarie Bank and Palisade Investment Partners, while Will’s experience is in energy infrastructure financing at Macquarie Bank, as well as co-founding the bank's digital assets team in 2018.

The two brothers combined their expertise in Bitcoin, energy, and infrastructure finance to found IREN, with the intent to capitalise on excess renewable energy and support energy networks.

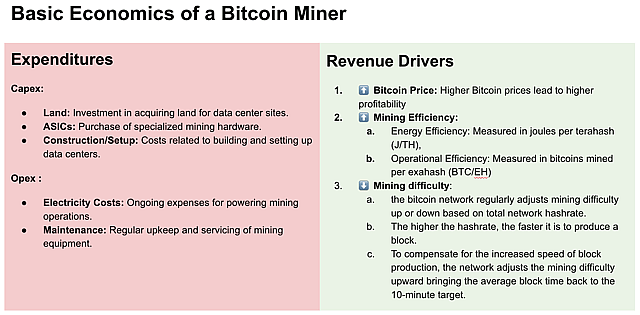

The Basics of Bitcoin Mining

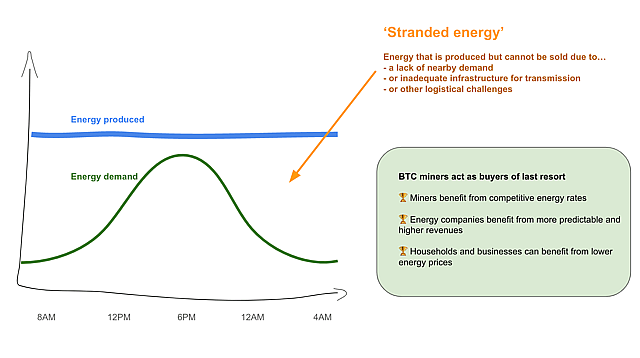

All miners must find the cheapest electricity possible to ensure profitability. Because of this, miners are incentivized to seek out 'stranded energy'—excess energy from power plants that would otherwise be wasted, often in remote locations.

IREN acts as a buyer of last resort, benefiting from competitive electricity costs (averaging around $0.05 per kWh as of late 2023) while simultaneously supporting electricity networks through automatic dynamic load management. Their data centers can adjust electricity usage based on demand and renewable energy production. This flexibility allows them to adapt dynamically to fluctuating costs. This symbiotic relationship between the energy company and the miner creates a virtuous cycle where IREN secures highly competitive energy rates, energy companies benefit from increased revenues and predictability, and households and businesses enjoy a more stable grid and lower energy prices.

As of June 2024, the company’s cost per Bitcoin mined was approximately $39,466, providing a post halving gross margin of 41%. The company expects to reduce this further this year with the upgrade of the miners fleet.

Peer comparison

IREN is a mid-tier miner that stands out due to its superior energy and mining efficiency (25 J/TH vs most of competitors being above 27) ranking first with 25 bitcoins mined per 1 EH/s. The company plans to improve further by the end of the year targeting of 16 J/TH with the deployment of a fully updated fleet of Bitmain S21 PRO miners, already secured through recent capital raising via substantial share dilution.

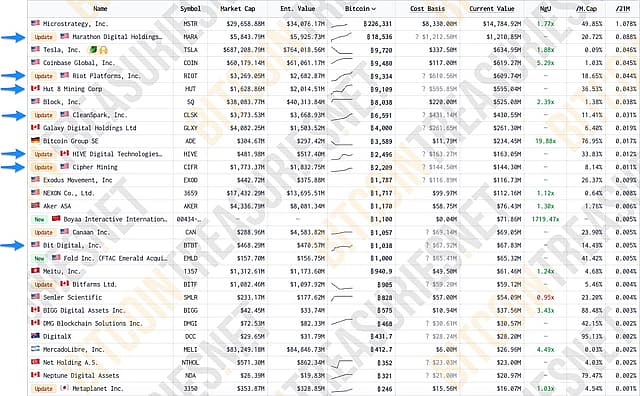

Unlike most other miners, IREN sells 100% of its mined Bitcoin daily, regardless of the price. This strategy benefits the company by eliminating the need for custody and improving cash flow. In contrast, Marathon has accumulated a record amount of BTC as company treasury (currently 18,536 bitcoins, valued at approximately $1.23 billion), while Cleanspark tends to accumulate during bear markets and sell during bull markets. Each strategy has its pros and cons, which is why I diversify my investments across multiple miners, including shares in Marathon and Cleanspark.

https://bitcointreasuries.net/

Financials

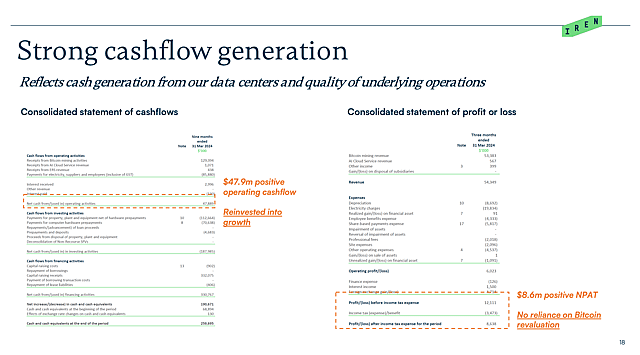

The company holds $425.3 million in cash reserves, raised through significant share dilution over the past year. Despite this, the successful capital raise ensures robust funding for expansion and strategic initiatives without the immediate need for external financing. IREN is, at the time of writing, in good financial shape with no debt and just recently became profitable in Q1 2024, reporting strong cash flow of $47.9m and USD$8.6m in net profit. It is important to note that Q1 2024 was pre-halving (mining rewards halved in April 2024; at the time of writing, we still don't have official data for Q2).

Growth Catalysts

- Ambitious Plans to Expand Mining Capacity: IREN surpassed its H1 2024 growth target, reaching 10 EH/s more than a month ahead of schedule. The company now aims to achieve 20 EH/s by September 30, 2024, and 30 EH/s by the end of the year. The image below highlights the ongoing construction at the Childress site, which is set to increase from 100 MW of operational power to 350 MW by December 31, 2024. Update (July 24, 2024 ): The Company announced it has reached 750MW of available power capacity at its Childress siteA successful upgrade to 30 EH/s by year-end would place IREN among industry leaders like RIOT, MARA, and CLSK, who are also planning to expand towards a staggering 70 EH/s. However, the expansion to 30 EH/s appears to be only partially funded, raising concerns about potential further dilution in 2024, which I will monitor closely. The company is also considering a further expansion to 40 EH/s in 2025.

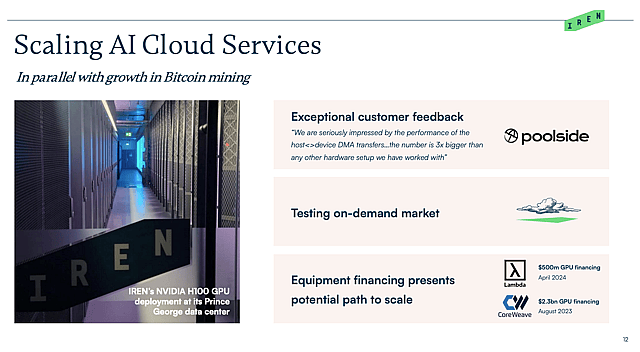

- Strategic Diversification: IREN is exploring HPC and AI applications to diversify its revenue streams, particularly during BTC price cycle downturns. Its AI Cloud Services, featuring 816 NVIDIA H100 GPUs, saw a 21% revenue increase in June 2024 due to higher utilisation by their customer, Poolside AI, and the onboarding of new customers. This growth reflects the company's expanding service capabilities in both reserved and on-demand markets.I remain somewhat skeptical about this strategy, as it could distract from the company's core mining business. The CEO has addressed these concerns, emphasising that this is not a pivot away from mining but an exploration of a complementary business. He clarified that while AI data centers are typically close to end users to minimise latency, this is only necessary for inference, not for AI training, which is IREN’s focus. Furthermore, IREN's data centers are built with high energy capacity in mind, given that the H100 GPU requires significant power (70kW per rack). Thus, setting up an AI data center with their existing infrastructure is primarily a matter of integrating these GPUs.While it's early to determine the success of this strategy, I currently view it more as a PR effort to enhance their brand, especially for potential investors and banks. The CEO mentioned the challenges of raising capital due to Bitcoin mining's negative reputation with traditional financial institutions, so this diversification may help improve their standing in the financial community.

- Bitcoin Price: I expect Bitcoin price to keep rising into 2025 driven by:

- Sustained ETF inflows & institutional demand

- Rate cuts and an increase in global liquidity

- More favourable regulations in the US

- Less sell pressure after halving event, German Gov. dumping and Mt.Gox distribution

- Sustained ETF inflows & institutional demand

- Regulatory Tailwinds: A Republican win in the upcoming elections would present a significant regulatory catalyst. This favourable environment could further legitimise and bolster the industry. Ex-President Trump has recently stated his support for Bitcoin and miners, following meetings with companies like Cleanspark. While it’s challenging to trust any politician, it’s unlikely he would continue the strategies pursued by the current administration over the last few years, which has also shown recent signs of a pivot away from their anti-crypto stance.

- Unlocking Value from Land and Energy Contracts: IREN is exploring strategies to unlock value from its land and energy contracts, considering that current data center growth is hampered by grid connection wait times, as reported by Morgan Stanley in a recent report. According to the firm, it takes five years for an existing data center to increase its energy capacity, which until now wasn’t required to run a regular data center. However, AI requires high amounts of energy, and miners are already positioned to support that. This strategic move may enhance revenue streams and profitability in the future.

Risks

- Bitcoin Price, Cyclicality, and Unpredictability: The success of IREN is heavily dependent on the continuous increase in Bitcoin prices over the coming years. Regardless of IREN's efforts to update its fleet of miners and run the company efficiently, these efforts will be in vain if Bitcoin's price does not stay sufficiently high to maintain profitability. The inherently unpredictable and cyclical nature of the Bitcoin market, characterised by its boom and bust cycles, adds a significant layer of uncertainty to the business.

- Need for Dilution: Iren has drastically diluted shareholders in the past. To maintain growth and fund new mining equipment, IREN may need to resort to more equity dilution unless it remains consistently profitable. Investors should be prepared for potential substantial dilution.

- Operational Risks: The technical complexities of HPC and AI services require IREN to develop the necessary software and expertise. The highly competitive nature of these markets means IREN must establish strong value propositions to attract and retain clients.

- Regulatory Risks: Adverse regulatory developments could pose significant risks to operations and profitability, such as the introduction of a Bitcoin mining tax proposed by Elizabeth Warren and her ‘anti-crypto army’ in the past.

- Short sellers: A short seller's report published in July 2024 by Culper Research criticised Iren for operational inefficiencies and financial issues, including significant cash burn and share dilution, while noting the CEOs' recent share sales. Analysts at Bernstein SG have disputed Culper's claims, maintaining an "outperform" rating and a target price of $26 for Iren shares. However, more short reports might emerge, considering the company is widely misunderstood, which could create further volatility.

Valuation

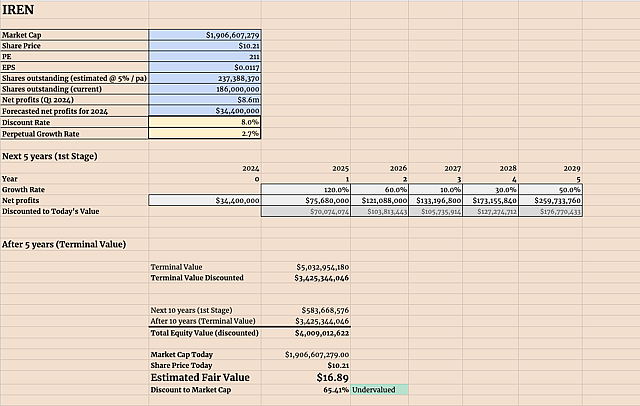

At the time of writing, I approximate the fair value per share to be around $16.89, still presenting a solid upside from the current share price of $10.11.

Hypothesis Underlying the Valuation

The valuation is based on the assumptions that

- Bitcoin price continues to increase in the next 12 months and reaches US$100,000

- In the next cycle low, Bitcoin won't go below US$60,000

- IREN achieves its goals to expand mining capacity in 2024 to 30 EH/s.

- IREN maintains and strikes new deals with energy companies to ensure low energy costs (less than $0.05/kW)

- The company's strong financial position can support its expansion plans with minimal dilution. I do have factored in a 5% annual increase in shares outstanding.

- The successful transition into HPC and AI services starts to generate meaningful amount of revenues during bitcoin's cycle lows (20% of mining).

Earnings Projections:

- 2024: $34.4 million calculated as $8.6M x 4 qtr

- 2025: $75.68 million, growth of 120% YoY

- 2026: $121.09 million, growth of 60% YoY

- 2027: $133.19 million, growth of 10% YoY

- 2028: $173.15 million, growth of 30% YoY

- 2029: $259.28 million, growth of 50% YoY

DCF Valuation:

- Discount Rate: 8.0%

- Perpetual Growth Rate: 2.7%

- Shares Outstanding: 237,388,370 (5% dilution p.a from 186,000,000)

Conclusion

IREN represents an intriguing yet risky investment opportunity in the evolving landscape of Bitcoin mining and computational services. With its leading efficiency, strategic diversification into HPC and AI, and strong financial footing, IREN is well-positioned to capitalise on future growth opportunities. However, given the inherent risks, it's wise for investors interested in the Bitcoin mining space to diversify with other miners that have different strategies, such as Marathon, Cleanspark, Wulf, and Core Scientific.

Investors should monitor both the company and Bitcoin closely, considering the high risks associated with market volatility and potential further dilution. The estimated fair value per share suggests significant upside, but the valuation is simplistic, and the company must deliver on all its strategic initiatives to realise this potential, with Bitcoin needing to continue to rise.

Major red flags in the short term include potential issues with the deployment of new ASICs to get to 30 EH/s and further dilution in 2024.

One final question remains: Why should someone bullish on Bitcoin invest in miners and IREN specifically instead of simply buying the underlying digital commodity? The answer is simple: outperformance. I expect IREN to trade as a beta play to Bitcoin, following its trajectory but with greater swings, providing the possibility to outperform Bitcoin over the next 12 months and potentially in the future.

Disclaimer: I'm NOT a financial advisor, this is NOT financial advice. Please do your own research.

Have other thoughts on IREN?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

BlackGoat is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. BlackGoat has a position in NasdaqGS:IREN.. Simply Wall St has no position in any companies mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.