Last Update23 Aug 25Fair value Increased 70%

Ondas Holdings’ consensus price target has been significantly raised to $5.00 as analysts cite the company’s strengthening leadership in U.S. drones, increasing defense sector traction, and large addressable opportunities that underpin expectations for robust long-term growth.

Analyst Commentary

- Bullish analysts highlight Ondas' strong positioning as a leading U.S.-based pure-play drone company, expecting the unmanned aerial systems industry to enter a multi-year supercycle.

- The company's end-to-end portfolio is targeting high-growth market verticals, with analysts estimating a near-term addressable opportunity exceeding $5 billion.

- The OAS drones business is gaining significant traction in the defense sector, supporting expectations for substantial revenue growth.

- Ondas' continued execution on its strategic roadmap is driving confidence in sustained multiple expansion and long-term performance.

- Despite recent significant stock price appreciation, analysts remain optimistic that large greenfield opportunities and Ondas' growth trajectory can drive further upside.

What's in the News

- Ondas Holdings completed two follow-on equity offerings: $39.99 million (22.4 million common shares at $1.25, 9.6 million pre-funded warrants at $1.2499), and $150.02 million (46.16 million common shares at $3.25).

- Multiple 60- and 90-day lock-up agreements enacted for common stock, warrants, stock options, and RSUs involving executives, directors, and major stockholders.

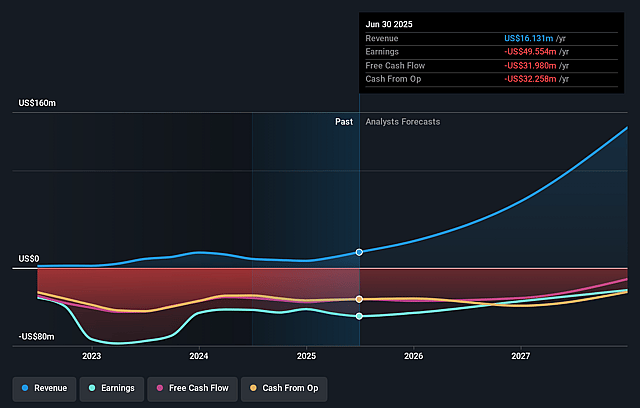

- Ondas reaffirmed 2025 revenue guidance of at least $25 million.

- Subsidiary American Robotics entered a strategic partnership with Mistral Inc. to accelerate adoption of defense and public safety drone platforms in U.S. government channels.

- Ondas formed a partnership with Klear Inc. to provide off-balance sheet working capital solutions to subsidiaries and affiliates, supporting acquisition-driven growth.

Valuation Changes

Summary of Valuation Changes for Ondas Holdings

- The Consensus Analyst Price Target has significantly risen from $2.94 to $5.00.

- The Future P/E for Ondas Holdings has significantly risen from 46.45x to 109.27x.

- The Net Profit Margin for Ondas Holdings has significantly fallen from 10.99% to 7.54%.

Key Takeaways

- Strategic partnerships and expanding defense contracts in various sectors are driving significant revenue growth and market diversification for Ondas Holdings.

- Advancements in autonomous systems and private network technologies are set to enhance operational efficiency, potentially improving margins and financial performance.

- High operating expenses and debt reliance are challenges, with conservative revenue expectations and volatile margins posing risks to future profitability and growth.

Catalysts

About Ondas Holdings- Provides private wireless, drone, and automated data solutions in the United States and internationally.

- Ondas anticipates record revenue growth in 2025, primarily driven by Ondas Autonomous Systems (OAS), due to significant backlog and expanding programs with Optimus and Iron Drone systems in defense and homeland security sectors. This will directly impact revenue.

- The strategic partnership with Palantir Technologies aims to leverage advanced AI capabilities to enhance operational efficiencies and scale OAS’s operations, which is expected to support the revenue ramp and broaden their customer base, influencing earnings and margins through improved operational scale.

- The expansion of OAS’s market presence, with increased customer engagement and government contracts in defense sectors in Israel and the UAE, is set to secure additional military customers, suggesting potential revenue growth and improved market diversification.

- Expected improvements in operating leverage as revenues grow, particularly at OAS, are set to recover gross margins, which could reach 50% or better in the second half of 2025, impacting net margins positively.

- Continued strategic value building at Ondas Networks and progress in private wireless network technologies for rail operations, which includes 900-megahertz network rollouts and new product opportunities, aims to unlock further revenue streams and bolster financial performance.

Ondas Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ondas Holdings's revenue will grow by 141.1% annually over the next 3 years.

- Analysts are not forecasting that Ondas Holdings will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Ondas Holdings's profit margin will increase from -433.8% to the average US Communications industry of 10.7% in 3 years.

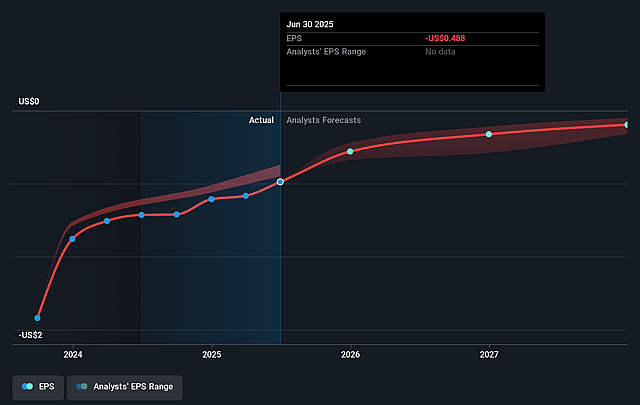

- If Ondas Holdings's profit margin were to converge on the industry average, you could expect earnings to reach $16.3 million (and earnings per share of $0.08) by about July 2028, up from $-46.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 40.9x on those 2028 earnings, up from -7.8x today. This future PE is greater than the current PE for the US Communications industry at 28.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.59%, as per the Simply Wall St company report.

Ondas Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ondas Holdings faced challenges in 2024, such as extending timelines at Ondas Networks and disruptions due to military activity in Israel, which could impede future revenue growth if similar issues recur.

- The company's revenue expectations for 2025 remain conservative at $25 million, with uncertainties related to Ondas Networks affecting the potential for revenue expansion.

- Gross margins are expected to be volatile due to the early stages of platform adoption and shifts in revenue mix, which may impact net margins and profitability.

- As of 2024, Ondas Holdings reported high operating expenses and adjusted EBITDA loss, with existing revenues not covering these expenses, posing a risk to future earnings if revenue growth does not accelerate as projected.

- The $52 million in debt outstanding and reliance on raising additional funds or extending debt terms might impact the company's financial health and its ability to invest in growth initiatives.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $2.5 for Ondas Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.0, and the most bearish reporting a price target of just $2.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $151.6 million, earnings will come to $16.3 million, and it would be trading on a PE ratio of 40.9x, assuming you use a discount rate of 7.6%.

- Given the current share price of $2.1, the analyst price target of $2.5 is 16.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.