Last Update 07 Jul 26

Fair value Increased 2.82%OKTA: Agentic AI Identity Hype Will Eventually Confront Full Pricing

Okta's analyst fair value estimate has been nudged higher to $121.88 from $118.53, with analysts pointing to a broad series of price target increases tied to stronger Q1 execution and growing interest in the company's agentic AI identity and security offerings.

Analyst Commentary

Street research on Okta clusters around two main themes: how much credit to give the stock for its agentic AI opportunity, and how sustainable the current execution looks after a strong Q1.

Bullish Takeaways

- Bullish analysts highlight solid Q1 results, with repeated references to beats across revenue, remaining performance obligations, operating margin, and free cash flow, which they see as evidence of improved execution and go to market productivity.

- Many upbeat reports point to rising customer interest in Okta's agentic AI and identity security offerings, including traction in identity governance and privileged access management, and argue that this helps justify higher valuation multiples and price targets up to US$165.

- Several firms call out an improving demand backdrop in identity security, supported by field checks and CIO surveys that put AI and AI readiness spending high on IT budget priority lists, which they see as supportive of Okta's long term growth profile.

- Supportive commentary often frames Okta as a neutral, independent identity provider that fits into zero trust architectures and multivendor environments, which they argue positions the company to capture more large enterprise deals over time.

Bearish Takeaways

- Bearish analysts, including Mizuho, argue that after a sharp share price move of 48% over two sessions and 67% year to date, Okta's valuation looks "full at current levels," leading them to downgrade the stock even as they lift the price target to US$125.

- Cautious research notes flag that the timing and magnitude of any agentic AI revenue uplift are still unclear, with some firms explicitly stating that guidance embeds minimal contribution from these products and that many implementations remain early.

- Some more neutral or cautious voices prefer to stay "on the sidelines," citing questions about whether Okta can meaningfully re accelerate growth in the near to medium term and whether recent strength in Q1 metrics is enough to justify aggressive long term assumptions.

- There are also reminders that product feature depth in certain areas still lags some competitors, which could limit pricing power or win rates if larger security vendors push harder into identity over time, especially if budgets become more scrutinized.

What’s in the News for Okta

- Okta featured in Q1 cybersecurity earnings coverage, with the company reporting an 11.2% year over year revenue increase and a beat on billing estimates, which was linked in that report to strong stock performance after the release. Source: "Spotting Winners: Okta (NASDAQ:OKTA) And Cybersecurity Stocks In Q1".

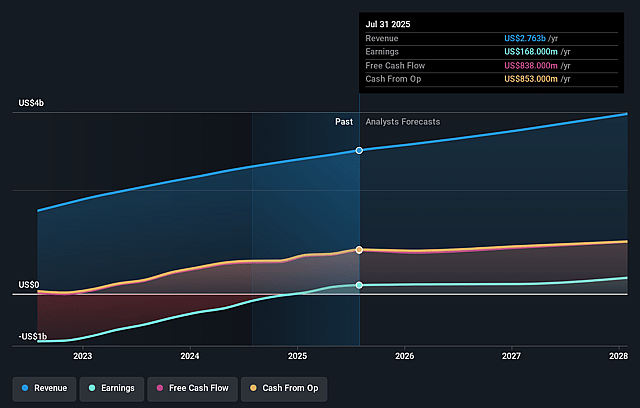

- Okta issued earnings guidance for fiscal Q2 2027, indicating expected total revenue between US$790 million and US$794 million, and for the full fiscal year 2027, total revenue between US$3.185b and US$3.205b, described in the guidance as a 9% to 10% year over year growth range.

- Okta was dropped as a constituent from multiple Russell growth benchmarks, including the Russell Small Cap Comp Growth, Russell Midcap Growth, Russell 1000 Growth, Russell 3000E Growth, and Russell 3000 Growth benchmarks.

- Okta reported progress on its share repurchase program, with 3,027,000 shares bought between February 1, 2026 and April 30, 2026 for US$240.83 million, and a total of 3,902,000 shares repurchased for US$320.14 million under the buyback first announced on January 5, 2026.

- Okta featured in a product announcement from Automation Anywhere, which introduced EnterpriseClaw, an AI agents capability developed with partners including Cisco, NVIDIA, Okta, and OpenAI, where Okta is described as providing cross agent identity management and authentication controls.

Valuation Changes for Okta

- Fair Value: The updated analyst fair value estimate has edged higher from $118.53 to $121.88, a small upward adjustment of around 3%.

- Discount Rate: The discount rate has risen slightly from 8.73% to 8.82%, which implies a modestly higher required return for Okta in the model.

- Revenue Growth: The assumed long term revenue growth rate has been adjusted marginally from 9.62% to 9.61%, effectively unchanged in the latest update.

- Net Profit Margin: The long term net profit margin assumption has been trimmed from 13.97% to 13.59%, a small reduction of around 0.4 percentage points.

- Future P/E: The future P/E multiple has moved up from 47.0x to 48.6x, indicating a slightly higher valuation multiple applied to Okta's projected earnings.

Key Takeaways

- Okta benefits from growing demand for unified cloud identity platforms and rising security needs amid complex digital transformations, driving durable revenue and larger contracts.

- Expansion into AI-driven security and broadening platform offerings increases cross-sell opportunities, supporting margin improvement and long-term profitability.

- Intensifying competition, integration risks, limited new customer growth, selective international focus, and evolving technologies threaten Okta's revenue growth, pricing power, and long-term margins.

Catalysts

About Okta- Operates as an identity partner in the United States and internationally.

- Okta is positioned to capture expanding demand as enterprises globally accelerate cloud migration and digital transformation, with increasing complexity and fragmentation in identity systems driving large organizations to consolidate onto a unified, cloud-native platform-supporting multi-year revenue growth and larger average contract values (ACV).

- The proliferation of AI agents and nonhuman identities is creating new, urgent security use cases that require sophisticated identity governance, privileged access management, and policy controls-areas where Okta is innovating (Cross App Access, Auth0 for AI Agents, Axiom acquisition), opening incremental growth avenues and potential margin expansion through higher value and differentiated products.

- The rising frequency and sophistication of cyberattacks, combined with tightening regulatory mandates (especially in the public sector and large enterprises), are establishing identity as a mission-critical, recurring investment category; this aligns with Okta's increased penetration in federal and enterprise verticals, which enhances revenue durability and long-term earnings visibility.

- Okta's expanding platform breadth beyond workforce IAM-including customer identity, security posture management, threat protection, and suites-improves cross-sell and upsell opportunities, supporting top-line acceleration and leveraging existing sales channels for improved operating leverage and net margin improvement as specialization in go-to-market teams boosts sales productivity.

- Global adoption of Zero Trust security frameworks and the movement toward SaaS-native security stacks favor independent, extensible platforms with broad integration ecosystems, allowing Okta's neutral, open approach to capture wallet share as customers seek to avoid vendor lock-in from larger, bundled security suites-sustaining long-term revenue growth and profitability.

Okta Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Okta's revenue will grow by 9.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.2% today to 13.6% in 3 years time.

- Analysts expect earnings to reach $536.4 million (and earnings per share of $3.36) by about July 2029, up from $247.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $773.1 million in earnings, and the most bearish expecting $254.4 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 48.8x on those 2029 earnings, down from 104.6x today. This future PE is greater than the current PE for the US IT industry at 18.6x.

- Analysts expect the number of shares outstanding to decline by 1.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.82%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The ongoing consolidation of the cybersecurity and identity markets-exemplified by platform companies like Palo Alto entering the space-could pressure Okta's market share and negotiating leverage, especially if large enterprises increasingly prefer integrated multi-function security suites over independent identity specialists; this trend risks long-term revenue growth and may impact Okta's ability to maintain pricing power.

- Okta's strategy of frequent product expansion (e.g., acquisition of Axiom Security and rapid feature rollout) introduces elevated product integration and execution risk; difficulties integrating new technologies and teams or falling behind in essential innovations (such as passwordless authentication or AI agent management) could erode Okta's competitive differentiation, putting downward pressure on revenue growth and gross margins.

- The continued focus on upsell and cross-sell to existing large enterprise and public sector customers, rather than driving robust new customer growth, may signal potential limitations in Okta's addressable market expansion; if new customer pipeline falters or churn increases due to past breaches or competitive switching, recurring revenue and long-term earnings durability could be negatively affected.

- International market expansion is being prioritized only in select top-10 countries to avoid spreading resources too thin; however, if Okta encounters increased regulatory complexity, data localization requirements, or stiffer competition from local or global players (especially with tightening global privacy laws), international growth may underperform, constraining total revenue and operating margin expansion opportunities.

- The rise of decentralized identity technologies (such as blockchain-based identity) and the growing commoditization of identity and access management tools via open-source or low-cost solutions could increase price-based competition and reduce Okta's revenue per customer; failure to differentiate sufficiently in this evolving landscape may suppress average contract values and compress net margins over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $121.88 for Okta based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $165.0, and the most bearish reporting a price target of just $75.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.9 billion, earnings will come to $536.4 million, and it would be trading on a PE ratio of 48.8x, assuming you use a discount rate of 8.8%.

- Given the current share price of $148.6, the analyst price target of $121.88 is 21.9% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Okta?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.