Last Update 01 Jul 26

Fair value Decreased 5.48%IDXX: Expanded Diagnostics And Reset Expectations Will Support Future Shareholder Value

Analysts have trimmed their price targets on IDEXX Laboratories by roughly $40. This reflects slightly lower fair value estimates, a modestly reduced revenue growth outlook, and a lower assumed future P/E multiple.

Analyst Commentary

Recent research on IDEXX Laboratories points to a more balanced view, with analysts weighing the company’s growth prospects against valuation and execution risks. The lower price targets, including meaningful cuts mentioned in recent reports, underline a reassessment rather than a full shift in sentiment.

Bullish Takeaways

- Bullish analysts still see IDEXX Laboratories as a high quality business, with a focus on durable demand in veterinary diagnostics that can support long term revenue growth assumptions.

- Some commentary around neutral initiations suggests room for upside if IDEXX executes well on product adoption and operational efficiency, especially if current expectations are reset to more achievable levels.

- The reduced price targets incorporate lower assumed P/E multiples, which bullish analysts view as creating a more grounded entry point compared with prior, higher valuation assumptions.

- Supportive views often highlight IDEXX’s established market position and recurring revenue characteristics as positives for long term cash flow visibility.

Bearish Takeaways

- Bearish analysts point to the size of the recent price target cuts, including triple digit US$ reductions in some cases, as a sign that prior expectations for IDEXX Laboratories were too optimistic.

- Reduced revenue growth outlooks suggest concern that the company may face slower procedure volumes or more conservative spending by veterinary clinics than previously built into models.

- Lower assumed future P/E multiples reflect caution that investors may be less willing to pay premium valuations for IDEXX if execution is uneven or growth moderates.

- Neutral ratings indicate uncertainty around the near term risk or reward skew, with some analysts preferring to wait for clearer evidence on growth and margin trends before turning more positive.

What's in the News for IDEXX Laboratories

- IDEXX Laboratories expanded its Fecal Dx antigen testing platform to include taeniid tapeworm species, including Taenia and Echinococcus, adding broader intestinal parasite detection in a single test for wellness and sick pet care. Source: company product announcement.

- The Fecal Dx platform now covers seven key parasite groups, and IDEXX Reference Laboratories customers in the United States and Canada are set to receive the taeniid tapeworm upgrade beginning in late June at no additional cost. Source: company product announcement.

- IDEXX Laboratories is integrating the SDMA renal biomarker into Catalyst CLIPs, making complete kidney function evaluation part of common in-clinic chemistry panels and aiming to support earlier detection of kidney function loss in dogs and cats. Source: company product announcement.

- Clinical use of SDMA at IDEXX has scaled to about 119 million patient tests globally, with results integrated into VetConnect PLUS alongside other diagnostics to support kidney health assessment during the veterinary visit. Source: company product announcement.

- Recent index actions show IDEXX Laboratories being added to several Russell value and dynamic benchmarks, including the Russell 1000 Value and Russell Midcap Value indexes, which can influence how index-based investors gain exposure to the stock. Source: index constituent changes.

Valuation Changes for IDEXX Laboratories

- Fair Value: trimmed from $750.23 to $709.14, a reduction of about 5% in the modelled estimate.

- Discount Rate: adjusted slightly lower from 7.69% to 7.48%, indicating a modest change in the required return assumption.

- Revenue Growth: eased from 9.01% to 8.68%, reflecting a small reduction in modelled top line growth for IDEXX Laboratories.

- Net Profit Margin: moved marginally from 26.16% to 26.11%, keeping profitability assumptions broadly stable.

- Future P/E: revised down from 50.11x to 44.31x, a significant reset in the valuation multiple applied to IDEXX Laboratories in the model.

Key Takeaways

- Expansion in innovative diagnostic platforms and international markets is driving recurring revenue growth, margin expansion, and enhanced geographic diversification.

- Strong customer retention and broader adoption of cloud solutions create stable, high-margin revenue streams and position the company for sustained long-term earnings growth.

- Slowing U.S. clinical visit growth, international adoption challenges, reliance on instrument placements, rising competition, and price sensitivity all threaten IDEXX's long-term revenue and margin prospects.

Catalysts

About IDEXX Laboratories- Develops, manufactures, and distributes products for the companion animal veterinary, livestock and poultry, dairy, and water testing industries in the United States and internationally.

- Rapid adoption of innovative diagnostic platforms such as inVue Dx, Catalyst Cortisol, and Cancer Dx are expanding IDEXX's addressable market and boosting recurring consumables demand, which is likely to drive sustained revenue and margin growth as new product usage ramps and menu breadth increases.

- Expansion of commercial investments in underpenetrated international markets-combined with localization strategies and tailored product offerings-is fueling double-digit recurring diagnostic revenue growth outside North America, providing geographic diversification and supporting long-term top-line growth.

- Increasing utilization rates of advanced diagnostics per clinical visit, supported by pet owners' willingness to spend on preventive and early detection care for an aging pet population, are driving higher diagnostic frequency and supporting recurring revenue and net margin expansion.

- Broader adoption and enhancement of cloud-based practice management and analytics solutions is strengthening customer retention, raising multi-product utilization, and increasing customer lifetime value, translating to improved recurring revenue and net margins.

- High customer retention and growing installed base of premium instruments provide IDEXX with stable, high-margin recurring revenue streams, positioning the company to compound earnings growth over time as industry consolidation and elevated care standards continue.

IDEXX Laboratories Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

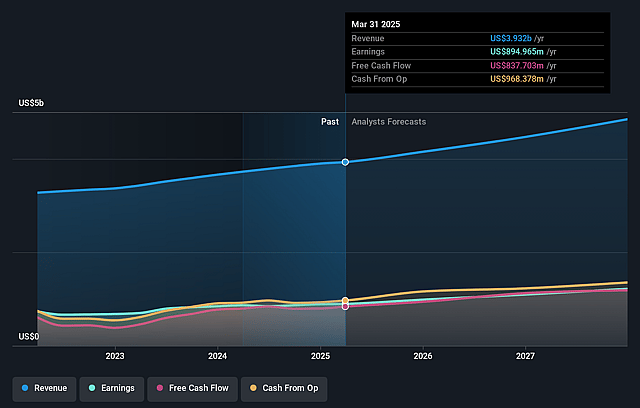

- Analysts are assuming IDEXX Laboratories's revenue will grow by 8.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 24.6% today to 26.1% in 3 years time.

- Analysts expect earnings to reach $1.5 billion (and earnings per share of $19.29) by about July 2029, up from $1.1 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 44.7x on those 2029 earnings, up from 38.7x today. This future PE is greater than the current PE for the US Medical Equipment industry at 25.6x.

- Analysts expect the number of shares outstanding to decline by 1.4% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.48%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Sustained declines in U.S. clinical visit growth (down 2.5% in the quarter and forecasted to remain soft) suggest that underlying veterinary visit frequency is under pressure and could limit CAG Diagnostic recurring revenue growth over the long term, directly impacting revenue and earnings resilience.

- International markets, while delivering strong growth now, are described as "more embryonic" and dependent on expanding diagnostic use among smaller clinics; slower adoption or inability to replicate U.S.-style diagnostic penetration may temper future global revenue expansion and earnings diversification.

- The consumables revenue surge is highly linked to rapid instrument placements (notably inVue Dx); if future instrument placement growth slows or installed base saturation is reached (implied by management's expectation of a relative slowdown in 2H placements compared to 2Q), recurring consumable revenue growth and margin improvements could decelerate, affecting long-term net margins.

- Intensifying competition, including from new entrants and disruptive startups targeting point-of-care and specialty diagnostics, is acknowledged as ongoing; any failure to maintain IDEXX's innovation pace or if competitors introduce faster/cheaper solutions could erode pricing power and market share, negatively impacting both revenue growth and net margins.

- Heavy reliance on price increases for recent revenue gains (e.g., 4%+ global net price realization), combined with macroeconomic pressures, regulatory risk, and the possibility of large veterinarian groups negotiating lower prices, could squeeze long-term operating margins and restrict IDEXX's ability to sustain high earnings growth rates.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $709.14 for IDEXX Laboratories based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $805.0, and the most bearish reporting a price target of just $470.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $5.7 billion, earnings will come to $1.5 billion, and it would be trading on a PE ratio of 44.7x, assuming you use a discount rate of 7.5%.

- Given the current share price of $537.58, the analyst price target of $709.14 is 24.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on IDEXX Laboratories?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.