Last Update 04 Jun 26

Fair value Increased 1.88%JBHT: Tight Trucking Capacity And Higher P/E Will Limit Future Upside Potential

Analysts lifted the updated J.B. Hunt Transport Services fair value estimate by about $4 to $238.27, mainly reflecting a higher future P/E assumption, supported by a broad wave of recent price target increases across major research firms.

Analyst Commentary

The recent wave of target price revisions for J.B. Hunt Transport Services adds useful context around how professional analysts are thinking about the stock’s valuation, execution risk, and growth potential. Most of the changes are upward adjustments, with only one recent trim. This gives you a sense of where sentiment currently leans and where the main debate sits.

Bullish Takeaways

- Bullish analysts are consistently lifting target prices by single to double digit dollar amounts, which signals greater comfort with a higher P/E multiple and the company’s ability to support that valuation through its operating model.

- Several target hikes in quick succession suggest increased confidence that J.B. Hunt can execute on growth initiatives in its key businesses. This is enough for analysts to underwrite higher long term earnings power in their models.

- Large upward adjustments in some cases, such as moves of US$20 or more, indicate that some analysts see meaningful upside versus prior expectations, particularly if the company delivers on efficiency and volume assumptions embedded in their forecasts.

- Support from major firms such as JPMorgan and Goldman Sachs adds weight to the bullish camp. Their updated targets imply that the stock’s current valuation is not viewed as stretched under their base case scenarios.

Bearish Takeaways

- One firm recently trimmed its target by US$3, which shows that not all analysts are aligned and that some remain cautious about how much investors should pay for the stock, even with the broader backdrop of rising targets.

- The wide spread in individual target moves, ranging from only a few dollars to US$40 or US$50, highlights uncertainty around execution and growth outcomes. It also suggests that the margin for error on current valuation may be tight for more cautious analysts.

- Bearish analysts appear focused on the risk that expectations have moved ahead of what the company can deliver, which could limit upside if earnings, cash flow or network efficiencies come in below the more optimistic assumptions baked into higher targets.

- The presence of both upward and downward revisions over the same period is a reminder that, while sentiment is generally positive, there is still debate over how durable current trends are and how much of that is already reflected in the share price.

What's in the News

- J.B. Hunt reported Q1 2026 earnings per share of $1.49, a 27% year-over-year increase that topped Wall Street forecasts, with revenue of $3.06b supported by broad-based demand and strong Intermodal volumes in the Eastern network. (Source: Recent earnings reports, May 15, 2026)

- Operational changes, including more than $30 million in cost reductions, contributed to improved profitability and margin expansion targets in the 10% to 12% range, even as truckload markets and labor conditions remained tight. (Source: Recent earnings reports, May 15, 2026)

- Intermodal, Dedicated Contract Services, and brokerage each contributed to revenue and operating income, with management indicating that the Dedicated segment is expected to return to fleet growth during the year. (Source: Recent earnings reports, May 15, 2026)

- J.B. Hunt shares reached an all time high of $265.34 following the Q1 2026 report, as analyst commentary highlighted tightening trucking capacity and margin prospects supported by the company’s intermodal network and physical assets. (Source: Recent earnings reports, May 15, 2026)

- Between January 1 and March 31, 2026, the company repurchased 383,000 shares for $80 million, bringing total buybacks under the October 22, 2025 authorization to 575,748 shares for $112 million. (Source: Company buyback update)

Valuation Changes

- Fair Value has been updated from $233.87 to $238.27, representing a slight increase in the estimated worth of the stock.

- The Discount Rate remains at 8.20%, reflecting only a minimal change, if any, in the assumed required return.

- Revenue Growth is held at about 6.63% and is effectively unchanged, so the updated valuation does not rely on different top-line growth assumptions.

- The Net Profit Margin is kept near 6.33% and is also effectively unchanged, indicating little adjustment to long-run profitability assumptions.

- The Future P/E has been updated from 25.77x to 28.19x, indicating a higher assumed earnings multiple in the new valuation work.

Key Takeaways

- Improved equipment utilization and cost optimization efforts enhance operational efficiencies, positively affecting net margins and profitability.

- Strategic investments in technology and capacity expansion support long-term revenue growth by accessing large addressable markets.

- Inflationary pressures, competitive rates, and muted demand in key segments challenge margins and earnings amidst an uncertain macroeconomic and policy environment.

Catalysts

About J.B. Hunt Transport Services- Provides surface transportation, delivery, and logistic services in the United States.

- Record first quarter intermodal volumes could indicate an ability to capture more market share, contributing to potential revenue growth.

- Efforts to improve equipment utilization and reduce empty move costs may enhance operational efficiencies, positively impacting net margins.

- Strategic investments in technology and capacity expansion may provide a platform for long-term revenue growth by better serving large addressable markets.

- Successful bid season outcomes, including modest rate increases and filling costly empty lanes, could drive better revenue and profitability metrics.

- The focus on reducing and optimizing costs, combined with a disciplined capital allocation strategy, suggests improvements in earnings as the company scales operations.

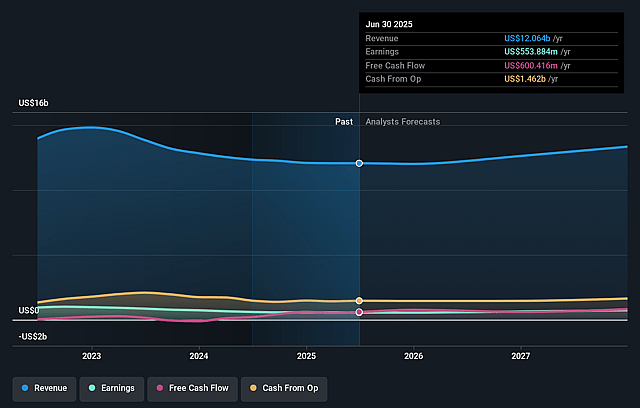

J.B. Hunt Transport Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming J.B. Hunt Transport Services's revenue will grow by 6.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.1% today to 6.3% in 3 years time.

- Analysts expect earnings to reach $931.3 million (and earnings per share of $10.42) by about June 2029, up from $622.1 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $1.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 28.3x on those 2029 earnings, down from 42.5x today. This future PE is lower than the current PE for the US Transportation industry at 42.5x.

- Analysts expect the number of shares outstanding to decline by 2.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.2%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company faces a challenging operating environment with inflationary cost pressures more than offsetting productivity improvements, affecting margins and earnings.

- Lower yields and increased insurance premiums have been weighing on operating income, indicating potential pressure on net margins and earnings.

- Seasonally lower volume and rate pressure coupled with competitive truckload rates, especially in the Eastern network, may limit the ability to achieve desired price increases and hurt revenue and margins.

- Demand for Final Mile services such as furniture and appliances remains muted, potentially impacting revenue and margin growth in this segment.

- The uncertain macro environment and changing trade policies, including tariffs, pose risks to supply and demand dynamics, which could impact revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $238.27 for J.B. Hunt Transport Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $171.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $14.7 billion, earnings will come to $931.3 million, and it would be trading on a PE ratio of 28.3x, assuming you use a discount rate of 8.2%.

- Given the current share price of $280.05, the analyst price target of $238.27 is 17.5% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on J.B. Hunt Transport Services?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.