Last Update 26 Jun 26

DCI: Q3 Beat And Narrowed Guidance Will Shape Balanced Future Returns

Analysts have trimmed their 12 month price target on Donaldson Company by $5 to $91 from $96, citing updated estimates after a fiscal Q3 beat and narrower organic guidance.

Analyst Commentary

Recent commentary around Donaldson Company focuses on how the latest fiscal Q3 results and updated organic growth guidance feed into valuation expectations over the next year.

Bullish analysts and bearish analysts are taking different cues from the same information, leading to a lower 12 month price target but mixed views on execution and growth visibility.

Bullish Takeaways

- Bullish analysts point to the fiscal Q3 beat as evidence that Donaldson Company is executing against current expectations, which can support confidence in near term earnings delivery.

- The narrowing of organic guidance is taken by some as a sign of improved visibility into the order pipeline, which can help investors frame potential outcomes more clearly.

- Even with a lower target, bullish analysts see room for the stock to reflect the updated estimate base if Donaldson Company continues to meet or slightly exceed quarterly expectations.

- Refreshed models after Q3 provide investors with a more current view of earnings and cash flow assumptions, which some see as reducing uncertainty around valuation inputs.

Bearish Takeaways

- Bearish analysts highlight that the cut in the 12 month price target signals a more cautious stance on what investors may be willing to pay for Donaldson Company shares relative to prior assumptions.

- The narrowed organic guidance range is also viewed as a constraint on upside, with less room for positive surprise in growth versus earlier expectations.

- Some bearish analysts see the updated estimates as reflecting a more balanced risk and reward profile, with limited valuation expansion if growth or margins do not materially outpace the revised outlook.

- The combination of a target reduction and a Hold rating framework suggests that, for more cautious analysts, Donaldson Company is priced closer to their view of fair value on current projections.

What’s in the News for Donaldson Company

- Donaldson Company issued earnings guidance for the fourth quarter of fiscal 2026, with expected sales between $25 million and $30 million. The company indicated that this would add around 70 to 80 basis points to its full year growth rate. (Source: Company guidance)

- The company provided an update on its share repurchase activity, stating that from February 1, 2026 to April 30, 2026 it repurchased 0 shares for $0 million. It also reported that it completed the previously announced buyback program with a total of 7,499,169 shares repurchased for $528.67 million since November 17, 2023. (Source: Buyback tranche update)

- Donaldson Company’s Board of Directors declared a regular cash dividend of $0.32 per share, described as a 6.7% change from the prior quarterly dividend of $0.30 per share. The dividend is payable on June 30, 2026 to shareholders of record on June 15, 2026. (Source: Dividend announcement)

Valuation Changes for Donaldson Company

- Fair Value: Modelled fair value remains at $96.80, with no change between the prior and updated estimates.

- Discount Rate: The discount rate has fallen slightly from 8.61% to 8.50%, implying a modest adjustment to the required return used in the Donaldson Company valuation work.

- Revenue Growth: The revenue growth assumption has risen slightly from 6.00% to 6.08%, reflecting a small change in expected top line expansion for Donaldson Company.

- Net Profit Margin: The net profit margin assumption has risen slightly from 12.99% to 13.07%, pointing to a minor revision in expected profitability levels.

- Future P/E: The future P/E multiple has edged down from 23.99x to 23.94x, indicating a very small reduction in the valuation multiple applied to Donaldson Company earnings forecasts.

Key Takeaways

- Expansion into high-growth filtration segments and strategic acquisitions are enhancing profit margins, earnings quality, and product innovation.

- Increased demand from stricter regulations, automation, and urbanization is driving sustained sales growth, recurring revenue, and operating margin improvement.

- Heavy dependence on legacy product segments and aftermarket sales, combined with external market headwinds, threatens long-term revenue growth, margin stability, and earnings predictability.

Catalysts

About Donaldson Company- Manufactures and sells filtration systems and replacement parts worldwide.

- Global expansion of environmental regulations and emissions standards is increasing demand for advanced filtration across industrial and transportation sectors, positioning Donaldson to achieve record sales in both Industrial Solutions and Mobile Solutions, with a direct positive impact on revenue and earnings growth in FY26 and beyond.

- Industrial automation and digitalization are driving higher requirements for contaminant-free environments, fueling double-digit growth in Donaldson's connected and aftermarket filtration solutions, improving the recurring revenue base and operating margins.

- Continued urbanization and infrastructure build-out globally-particularly in China and power generation-are expanding addressable markets, supporting recovery in first-fit sales and sustaining backlog visibility, underpinning revenue stability and top-line growth.

- Strategic investments and M&A in high-margin, structurally growing segments (e.g., Life Sciences and Food & Beverage filtration) are expected to enhance margin mix and earnings quality, with Life Sciences segment margins improving notably and diversified R&D accelerating product innovation.

- Ongoing replacement parts/service model and the rising installed base are improving revenue predictability and resilience, increasing aftermarket sales mix (now over 50% of certain businesses), which supports stable cash flow and long-term earnings durability.

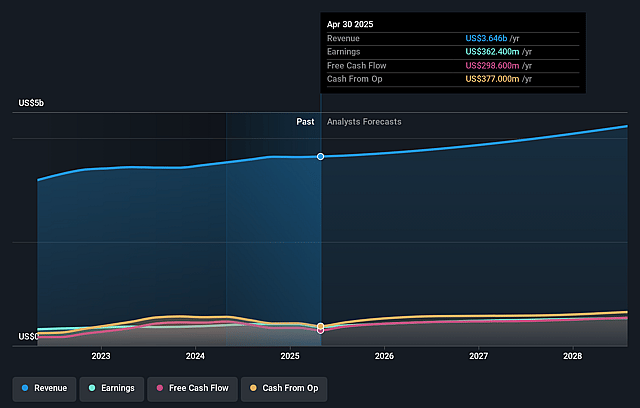

Donaldson Company Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Donaldson Company's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.5% today to 13.1% in 3 years time.

- Analysts expect earnings to reach $594.0 million (and earnings per share of $5.19) by about June 2029, up from $438.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 24.1x on those 2029 earnings, up from 23.5x today. This future PE is lower than the current PE for the US Machinery industry at 27.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.5%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent delays and muted performance in bioprocessing, a key growth driver within Life Sciences, suggest a slower-than-expected ramp in high-margin segments, limiting revenue growth and margin expansion until at least fiscal 2027.

- Heavy reliance on aftermarket and replacement part sales in both Mobile and Industrial Solutions exposes the company to long-term risks if customers gradually shift toward maintenance-free systems or adopt circular economy practices, which could weaken recurring revenue streams and future cash flow predictability.

- Ongoing uncertainties and caution regarding demand in China and other APAC and LatAm regions, including operating challenges from international trade tensions or macroeconomic headwinds, may constrain international sales growth and curtail overall top line expansion.

- Donaldson's strategy and current mix are still significantly dependent on traditional engine-based (ICE-related) filtration; despite growing diversification, accelerated electrification in transportation and off-highway equipment could erode core market revenue over the long term as demand for ICE filtration products declines.

- Substantial gross margin sensitivity to tariff-related cost inflation, LIFO accounting volatility, and ongoing footprint optimization initiatives signals exposure to operational margin squeeze if raw material or input costs rise and the company is unable to sustain price increases, posing a risk to net margin and future earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $96.8 for Donaldson Company based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $123.0, and the most bearish reporting a price target of just $79.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.5 billion, earnings will come to $594.0 million, and it would be trading on a PE ratio of 24.1x, assuming you use a discount rate of 8.5%.

- Given the current share price of $89.11, the analyst price target of $96.8 is 7.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Donaldson Company?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.