Last Update 02 Jul 26

Fair value Increased 3.86%AGCO: Tariff Relief And Q2 Earnings Setup Will Shape 2026 Margin Power

AGCO's analyst price target has been revised higher from $152 to about $158, with analysts pointing to tariff relief for agricultural equipment makers and a supportive sector setup ahead of upcoming earnings as key drivers for their updated assumptions.

Analyst Commentary

Recent research on AGCO highlights a mix of views, but the latest revisions show some bullish analysts becoming more constructive on the stock, particularly as they factor in tariff relief and the setup into upcoming earnings seasons across the broader machinery and industrial complex.

Several bullish analysts have raised formal price targets on AGCO, reflecting updated assumptions rather than a change in rating alone. These moves are being framed around sector level demand trends, expectations for earnings reports, and the potential earnings effect of lower tariffs on agricultural equipment.

One research note describes the recent White House section 232 tariff update as an incremental positive for agricultural equipment makers, with the reduction of tariffs on agricultural equipment to 15% from 25% cited as a potential earnings tailwind. Within that context, AGCO is grouped with peers that could see a slightly more material benefit because of their imported finished goods exposure.

Looking at the broader industrial and machinery group, some bullish analysts highlight what they describe as a positive setup for Q2 earnings across the sector, with demand trends characterized as strong in areas like power, data center, aerospace and defense, and infrastructure. While these comments are sector wide rather than AGCO specific, they inform how some investors are thinking about the company’s positioning and valuation within that group.

Bullish Takeaways

- Recent price target increases on AGCO from bullish analysts point to a view that current valuation may not fully reflect their updated earnings and sector assumptions.

- The cut in agricultural equipment tariffs to 15% from 25% is framed as an incremental positive, with AGCO cited as potentially seeing a slightly more material earnings tailwind relative to some peers.

- Bullish analysts see a constructive setup into Q2 earnings for the broader machinery and industrial group, which supports more confident modeling around AGCO’s near term execution.

- Sector commentary that highlights strong demand trends in areas such as power, data center, aerospace and defense, and infrastructure contributes to a more favorable backdrop for AGCO in multi industry portfolios.

What's in the News for AGCO

- AGCO is expanding fuel saving technologies across its Fendt, Massey Ferguson and Valtra tractor brands, with independent DLG PowerMix testing cited as reflecting efficiency outcomes in real world field and transport work. Source: AGCO product related announcement.

- AGCO Power engines, including the CORE engine family used in Fendt 600 and 700 Vario series tractors, are highlighted as part of integrated powertrain solutions focused on fuel efficiency, performance and uptime. Source: AGCO product related announcement.

- Management reports share repurchases of 333,755 shares from January 1, 2026 to March 31, 2026 for US$35.8 million, within a total of 2,330,959 shares bought for US$250 million under a program announced July 9, 2025. Source: AGCO buyback tranche update.

- AGCO states that its capital allocation framework includes pursuing acquisitions to support technology adoption, alongside reinvestment in the business, maintaining an investment grade balance sheet and returning capital to shareholders. Source: AGCO 2026 First Quarter Earnings Call.

- AGCO's Board approved a regular quarterly dividend rate of US$0.30 per share and declared a dividend payable on June 15, 2026, to stockholders of record on May 15, 2026, which would total US$1.20 per share on an annual basis at that rate. Source: AGCO dividend announcement.

Valuation Changes for AGCO

- Fair Value: The updated estimate has risen slightly from $152.00 to about $157.87, reflecting refreshed inputs in the model used for AGCO.

- Discount Rate: The assumed discount rate has moved slightly higher from 9.10% to about 9.26%, signaling a modestly higher required return in the updated framework.

- Revenue Growth: Assumed long term revenue growth has been trimmed from about 7.40% to about 6.50%, suggesting a more cautious stance on AGCO's top line expansion in the model.

- Net Profit Margin: The assumed net profit margin has edged up from about 7.78% to about 7.85%, indicating a slightly stronger earnings profile on each dollar of revenue in the updated assumptions.

- Future P/E: The forward valuation multiple has been nudged higher from about 13.42x to about 13.82x, pointing to a modestly richer P/E assumption for AGCO in the revised analysis.

Key Takeaways

- Leadership in precision agriculture and smart farming solutions enables AGCO to boost recurring revenues and margins amid rising global demand for digital agricultural technology.

- Expansion in emerging markets and focus on next-generation, eco-friendly machinery set the stage for robust long-term revenue growth and increased market share.

- Weakened demand, rising global uncertainties, competitive disruption, and operational challenges threaten AGCO’s long-term revenue, profitability, and market position.

Catalysts

About AGCO- Manufactures and distributes agricultural equipment and replacement parts worldwide.

- AGCO’s accelerating investment and leadership in precision agriculture—highlighted by the growth of its PTx Trimble joint venture and rapid integration of advanced technology across its product lines—positions the company to capture higher-margin, recurring revenue streams from smart farming solutions as global demand for digital and autonomous equipment surges, supporting significant future earnings and net margin expansion.

- The company’s continued focus on launching next-generation, environmentally efficient machinery, including low-emission and autonomous models, directly benefits from farmers’ increasing adoption of climate-smart agriculture, which is being accelerated by both customer preference and regulatory pressures, setting the stage for robust top-line growth and improved market share as replacement cycles shorten globally.

- Expansion in rapidly mechanizing emerging markets such as Brazil, coupled with AGCO’s strong local presence and investment in regional dealer networks, positions the company to benefit disproportionately from rising food demand and a growing middle class, which drives steady long-term revenue growth as modern equipment penetration increases.

- Structural cost reductions and modular manufacturing initiatives, which have already delivered and are expected to further deliver $100–$125 million in annual savings, will provide meaningful operating leverage and enhance profitability when industry volumes recover, leading to higher incremental margins and improved free cash flow conversion.

- The globalization and full-line rollout of premium brands like Fendt, especially as AGCO captures share in North and South America, is expected to drive mix improvement and higher operating margins, contributing to the company’s long-term target of 14–15 percent mid-cycle operating margins by 2029 and underpinning bullish projections for sustained earnings per share growth.

AGCO Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on AGCO compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming AGCO's revenue will grow by 6.5% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 7.4% today to 7.8% in 3 years time.

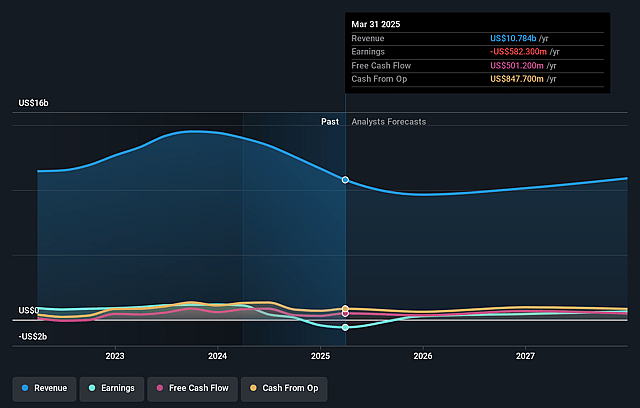

- The bullish analysts expect earnings to reach $983.2 million (and earnings per share of $14.67) by about July 2029, up from $771.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $679.6 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 13.9x on those 2029 earnings, up from 10.9x today. This future PE is lower than the current PE for the US Machinery industry at 27.9x.

- The bullish analysts expect the number of shares outstanding to decline by 2.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.26%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- AGCO is experiencing a sharp decline in net sales across all major regions, driven by persistently weak farm equipment demand, continued dealer inventory destocking, and reduced production volumes, which could continue to pressure both revenue and earnings in the coming years.

- The company faces increased exposure to geopolitical and trade uncertainties, with new and potential retaliatory tariffs—particularly between the US, EU, and China—raising costs and creating demand uncertainty, which is already anticipated as a net negative for both revenue and earnings per share.

- There are structural and demographic headwinds in key developed markets, including an aging farmer population, tightening rural labor supplies, and changing dietary preferences, all of which could shrink long-term demand for large-scale agricultural equipment and negatively impact AGCO’s addressable market and revenues.

- The pace of industry transition toward precision agriculture, automation, and as-a-service models could outstrip AGCO’s innovation and go-to-market capacity, leaving it vulnerable to loss of market share to more agile competitors and tech-driven new entrants, resulting in revenue erosion and margin compression.

- Persistent supply chain vulnerabilities, input cost inflation, and heavy reliance on lower-margin emerging markets threaten AGCO’s ability to maintain operating margins, as evidenced by recent factory underabsorption, higher discounts, and ongoing profitability weakness in key geographies, all of which may reduce future net income and overall earnings growth potential.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for AGCO is $157.87, which represents up to two standard deviations above the consensus price target of $128.5. This valuation is based on what can be assumed as the expectations of AGCO's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $159.0, and the most bearish reporting a price target of just $105.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $12.5 billion, earnings will come to $983.2 million, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 9.3%.

- Given the current share price of $116.49, the analyst price target of $157.87 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AGCO?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.