Last Update 17 Nov 25

Fair value Decreased 0.94%SCCO: Delays At Tia Maria Will Likely Limit Upside Despite Sector Momentum

Southern Copper's analyst price target has been marginally revised down from $118.88 to $117.76, as analysts factor in a higher discount rate and recent shifts in commodity price forecasts.

Analyst Commentary

Recent Street research reveals a wide range of analyst opinions on Southern Copper, highlighting both optimism regarding copper market dynamics and caution around execution and valuation challenges.

Bullish Takeaways

- Bullish analysts have raised their price targets, in some cases substantially, as copper and precious metal prices reach multi-decade highs. Supply disruptions are also supporting stronger pricing.

- The outlook for 2025 and 2026 earnings has improved, with analysts increasing EBITDA estimates in response to updated expectations for the global copper market and Southern Copper's parent company.

- Expectations for robust free cash flow continue, supporting the company's ability to sustain its attractive dividend policy. This policy includes both cash and stock components.

- Some analysts now anticipate tightening supply in the copper market through 2026. The company is seen as well-positioned to benefit from restricted supply and elevated prices.

Bearish Takeaways

- Bearish analysts express concern over execution risks, particularly referencing project delays such as those at Tia Maria. These delays could affect earnings in future years.

- Valuation remains a key focal point for caution. Some analysts note that shares are trading at elevated levels compared to peers, which may limit near-term upside.

- There are references to continued Sell ratings, with skepticism about whether strong commodity pricing is sufficient to offset operational and project-specific headwinds.

- Parent company developments and external factors, such as bids for unrelated assets, are viewed as possible contributors to a heightened valuation discount in the near term.

What's in the News

- The U.S. Department of the Interior has added copper, silver, and metallurgical coal to its "critical minerals" list. This move could lead to changes in tariff policies affecting Southern Copper (Financial Times).

- Southern Copper's Board of Directors has authorized a quarterly cash dividend of $0.90 per share and a stock dividend of 0.0085 shares per share. Both dividends are payable on November 28, 2025, to shareholders of record on November 12, 2025.

- The company reported third-quarter copper production of 234,892 tonnes, a decrease from 252,219 tonnes last year. In contrast, zinc and silver output increased year-over-year.

- Southern Copper completed the repurchase of approximately 119.5 million shares, representing 13.68% of total shares, under its buyback program.

Valuation Changes

- Consensus Analyst Price Target has been revised down marginally from $118.88 to $117.76.

- Discount Rate has risen slightly, increasing from 7.66% to 8.14%.

- Revenue Growth projections remain virtually unchanged at approximately 4.80%.

- Net Profit Margin estimates are stable, with a negligible change from 31.40% to 31.40%.

- Future P/E ratio forecast has increased modestly, moving from 27.02x to 27.36x.

Key Takeaways

- Substantial capital investments and efficient operations are expected to drive significant production growth, enhancing revenue and net margins.

- Tight market conditions and low inventory levels may boost copper prices, positively impacting Southern Copper's revenue and profitability.

- Southern Copper is vulnerable to U.S.-China tensions, rising costs, and operational disruptions, risking revenue and margins despite planned significant capital expenditure.

Catalysts

About Southern Copper- Engages in mining, exploring, smelting, and refining copper and other minerals in Peru, Mexico, Argentina, Ecuador, and Chile.

- Southern Copper has announced substantial capital investments totaling over $15 billion, including projects in Mexico and Peru, which are expected to drive future production growth and potentially boost revenue significantly.

- The company's Buenavista zinc concentrator is now operating at full capacity, anticipated to drive a 31% increase in zinc production in 2025, likely enhancing revenues and improving net margins due to efficient operations.

- Expansion projects such as Tia Maria, Los Chancas, and Michiquillay are progressing, with expectations for additional production capacity, which could positively impact revenue and earnings starting in 2027 through 2030.

- Operational efficiencies and a strong focus on cost control have led to a reduction in cash costs, with expectations to sustain low costs between $0.75 to $0.80 per pound of copper in 2025, potentially boosting net margins and earnings.

- Tight copper market conditions, with expectations of supply-demand deficits and low inventory levels, could maintain or increase copper prices, positively impacting Southern Copper's revenue and profitability.

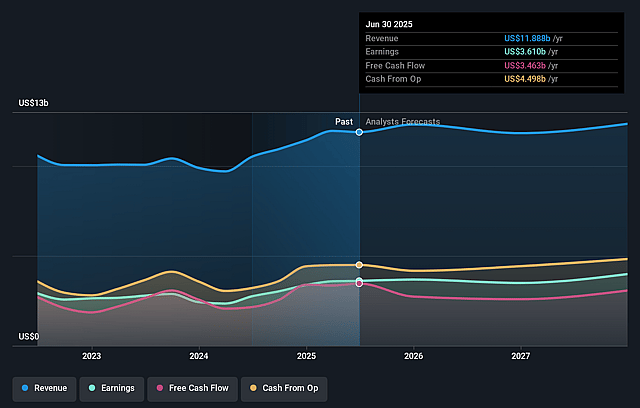

Southern Copper Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Southern Copper's revenue will grow by 3.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 30.4% today to 33.3% in 3 years time.

- Analysts expect earnings to reach $4.3 billion (and earnings per share of $5.24) by about September 2028, up from $3.6 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $4.8 billion in earnings, and the most bearish expecting $3.5 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.2x on those 2028 earnings, down from 22.5x today. This future PE is lower than the current PE for the US Metals and Mining industry at 22.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.57%, as per the Simply Wall St company report.

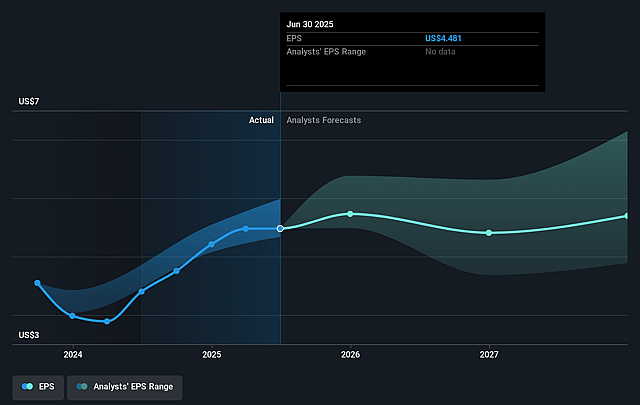

Southern Copper Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Southern Copper faces the risk of an intense commercial war between the U.S. and China, which could adversely affect global economic growth and subsequently reduce copper demand. This could potentially impact revenue and earnings.

- The significant arbitrage difference between COMEX and LME prices, largely driven by the potential for a 25% tariff on U.S. imports, presents uncertainty. If such tariffs are implemented, they could affect Southern Copper’s ability to sell profitably in the U.S. market, impacting revenue and profit margins.

- An increase in operating costs and expenses, which rose by 12% due to factors like inventory consumption and material costs, may hurt net margins despite sales growth.

- The company's significant capital expenditure plans over the next decade, exceeding $15 billion, could pressure cash flow and require careful financial management to maintain profitability.

- Community issues and disruptions, such as the incidents with illegal miners at the Los Chancas project, pose operational risks and could delay project timelines, adversely affecting future production and revenue projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $95.247 for Southern Copper based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $128.7, and the most bearish reporting a price target of just $66.63.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $13.0 billion, earnings will come to $4.3 billion, and it would be trading on a PE ratio of 22.2x, assuming you use a discount rate of 7.6%.

- Given the current share price of $99.91, the analyst price target of $95.25 is 4.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.