Last Update 09 Jun 26

Fair value Increased 0.36%SCCO: Rich P E And ESG Headwinds Will Shape Balanced Future Returns

Analysts have nudged their fair value estimate for Southern Copper slightly higher to about $163 per share, reflecting updated assumptions that temper revenue growth and margins while recognizing the stock's elevated P/E and the recent wave of Underweight and Sell ratings tied to concerns about a stretched valuation.

Analyst Commentary

Recent research on Southern Copper shows a crowded field of views, with several firms updating price targets and ratings in a short span. The common thread is that the stock screens as high quality operationally, but with a valuation that many see as rich versus copper peers.

Across these reports, you see a mix of cautious and more constructive takes, often within tight price target bands, as analysts weigh the company’s low cost profile and reserve depth against concerns about how much of that story is already reflected in the share price.

Bullish Takeaways

- Bullish analysts point to Southern Copper as a global leader in copper production, citing a low cost operations base and an extensive reserve portfolio as core supports for long term execution.

- The company’s growth pipeline is repeatedly highlighted, with supporters arguing that existing and planned projects help justify a premium P/E multiple versus many copper peers.

- Income focused investors are likely to focus on the stock’s high yielding dividend, which bullish analysts see as an added support to total return potential when compared with other metals producers.

- Even some cautious firms have adjusted price targets higher, which signals recognition of improved inputs in their models rather than a purely negative stance on the company’s fundamentals.

Bearish Takeaways

- Bearish analysts frequently describe the valuation premium as stretched relative to both large cap and small cap copper peers. They argue that current prices embed optimistic assumptions on copper markets and company execution.

- Several firms maintain Underweight, Underperform or Sell ratings despite upward tweaks to targets. This indicates ongoing concern that the risk reward skew is unfavorable at current levels.

- Some research frames Southern Copper within a broader sector view that favors other stocks in copper and metals. This effectively positions Southern Copper as a funding source rather than a preferred way to gain exposure.

- Target ranges in the US$135 to US$148 zone sit well below the recent trading level cited around US$178.49. This underscores the gap between what cautious analysts see as fair value and the price investors are currently paying.

What's in the News

- Communities affected by the 2014 spill of 40 million liters of toxic waste into the Sonora and Bacanuchi rivers by Buenavista del Cobre, owned by Grupo Mexico, are urging investors ahead of the 2026 AGMs of Grupo Mexico and Southern Copper to press for a concrete remediation plan and stronger tailings dam safety standards. (Source: community and NGO communications, May 26, 2026)

- Several banks, including UBS and Scotiabank, raised their price targets on Southern Copper in May while keeping Sell or Underperform ratings, citing ongoing political, social and regulatory risks in Peru and Mexico, even as copper demand linked to electrification and green energy remains a key part of the investment debate. (Source: broker research roundup, May 26, 2026)

- Southern Copper shares recently came under pressure as copper prices fell sharply and investors weighed uncertainty tied to potential changes in U.S. Section 232 tariff rules on metals imports, which could affect trade flows and pricing for producers. (Source: market reports, June 5, 2026)

- The Board appointed Leonardo Contreras Lerdo de Tejada as interim Chief Executive Officer effective April 16, 2026, and then as Chief Executive Officer on April 23, 2026, following the unexpected passing of long serving CEO and President Oscar Gonzalez Rocha on April 7, 2026. (Source: company announcements, April 2026)

- For the first quarter ended March 31, 2026, Southern Copper reported total copper mined of 230,544 tonnes, molybdenum of 7,516 tonnes, zinc of 40,164 tonnes and silver of 6,047,000 ounces, and also declared a 1.01% stock dividend dated May 13, 2026. (Source: company operating results and corporate actions, Q1 2026)

Valuation Changes

- Fair Value: The fair value estimate has risen slightly from about $162.54 to about $163.13 per share.

- Discount Rate: The discount rate assumption has risen slightly from about 8.55% to about 8.65%.

- Revenue Growth: The long term annual revenue growth input has been reduced from about 4.84% to about 4.26%.

- Net Profit Margin: The forecast net profit margin has been trimmed from about 36.70% to about 36.41%.

- Future P/E: The future P/E multiple applied in the model has increased from about 27.9x to about 29.1x.

Key Takeaways

- Substantial capital investments and efficient operations are expected to drive significant production growth, enhancing revenue and net margins.

- Tight market conditions and low inventory levels may boost copper prices, positively impacting Southern Copper's revenue and profitability.

- Southern Copper is vulnerable to U.S.-China tensions, rising costs, and operational disruptions, risking revenue and margins despite planned significant capital expenditure.

Catalysts

About Southern Copper- Engages in mining, exploring, smelting, and refining copper and other minerals in Peru, Mexico, Argentina, Ecuador, and Chile.

- Southern Copper has announced substantial capital investments totaling over $15 billion, including projects in Mexico and Peru, which are expected to drive future production growth and potentially boost revenue significantly.

- The company's Buenavista zinc concentrator is now operating at full capacity, anticipated to drive a 31% increase in zinc production in 2025, likely enhancing revenues and improving net margins due to efficient operations.

- Expansion projects such as Tia Maria, Los Chancas, and Michiquillay are progressing, with expectations for additional production capacity, which could positively impact revenue and earnings starting in 2027 through 2030.

- Operational efficiencies and a strong focus on cost control have led to a reduction in cash costs, with expectations to sustain low costs between $0.75 to $0.80 per pound of copper in 2025, potentially boosting net margins and earnings.

- Tight copper market conditions, with expectations of supply-demand deficits and low inventory levels, could maintain or increase copper prices, positively impacting Southern Copper's revenue and profitability.

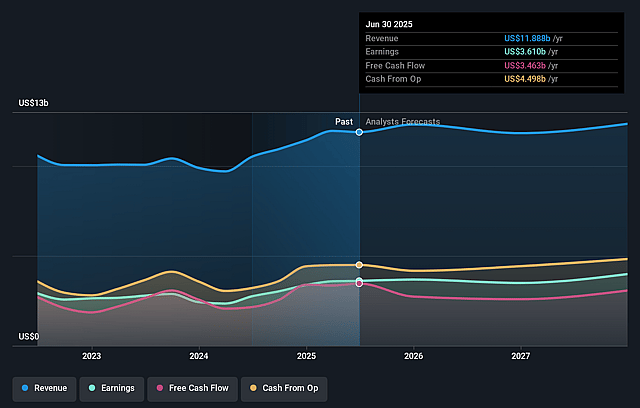

Southern Copper Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Southern Copper's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 34.1% today to 36.4% in 3 years time.

- Analysts expect earnings to reach $6.0 billion (and earnings per share of $6.9) by about June 2029, up from $5.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $6.7 billion in earnings, and the most bearish expecting $4.9 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.1x on those 2029 earnings, up from 28.6x today. This future PE is greater than the current PE for the US Metals and Mining industry at 19.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.65%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Southern Copper faces the risk of an intense commercial war between the U.S. and China, which could adversely affect global economic growth and subsequently reduce copper demand. This could potentially impact revenue and earnings.

- The significant arbitrage difference between COMEX and LME prices, largely driven by the potential for a 25% tariff on U.S. imports, presents uncertainty. If such tariffs are implemented, they could affect Southern Copper’s ability to sell profitably in the U.S. market, impacting revenue and profit margins.

- An increase in operating costs and expenses, which rose by 12% due to factors like inventory consumption and material costs, may hurt net margins despite sales growth.

- The company's significant capital expenditure plans over the next decade, exceeding $15 billion, could pressure cash flow and require careful financial management to maintain profitability.

- Community issues and disruptions, such as the incidents with illegal miners at the Los Chancas project, pose operational risks and could delay project timelines, adversely affecting future production and revenue projections.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $163.13 for Southern Copper based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $232.67, and the most bearish reporting a price target of just $125.74.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $16.5 billion, earnings will come to $6.0 billion, and it would be trading on a PE ratio of 29.1x, assuming you use a discount rate of 8.6%.

- Given the current share price of $170.48, the analyst price target of $163.13 is 4.5% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Southern Copper?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.