Last Update 01 Aug 26

Fair value Increased 19%PRCH: Excess Insurance Capital Will Support Future Underwriting And Coverage Upside

Analysts have lifted their average price target on Porch Group to about $19.42 from $16.25, citing updated views on fair value, discount rate, revenue growth, profit margin and future P/E assumptions based on recent research commentary.

Analyst Commentary

Recent research on Porch Group highlights a mix of optimism about the company’s long term potential and caution around what the current share price already reflects. Analysts are weighing the stock’s sharp move in recent months against factors like execution risk, insurance capital and underwriting performance.

Bullish Takeaways

- Bullish analysts point to Porch Group’s access to what they describe as ample excess insurance capital, which they see as a support for growth plans and product expansion over time.

- There is a view that Porch Group has underwriting advantages. Supportive analysts see this as a potential edge for unit economics and future profitability as the business scales.

- Some research commentary still describes Porch Group’s long term story in favorable terms, suggesting confidence in the business model even as shorter term expectations are reset.

- The lift in the average price target to about US$19.42 from US$16.25 reflects updated thinking on fair value that incorporates assumptions around revenue growth, profit margins and future P/E levels.

Bearish Takeaways

- Bearish analysts describe the recent share price move, including a 116% rally in the last three months referenced in research, as leaving a more balanced risk and reward profile compared with earlier this year.

- There is a view that the current valuation sets a higher bar for execution. Porch Group may need to hit ambitious operational and financial milestones to justify recent price targets.

- Some commentary pairs a rating downgrade with a higher price target. That combination signals that, while the business case is still viewed positively, the room for upside from today’s level is seen as more limited without further evidence of delivery.

- Analysts caution that any stumble in underwriting performance or use of insurance capital could put pressure on the assumptions embedded in current revenue growth, margin and P/E forecasts.

What’s in the News for Porch Group

- Porch Group, through its Homeowners of America subsidiary, announced an expansion into Michigan, which is the 22nd state in which HOA operates. Source: company key developments filing.

- The Michigan launch is described as supporting Porch Group’s broader plan to widen insurance distribution and pursue premium growth through its insurance platform over time. Source: company key developments filing.

- Management also links the Michigan entry to goals around building insurance related cash flow as the platform footprint increases. Source: company key developments filing.

Valuation Changes for Porch Group

- Fair value has risen moderately, with the average target moving from $16.25 to about $19.42 per share.

- The discount rate has edged lower, shifting from 9.39% to about 9.21%, which slightly reduces the implied required return in the updated models.

- Revenue growth assumptions are higher, moving from about 10.48% to roughly 12.32% in the latest research inputs.

- Profit margin expectations have been lifted, changing from about 7.62% to roughly 11.05% in the updated framework.

- The future P/E has been marked down, moving from about 52.3x to roughly 43.7x, which points to a lower multiple being used in the current valuation work.

Key Takeaways

- Porch Group's shift to a fee-based insurance model and formation of PIRE create a higher-margin, more predictable earnings structure.

- Strategic investments in software, data, and new geographies aim to boost future revenue and EBITDA growth, leveraging products like Home Factors.

- Porch Group faces potential revenue volatility and execution risks due to delayed initiatives and a transition to a commission-based model, impacting future earnings and growth.

Catalysts

About Porch Group- Operates a vertical software and insurance platform in the United States.

- Porch Group's transition to a fee-based, higher-margin model in insurance services should enhance gross margins to about 80% in 2025, making earnings more predictable and less impacted by weather volatility, thereby improving net margins.

- The formation of the Porch Insurance Reciprocal Exchange (PIRE) and the sale of Homeowners of America (HOA) Insurance Carrier into PIRE create a more predictable and higher-margin financial model, which could lead to improved earnings.

- Porch Group's strategic plans include reopening geographies and reactivating distribution partners, contributing to expected growth in gross written premiums, which could drive revenue and adjusted EBITDA growth.

- The company is investing in expanding its Vertical Software and data businesses, with initiatives such as new product launches and increased sales and product investments poised to drive faster revenue growth in 2026 and beyond.

- The introduction and expected growth of Home Factors, a data product which aids in risk selection and pricing, present new revenue opportunities and could significantly enhance the value of Porch Group's data segment, thereby impacting future revenue growth.

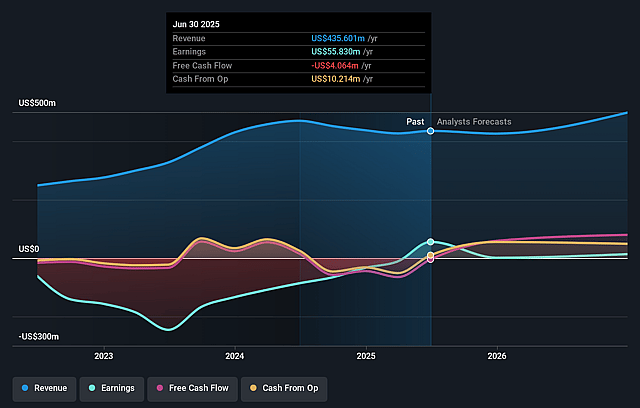

Porch Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Porch Group's revenue will grow by 12.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -2.6% today to 11.1% in 3 years time.

- Analysts expect earnings to reach $80.4 million (and earnings per share of $0.38) by about August 2029, up from -$13.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 43.7x on those 2029 earnings, up from -122.0x today. This future PE is greater than the current PE for the US Software industry at 28.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.21%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Porch Group's revenue in Q4 2024 decreased by 12% year-over-year due to nonrecurring items and the sale of their legacy agency, EIG, which could indicate potential volatility in future revenues.

- The formation of the Porch Insurance Reciprocal Exchange (PIRE) and sale of their Homeowners of America Insurance Carrier were delayed longer than anticipated, signaling potential execution risks which may impact revenue predictability.

- The company’s transition to a commission and fee-based insurance services model could result in lower revenue year-over-year, suggesting potential challenges in offsetting the reduction with higher margins.

- While Porch Group’s strategic price increases in their Vertical Software business showed a 6% growth, it could face challenges in maintaining these growth levels if the housing market does not stabilize, which could impact net margins.

- Porch's ambitious targets for growth in the homeowners insurance market and the new Home Factors product depend heavily on execution and adoption by third-party carriers. Delays or difficulties in realization of these strategies could adversely impact earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $19.42 for Porch Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $23.0, and the most bearish reporting a price target of just $16.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $727.9 million, earnings will come to $80.4 million, and it would be trading on a PE ratio of 43.7x, assuming you use a discount rate of 9.2%.

- Given the current share price of $14.45, the analyst price target of $19.42 is 25.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Porch Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.