Last Update 28 May 26

Fair value Increased 4.25%FANG: Higher Oil Decks And Cash Returns Will Drive Future Repricing Potential

Analysts have nudged the fair value estimate for Diamondback Energy higher to about $232 per share from roughly $223, pointing to a series of price target hikes that lean on firmer medium term oil price assumptions and expectations for stronger margins and earnings, which are reflected in lower forward P/E estimates.

Analyst Commentary

Street research on Diamondback Energy has tilted more constructive, with a series of higher price targets clustered around the low to mid US$200s. Most of the recent updates tie fair value more closely to higher crude price assumptions, tighter supply expectations, and company specific execution on capital plans.

At the same time, a few voices are more measured, pointing to valuation and the stock’s recent run as reasons to temper enthusiasm. Taken together, the commentary gives you a mix of optimism on earnings power and cash returns, balanced by concern about how much of that story is already reflected in the share price.

Bullish Takeaways

- Bullish analysts are lifting price targets into a US$220 to US$248 range, reflecting the view that current market pricing does not fully capture Diamondback’s earnings potential under firmer medium term oil assumptions.

- Several research notes point to higher 2026 and 2027 oil price decks and tighter global supply, which feed directly into stronger margin and cash flow forecasts for oil weighted producers like Diamondback.

- Commentary highlights company execution on a disciplined plan, including references to a growing base dividend and operational flexibility supported by inventory depth and a DUC backlog, which supports confidence in future cash return capacity.

- Some bullish analysts describe a disconnect between oil linked equities and crude price expectations, arguing that this gap could support further rerating for exploration and production stocks, with Diamondback cited as a key beneficiary.

Bearish Takeaways

- Bearish analysts flag valuation as a key concern, with at least one downgrade to Hold that cites limited upside from current levels, even after acknowledging sector moves and recent results.

- There is caution that, despite target hikes, the stock’s recent rally in the exploration and production sector may have already captured a meaningful portion of the improved macro and pricing outlook.

- One research note characterizes recent quarterly performance as unremarkable, which can lead more cautious analysts to question how much additional multiple expansion is justified without a clearer acceleration in growth.

- Some commentary references a "yellow light" backdrop for the sector, suggesting that while execution is on plan, broader risk considerations still matter for how aggressively investors may be willing to pay up for future growth.

What's in the News

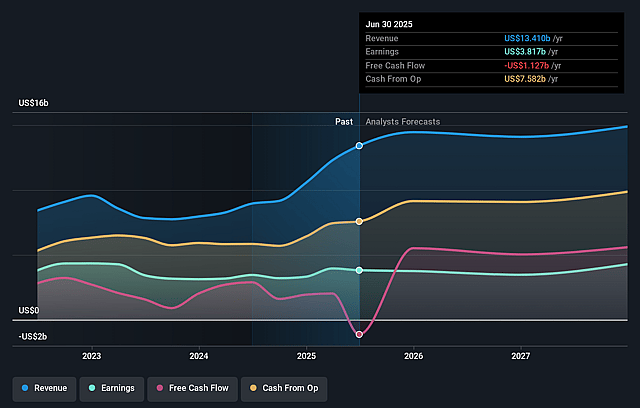

- Reported a US$1.4b impairment of oil and natural gas properties for the first quarter of 2026, which affects reported earnings even though it is a non cash accounting charge tied to asset values. (Key Developments)

- Announced a 5% increase to the base cash dividend to US$1.10 per common share for the first quarter of 2026, payable on May 21, 2026, to stockholders of record on May 14, 2026. (Key Developments)

- Released first quarter 2026 operating results, with reported oil, natural gas and NGL volumes and combined daily production levels that inform how the company is using its asset base. (Key Developments)

- Updated 2026 guidance, with higher annual oil and total BOE production targets and a second quarter range for oil and total volumes that gives you a reference point for near term execution. (Key Developments)

- Completed several capital markets moves, including a share repurchase tranche totaling 3,267,000 shares since January 1, 2026 under a broader 41,689,880 share buyback program, and a US$1.903b follow on equity offering of 11,000,000 common shares that interacts with that buyback activity. (Key Developments)

Valuation Changes

- Fair Value: updated to about $232.17 per share from roughly $222.70, a small upward move in the intrinsic value estimate.

- Discount Rate: increased slightly to 7.11% from 6.98%, indicating a modestly higher required return in the valuation model.

- Revenue Growth: revised to 4.47% from 3.05%, a moderate step up in the projected top line growth rate.

- Net Profit Margin: now modeled at 29.95% versus 27.07% previously, a moderate increase in expected earnings efficiency on each dollar of revenue.

- Future P/E: adjusted down to 14.91x from 16.29x, suggesting a somewhat lower earnings multiple in the updated framework.

Key Takeaways

- Successful Permian Basin consolidation and operational efficiency drive sustainable cost reductions, higher margins, and resilient cash flow amid oil market volatility.

- Strategic asset sales and disciplined capital allocation strengthen the balance sheet, reduce risk, and set the stage for enhanced shareholder returns and production growth.

- Rising operating costs, lower quality drilling inventory, oil price volatility, diminishing efficiency gains, and limited quality acquisitions threaten long-term profitability and revenue growth.

Catalysts

About Diamondback Energy- An independent oil and natural gas company, acquires, develops, explores, and exploits unconventional, onshore oil and natural gas reserves in the Permian Basin in West Texas.

- Ongoing consolidation in the Permian Basin, with Diamondback positioned as the "consolidator of choice" due to its industry-best integration, low cost structure, and ability to deliver synergies from recent large acquisitions (e.g., Double Eagle, Endeavor), supports future growth in scale, cost savings, and higher EBITDA margins.

- Consistent operational efficiency improvements (record drilling times, workover programs, optimization of older wells, and improved gas capture) point to sustainable cost reductions and productivity enhancements, supporting resilient net margins and robust free cash flow even in a volatile oil price environment.

- Anticipated noncore asset sales (targeting $1.5 billion), debt paydown, and enhanced balance sheet flexibility will lower interest expenses, reduce financial risk, and ultimately enable increased shareholder returns via buybacks/dividends, directly impacting future EPS and total returns.

- The company's ability to exploit emerging zones within its existing acreage (such as Wolfcamp B/D and others) without performance degradation, combined with the long-term, favorable trend of underinvestment and growing global oil demand, supports stable or growing production volumes and revenue over the next several years.

- Diamondback's focus on domestic energy security and operational discipline aligns with growing policy support and infrastructure investment, helping maintain or expand market share, and positioning the company to benefit disproportionately from secular demand for reliable U.S. oil supply-positively impacting long-term revenue and earnings resilience.

Diamondback Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Diamondback Energy's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.9% today to 29.9% in 3 years time.

- Analysts expect earnings to reach $4.9 billion (and earnings per share of $18.61) by about May 2029, up from $279.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $7.7 billion in earnings, and the most bearish expecting $4.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.9x on those 2029 earnings, down from 194.4x today. This future PE is greater than the current PE for the US Oil and Gas industry at 13.8x.

- Analysts expect the number of shares outstanding to decline by 2.82% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Increasing water management and disposal costs, coupled with electricity and power inflation in the Permian Basin, could significantly raise Diamondback's long-term operating expenses (LOE), thereby pressuring net margins and EBITDA.

- The company's development mix is increasingly shifting toward secondary and non-core zones as top-tier acreage becomes scarcer, risking declining well productivity and higher per-barrel costs in the future, which may erode long-term earnings resilience.

- Persistent uncertainty around oil price volatility and macroeconomic headwinds-combined with significant exposure to commodity price swings due to a less robust hedge position for 2026 and beyond-could impair future revenues, free cash flow, and the sustainability of shareholder returns if prices fall.

- Industry-wide efficiency gains and cost reductions are showing signs of plateauing, while supply chain risks (such as casing tariffs and steel cost inflation) could limit further margin improvements, challenging Diamondback's ability to maintain its cost leadership and robust capital efficiency over the long term.

- Limited inventory of high-quality, accretive acquisition targets in the Permian and growing competition among consolidators heighten the risk that future M&A will be either value-dilutive or unattainable, leading to slower production growth, less scale advantage, and increased reliance on organic opportunities which may yield lower returns and impact long-term revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $232.17 for Diamondback Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $277.0, and the most bearish reporting a price target of just $195.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $16.5 billion, earnings will come to $4.9 billion, and it would be trading on a PE ratio of 14.9x, assuming you use a discount rate of 7.1%.

- Given the current share price of $192.84, the analyst price target of $232.17 is 16.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Diamondback Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.