Last Update 04 Aug 26

Fair value Increased 2.27%DRS: AI Mission Software Acquisition Will Support Future Earnings Upside

Analysts have nudged their price targets for Leonardo DRS higher, with recent Street research moves supporting a shift in fair value to about $54.10 from $52.90 as they factor in updated assumptions on the discount rate, profit margin, and future P/E expectations.

Analyst Commentary

Recent research around Leonardo DRS gives investors a mix of supportive and cautious signals, with price targets such as the US$53 level from JPMorgan helping frame how analysts think about valuation, execution, and growth expectations today.

Bullish Takeaways

- Bullish analysts see the move to price targets around US$53 as consistent with their updated view of fair value for Leonardo DRS, given current assumptions on discount rates and profit margins.

- Some research points to improved confidence in the company’s ability to execute on its current backlog and program commitments, which feeds into higher earnings assumptions and P/E inputs.

- The clustering of targets in the low to mid US$50 range is viewed by bullish analysts as support for a more constructive stance on the stock’s medium term potential, without relying on aggressive growth assumptions.

- Supportive commentary around the existing business mix suggests that, in the eyes of bullish analysts, Leonardo DRS has a foundation they consider suitable for maintaining current valuation multiples.

Bearish Takeaways

- The Neutral rating maintained alongside the US$53 JPMorgan target signals that some analysts remain cautious about upside from current levels, even with higher fair value estimates.

- More conservative analysts highlight dependency on current profit margin assumptions, and see limited room for error if execution on key programs or contracts falls short.

- There is ongoing focus on how future P/E expectations are set, with bearish analysts questioning whether the present multiples fully account for potential cost pressures or delays.

- The relatively modest adjustment in price targets is read by cautious research teams as an indication that risk and reward appear balanced, rather than clearly skewed in favor of Leonardo DRS.

What’s in the News for Leonardo DRS

- Leonardo DRS agreed to acquire Raft LLC, a Virginia based defense technology firm focused on open architecture mission software that uses artificial intelligence and multi domain data fusion, in an all cash deal valued at US$450 million. Management describes the move as part of the shift toward being an integrated solutions provider that pairs software with existing sensing and tactical radar offerings. Source: company announcement.

- The Raft transaction is described as expected to be accretive to adjusted diluted earnings per share in the first full year after closing, with completion targeted for the fourth quarter of 2026, subject to regulatory approvals. Source: company announcement.

- Leonardo DRS reaffirmed earnings guidance for 2026 and now expects revenue in a range of US$3.9b to US$3.975b. Source: corporate guidance update.

- From 1 April 2026 to 30 June 2026, Leonardo DRS repurchased 261,526 shares for US$12 million. This brought total buybacks under the February 20, 2025 program to 1,246,056 shares for US$50.9 million, or 0.47% of shares. Source: buyback tranche update.

- Leonardo DRS announced a contract to supply more than 50,000 Tenum Orbit thermal imaging cameras under a blanket purchase agreement, as well as the launch of the Tenum 640 Orbit uncooled long wave infrared camera module for unmanned air, ground, and maritime platforms. The module is aimed at high volume production and exportable use across multiple end markets. Source: product and client announcements.

Valuation Changes for Leonardo DRS

- Fair Value has risen slightly, with the central estimate moving from $52.90 to $54.10.

- The Discount Rate is marginally lower, shifting from 7.90% to about 7.87%.

- Revenue Growth is slightly lower in the updated model, moving from about 7.08% to roughly 6.96%.

- The Profit Margin is set higher, moving from about 9.55% to roughly 10.02%.

- The Future P/E is set lower, moving from about 41.12x to roughly 39.42x in the latest assumptions.

Key Takeaways

- Alignment with defense modernization and geopolitical trends supports premium contracts, expanded programs, and diverse international growth opportunities.

- Increased R&D and proprietary technologies drive innovation, margin improvement, and competitive positioning in high-value defense sectors.

- Raw material constraints, rising costs, and reliance on key government contracts create margin, revenue, and growth risks amid intensifying competition and challenging M&A conditions.

Catalysts

About Leonardo DRS- Provides defense electronic products and systems, and military support services worldwide.

- Anticipated increases in U.S. and allied defense budgets-with substantial front-loaded funding and new NATO commitments-are expected to drive persistent and potentially accelerating demand for advanced defense technologies, positioning Leonardo DRS for strong multiyear revenue growth and increasing backlog.

- The company's strategic alignment with national priorities-including investments in naval modernization, next-generation air and missile defense (such as the Golden Dome initiative), and counter-UAS capabilities-sets the stage for premium contract awards and program expansions, benefiting both revenue and net margins over the next several years.

- Leonardo DRS is increasing its R&D investment to accelerate innovation in critical areas such as space sensing, advanced infrared technologies, and force protection, which should support the company's competitive positioning and allow for participation in higher-margin, next-generation defense programs-improving long-term earnings and margin trajectories.

- Global increases in digitization and modernization of military forces are benefiting DRS's proprietary solutions in network computing, electronic warfare, and electric propulsion, supporting higher average selling prices and expanded platform content, which is expected to enhance net margins and drive operational leverage.

- The company's growing international exposure-particularly in response to NATO's elevated defense spending targets and geopolitical tensions-presents a catalyst for above-average international sales growth and greater revenue diversification, mitigating dependency on the U.S. budget cycle and increasing total addressable market.

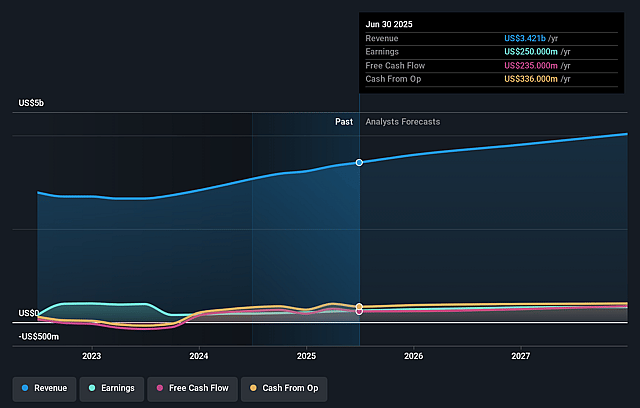

Leonardo DRS Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Leonardo DRS's revenue will grow by 7.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.5% today to 10.0% in 3 years time.

- Analysts expect earnings to reach $463.4 million (and earnings per share of $1.66) by about August 2029, up from $322.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 39.4x on those 2029 earnings, up from 37.5x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 37.7x.

- Analysts expect the number of shares outstanding to grow by 0.29% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.87%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heightened germanium supply constraints and escalating raw material costs, driven by Chinese export restrictions and slow ramp-up of alternative sources, are compressing margins in the Advanced Sensing and Computing business; prolonged supply issues or cost inflation could negatively affect program execution, delay deliveries, and reduce net margins.

- Increasing R&D intensity (from 2.8% to 3.5% of revenue) in response to evolving customer demands and market competition is creating a sustained headwind to operating margins, and if these investments do not result in contract wins or product adoption, long-term earnings growth and margin expansion could be impaired.

- The company's revenue streams are highly concentrated in large, long-term U.S. government contracts (e.g., Columbia-class), making them vulnerable to future shifts in federal defense budgets, delayed appropriations, or shifting administration priorities, which could suppress both revenue growth and backlog visibility.

- Rising valuations in the defense sector are making accretive M&A more difficult, while ongoing or future integration of acquired businesses and potential expansion into partnerships present ongoing execution and margin risks-missteps could result in increased SG&A costs and jeopardize projected EPS growth.

- Government and customer hesitancy over greater European defense industrial base investments and an emerging preference for indigenous capabilities may limit Leonardo DRS's ability to fully capitalize on NATO and European defense spending increases, potentially restricting international revenue growth despite favorable macro trends.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $54.1 for Leonardo DRS based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $59.0, and the most bearish reporting a price target of just $47.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.6 billion, earnings will come to $463.4 million, and it would be trading on a PE ratio of 39.4x, assuming you use a discount rate of 7.9%.

- Given the current share price of $45.27, the analyst price target of $54.1 is 16.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Leonardo DRS?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.