Last Update 18 Jun 26

BRC: Future Upside Will Rely On New CEO And Firm Earnings Guidance

Analysts have kept their average price target for Brady broadly unchanged at $101.50, citing stable fair value estimates and only slight adjustments to long term P/E assumptions, rather than any major shift in the outlook.

What’s in the News for Brady

- Brady Corporation appointed Vineet Nargolwala as CEO effective June 8, 2026, succeeding retiring CEO Russell Shaller. Shaller will remain in a consultative role until August 1, 2026. (Source: company announcement, multiple news reports)

- The board highlighted Nargolwala’s prior CEO experience at Allegro MicroSystems and his background at Sensata Technologies and Honeywell. It also noted his involvement in assessing Brady’s planned acquisition of Honeywell’s Productivity Solutions and Services business. (Source: company announcement)

- Shortly after taking the CEO role, Nargolwala bought 13,011 Brady shares in the open market, an insider purchase of around US$1 million that lifted his direct holdings to 78,393 shares. (Source: multiple news reports)

- The CEO transition was followed by a 10.4% decline in Brady’s share price, reflecting investor uncertainty around the leadership change. (Source: multiple news reports)

- Brady updated its earnings guidance for the year ending July 31, 2026, to a range of US$4.66 to US$4.76 per diluted Class A Nonvoting Common Share, compared with the prior range of US$4.62 to US$4.82. The company also reported that it has repurchased 4,095,932 shares, or 8.39% of its stock, for US$227.18 million under its buyback program. (Source: company guidance and buyback update)

Valuation Changes for Brady

- Fair Value: The fair value estimate for Brady stock is unchanged at $101.50, indicating no shift in the overall valuation anchor.

- Discount Rate: The discount rate remains effectively steady at 7.108%, with only an immaterial rounding adjustment.

- Revenue Growth: The modeled long term revenue growth assumption stays almost identical at 30.14%, with only a negligible numerical refinement.

- Net Profit Margin: The projected net profit margin is effectively unchanged at 10.12%, reflecting only a minor technical adjustment.

- Future P/E: The future P/E assumption has risen slightly from 15.85x to 16.19x, indicating a modestly higher multiple applied to Brady’s earnings in the valuation model.

Key Takeaways

- Strong R&D investments and strategic acquisitions are driving growth in automation, traceability, and compliance solutions, expanding Brady's presence in higher-margin markets.

- Operational improvements and global expansion, especially in high-growth regions, are enhancing profitability and providing diversified, resilient revenue streams.

- Brady's reliance on cost-cutting and legacy product demand, amid rising trade barriers, slow growth, and competitive pressures, threatens long-term revenue and margin sustainability.

Catalysts

About Brady- Manufactures and supplies identification solutions and workplace safety products that identify and protect premises, products, and people in the Americas, Asia, Europe, and Australia.

- Brady's consistent and increasing investment in R&D-especially the recent record spend and focus on high-performance, engineered products (such as the i7500 industrial printer and microfluidics platform)-positions the company to capture a greater share of demand from automation, IoT, and digital transformation initiatives in industrial, healthcare, and manufacturing sectors, setting up for sustained organic revenue growth and higher gross margins.

- The company's deepening product ecosystem and recent acquisitions (Gravotech, Funai Microfluidics, Mecco) expand capabilities in direct part marking, barcode/RFID solutions, and software integration, directly addressing rising global requirements for traceability, regulatory compliance, and asset tracking; this supports entry into higher-growth, higher-margin markets and drives recurring revenue streams.

- Operational efficiency initiatives-including facility closures, workforce reductions, cost structure realignment, and supply chain optimizations-are expected to significantly enhance profitability and support operating margin expansion as tariff headwinds are offset and integration synergies are realized.

- Brady's ongoing global expansion, especially robust organic growth in the Americas and Asia (with Asia ex-China up 23% in the latest quarter), leverages secular growth in emerging markets and the continued buildout of industries such as data centers, aerospace, and utilities, laying a foundation for diversified and resilient top-line growth.

- The rising demand for ESG, safety, and compliance solutions across industries-combined with Brady's growing ability to offer complete, customized identification systems-positions the company to benefit from long-term secular increases in regulatory and workplace safety spend, supporting both revenue growth and durable net margin expansion.

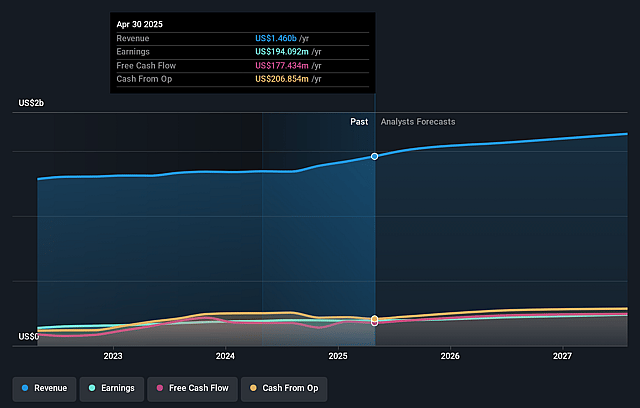

Brady Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Brady's revenue will grow by 30.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 12.9% today to 10.1% in 3 years time.

- Analysts expect earnings to reach $362.0 million (and earnings per share of $7.48) by about June 2029, up from $208.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.3x on those 2029 earnings, down from 18.8x today. This future PE is lower than the current PE for the US Commercial Services industry at 21.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Brady faces persistent challenges from tightening global trade policies and rising tariffs-estimated at $8 to $12 million incremental impact in FY26-which could erode operating margins if mitigation efforts and price increases are not fully effective or if trade policies worsen, impacting future earnings and profitability.

- Organic sales growth remains low single digits, and there is ongoing organic decline in key regions such as Europe and Australia, raising concerns about long-term revenue stagnation, especially if macroeconomic weakness persists in these mature markets and limits new growth opportunities.

- A significant portion of Brady's revenue (~40%) is dependent on printers and consumables, particularly serving end markets like data centers and defense; this exposes the company to risk if digital transformation or sustainability initiatives reduce future demand for traditional labeling solutions, potentially reducing future revenue streams.

- Ongoing facility consolidations, headcount reductions, and cost structure actions signal dependency on cost-cutting for near-term margin improvements rather than robust top-line growth or innovation-driven expansion, which could limit sustainable long-term margin expansion and earnings power.

- Increasing competition and the potential for commoditization in labeling and identification products threaten Brady's ability to maintain premium pricing, particularly as new acquisitions are integrated-any failure to achieve expected synergies or differentiate through technology could compress gross margins and reduce earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $101.5 for Brady based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.6 billion, earnings will come to $362.0 million, and it would be trading on a PE ratio of 16.3x, assuming you use a discount rate of 7.1%.

- Given the current share price of $83.45, the analyst price target of $101.5 is 17.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Brady?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.