Catalysts

About ATRenew

ATRenew operates an end to end platform for recycling, refurbishing and reselling pre owned consumer electronics and other high value categories in China and overseas.

What are the underlying business or industry changes driving this perspective?

- Although trade in penetration on major channels such as JD.com is still relatively low at just above 10 percent, future policy shifts or weaker subsidy support could slow upgrade activity and cap incremental device flow, limiting the pace of revenue growth from C2B supply inflows and related retail sales.

- Despite rapid network expansion to nearly 2,200 AHS stores and to door service coverage in about 300 cities, ongoing personnel, logistics and operating center costs may offset scale efficiencies, constraining further improvement in fulfillment expense ratios and non GAAP operating margins.

- While compliant refurbishment and 1P2C retail already lift 1P gross margin to 13.4 percent and 1P2C mix to 36.4 percent of product revenue, intensifying competition in premium pre owned smartphones could pressure pricing power and compress gross margin expansion, slowing earnings growth.

- Although multi category recycling and high value verticals like gold and luxury goods are scaling quickly with 95 percent transaction growth, structurally low take rates in standardized categories may dilute blended service margins and limit upside to net service revenue and overall profitability.

- While rising exports of China sourced used devices and the planned international version of PJT Marketplace open long term cross border opportunities, evolving export standards and execution complexity could delay overseas scaling, tempering the contribution of international business to total revenue and margin leverage.

Assumptions

This narrative explores a more pessimistic perspective on ATRenew compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

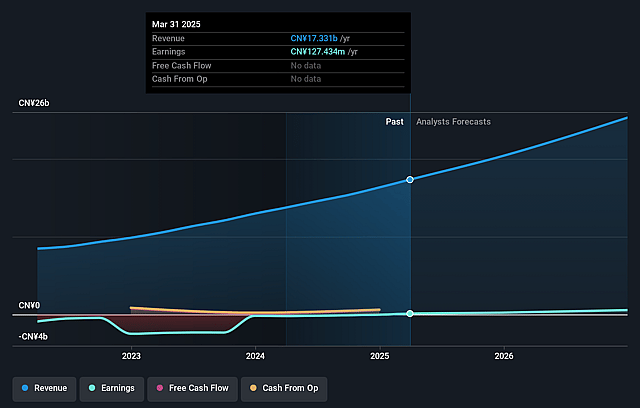

- The bearish analysts are assuming ATRenew's revenue will grow by 24.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 1.4% today to 3.6% in 3 years time.

- The bearish analysts expect earnings to reach CN¥1.4 billion (and earnings per share of CN¥6.82) by about December 2028, up from CN¥283.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 10.5x on those 2028 earnings, down from 29.2x today. This future PE is lower than the current PE for the US Specialty Retail industry at 19.9x.

- The bearish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.13%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The company is guiding to sustained rapid top line expansion, with third quarter 2025 revenue up 27.1 percent and full year revenue expected to grow close to 28 percent. If that high growth trend continues it could drive a re rating that lifts the share price as revenue scales.

- Structural mix improvements such as 1P gross margin rising to 13.4 percent and 1P2C revenue expanding to 36.4 percent of product revenue suggest growing pricing power and higher quality earnings. This could support a higher valuation multiple and stronger earnings growth.

- Scaling of higher take rate and value added services, including Paipai consignment with high single digit to 9 percent take rates and secondhand luxury with take rates above 10 percent, may steadily lift blended service margins and accelerate net margin expansion.

- Rapid expansion of the AHS Recycle brand, with nearly 2,200 stores, broad city coverage, and multi category recycling growth of 95 percent, could entrench market leadership in a structurally growing circular economy and potentially boost long term revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for ATRenew is $5.34, which represents up to two standard deviations below the consensus price target of $6.86. This valuation is based on what can be assumed as the expectations of ATRenew's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $8.04, and the most bearish reporting a price target of just $5.34.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2028, revenues will be CN¥37.8 billion, earnings will come to CN¥1.4 billion, and it would be trading on a PE ratio of 10.5x, assuming you use a discount rate of 9.1%.

- Given the current share price of $5.28, the analyst price target of $5.34 is 1.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ATRenew?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.