Last Update 09 Jul 26

Fair value Increased 3.10%COLB: Loan Trends Credit Stability And Buybacks Will Shape Future Risk Reward

Columbia Banking System's fair value estimate has been adjusted higher to $33.23 from $32.23 as analysts incorporate updated price targets in the low to mid $30s and expectations for steady loan, deposit, and C&I growth, along with stable credit trends.

Analyst Commentary

Recent research on Columbia Banking System centers on how current loan and deposit trends, along with credit quality, line up with valuation as price targets move into the low to mid $30s.

Bullish Takeaways

- Bullish analysts are raising price targets into the low to mid $30s, aligning with the updated fair value estimate and signaling that recent inputs on earnings power are viewed as supportive of this range.

- Expectations for loan and deposit growth in the mid single digit annualized range are seen as a positive for Columbia Banking System's ability to sustain revenue, which feeds directly into the higher valuation work.

- Stable credit trends cited in recent research underpin the case that current earnings assumptions are achievable, which helps justify price targets in the $32 to $35 area without relying on aggressive credit improvement.

- Comments about a multiyear inflection in C&I growth suggest that, if maintained, Columbia Banking System could have a more balanced growth mix, which some analysts see as supportive of its regional bank peer positioning.

Bearish Takeaways

- Despite higher targets, at least one major firm such as JPMorgan maintains a Neutral stance, signaling that, in its view, Columbia Banking System's current valuation already reflects much of the expected loan, deposit, and C&I growth.

- References to Equal Weight and Neutral ratings indicate that some bearish analysts remain cautious on upside potential, viewing the stock more as fairly valued than clearly mispriced.

- The reliance on mid single digit growth assumptions for both loans and deposits, along with stable credit, leaves limited room for execution missteps before the updated price targets could look demanding.

- With multiple firms adjusting models around the same set of expectations, there is a risk that Columbia Banking System is being priced off a relatively similar consensus view, which can limit rerating potential if results only track those assumptions.

What’s in the News for Columbia Banking System

- Columbia Banking System reported unaudited total net charge-offs of $35 million for the quarter ended March 31, 2026, compared with $30 million for the same quarter a year earlier. Source: Company key developments.

- From January 1, 2026 to March 31, 2026, Columbia Banking System repurchased 6,494,000 shares for $198.46 million, representing 2.2% of shares. Source: Company key developments.

- Since the buyback announced on October 30, 2025, Columbia Banking System has completed repurchases totaling 10,174,000 shares, or 3.43%, for $298.18 million. Source: Company key developments.

Valuation Changes for Columbia Banking System

- Fair Value: The fair value estimate for Columbia Banking System has risen slightly from $32.23 to $33.23.

- Discount Rate: The discount rate used in the valuation remains effectively unchanged at 7.11%.

- Revenue Growth: Revenue growth assumptions have edged down slightly from 10.31% to 10.24%.

- Net Profit Margin: Net profit margin expectations have fallen significantly from 37.99% to 31.97%.

- Future P/E: The future P/E assumption has increased from 11.77x to 14.45x, indicating a higher valuation multiple applied to Columbia Banking System's projected earnings.

Key Takeaways

- Expansion into high-growth Western regions and diversification of fee-based services are expected to drive revenue growth and stabilize earnings.

- Strategic investments in digital banking and operational efficiency should boost customer engagement, reduce costs, and enhance profitability.

- Heavy regional concentration, integration risks, lagging digital innovation, funding challenges, and portfolio runoff all threaten profitability and sustainable long-term revenue growth.

Catalysts

About Columbia Banking System- Operates as the Bank holding company of Umpqua Bank that provides banking, private banking, mortgage, and other financial services in the United States.

- The planned acquisition and integration of Pacific Premier is positioned to significantly expand Columbia's customer base and market reach in high-growth Western U.S. regions, increasing loan and deposit growth as both population and economic activity continue to rise in these areas; this is likely to have a positive impact on revenue and long-term earnings.

- Continued investment in AI, digital banking platforms, and embedded financial products is expected to drive greater customer engagement, acquisition, and retention-particularly as more consumers and businesses shift to digital channels-supporting higher fee income and reduced operating costs, thus improving net margins and earnings.

- The strategic expansion of fee-based businesses (treasury management, trust/custodial services, commercial card, merchant, and international banking), including new lines brought by Pacific Premier, should diversify revenue streams well beyond traditional lending, providing steadier top-line growth and helping to stabilize net margins.

- Columbia's disciplined approach to business banking, strong relationship focus, and targeting of small business clients positions it to benefit from the steady trend of small business formation in the U.S., which is likely to propel loan growth and recurring fee income, supporting revenue and earnings expansion.

- Ongoing operational efficiency initiatives, realized cost synergies from the Umpqua merger, and a robust capital position set the stage for ongoing improvements in operating leverage, capital returns, and ultimately, stronger net margins and book value per share.

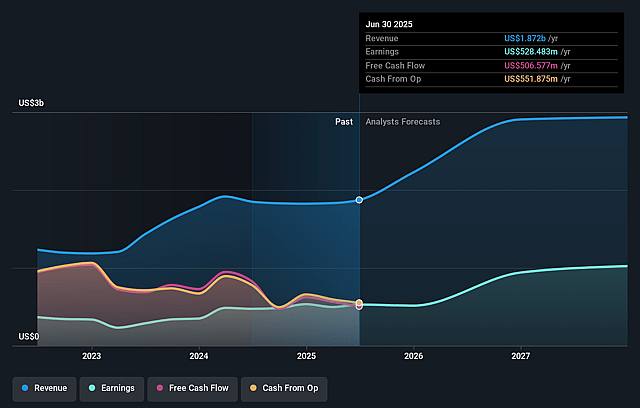

Columbia Banking System Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Columbia Banking System's revenue will grow by 10.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 28.0% today to 32.0% in 3 years time.

- Analysts expect earnings to reach $1.0 billion (and earnings per share of $3.53) by about July 2029, up from $654.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.5x on those 2029 earnings, up from 13.8x today. This future PE is greater than the current PE for the US Banks industry at 12.2x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Geographic and client base concentration remains high, with legacy and expanded operations still heavily dependent on the Western U.S. and specific new markets (e.g., Intermountain states), leaving Columbia Banking System vulnerable to regional economic downturns-potentially impacting credit quality, loan losses, and ultimately net margins and earnings.

- The company is engaged in multiple major integrations in close succession (recent Umpqua merger and upcoming Pacific Premier acquisition), which heightens execution risk; failure to realize anticipated synergies or unexpected integration costs could put pressure on operating efficiency and net margins.

- While technology investment in AI and fintech is mentioned, ongoing digitalization across banking creates competitive risk if Columbia lags relative to national banks or fintechs in delivering innovative online and mobile experiences; this could drive higher customer attrition and limit new customer acquisition, negatively affecting revenue and long-term growth.

- Prolonged deposit outflows, influenced by seasonal factors but also by customers' shifting funds into wealth management products or paying down debt, combined with reliance on wholesale funding to cover deposit shortfalls, could increase funding costs and compress net interest margins, eroding profitability.

- Continued runoff and repricing of the $6 billion legacy transactional asset portfolio creates an earnings headwind, and muted or negative net loan growth may persist during the multi-year transition; this could constrain revenue growth and delay improvement in overall profitability despite efforts to remix and improve the loan book.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $33.23 for Columbia Banking System based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $36.0, and the most bearish reporting a price target of just $29.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.1 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 14.5x, assuming you use a discount rate of 7.1%.

- Given the current share price of $31.27, the analyst price target of $33.23 is 5.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Columbia Banking System?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.