Last Update 01 Jun 26

Fair value Increased 0.65%CHRW: Scale And AI Productivity Programs Will Shape Post Montgomery Freight Cycle Outcomes

Analysts have nudged their average price target for C.H. Robinson Worldwide slightly higher to about $197 from roughly $196, reflecting growing confidence in the company's scale advantages and ongoing technology and productivity transformation following recent research updates and the post-Montgomery regulatory backdrop.

Analyst Commentary

Recent research has skewed more positive on C.H. Robinson, with several firms raising ratings or targets while still flagging real execution and regulatory risks. For you as an investor, the updates center on how well the company can turn its scale and technology work into margins and cash flow under a tighter legal framework.

Bullish Takeaways

- Bullish analysts highlight the company’s technology and productivity program as a key driver for future efficiency, arguing that the on site review of operations supports confidence in execution on cost and service improvements.

- Several bullish analysts point to scale as a core advantage in the post Montgomery regulatory setting, suggesting that higher compliance and insurance costs could weigh more heavily on smaller brokers and truckload carriers.

- Some research notes emphasize the balance sheet, suggesting C.H. Robinson is positioned as a potential consolidator if smaller competitors struggle with the new liability framework, which could influence long term growth and competitive positioning.

- One upgrade follows Q1 results that were viewed as better than expected on margins, with the view that the stock’s prior underperformance relative to peers already reflects concerns about truckload spot rate pressure.

Bearish Takeaways

- Bearish analysts point to prior margin risk tied to higher truckload spot rates, cautioning that profitability could be pressured if pricing and volumes do not offset cost headwinds.

- Some research items reference lower price targets or list removals, signaling concern that expectations may have run ahead of the company’s ability to execute consistently on its tech and productivity goals.

- The Supreme Court’s Montgomery decision is also viewed as a source of added legal and operational complexity, with cautious analysts warning that liability exposure could raise ongoing compliance costs and weigh on returns if not managed carefully.

- Where targets have been reduced, the tone suggests a more conservative stance on valuation until there is clearer evidence that margin improvements and regulatory adjustments are sustainable.

What's in the News

- The U.S. Supreme Court’s Montgomery v. Caribe Transport II decision allows freight brokers such as C.H. Robinson to be held liable in accident related lawsuits, increasing potential litigation and insurance costs while potentially pressuring smaller brokers that have fewer compliance resources. (Source: Supreme Court ruling coverage)

- Following the ruling, analysts at Citi, Jefferies and JPMorgan highlighted C.H. Robinson’s scale, carrier vetting processes, fraud prevention tools and compliance programs as potential advantages. Some research also pointed to possible consolidation as smaller competitors face higher risk. (Source: Supreme Court ruling coverage)

- C.H. Robinson expressed disappointment with the Montgomery decision but reaffirmed its focus on safety, service and federal oversight, including support for Dalilah’s Law. Management indicated they expect only modest financial impact from potential insurance premium changes. (Source: Supreme Court ruling coverage)

- Jefferies upgraded C.H. Robinson from Hold to Buy and lifted its price target to US$200, citing early stage technology and productivity work, use of AI and Lean practices, and the company’s balance sheet as reasons it could act as a consolidator in freight brokerage. This comes even with competitive noise from Amazon’s supply chain offering. (Source: Jefferies research summary)

- C.H. Robinson shares fell 3.6% after the Q1 2026 filing as investors focused on cash flow, working capital pressures and freight cycle uncertainty. A prior 8.9% share drop earlier in May followed Amazon’s expansion of supply chain services to third party businesses. (Source: Q1 2026 trading recap)

Valuation Changes

- Fair Value: updated to $196.79 from $195.52, a modest upward move of about 0.6% that keeps the implied valuation range relatively tight.

- Discount Rate: adjusted to 7.92% from 7.83%, a small increase that slightly raises the required return used in the model.

- Revenue Growth: now set at 5.58% versus 5.57% previously, a minimal change that keeps long term top line assumptions broadly consistent.

- Net Profit Margin: revised to 4.75% from 4.60%, a mild uplift in expected profitability on future dollar revenue.

- Future P/E: reduced to 31.95x from 34.41x, a moderate downward shift that implies a lower valuation multiple applied to projected earnings.

Key Takeaways

- AI-driven automation and digital tools are boosting margins, efficiency, and customer retention while supporting scalable growth and market share gains.

- Investments in integrated, data-rich logistics and global expansion position the company to benefit from outsourcing trends and increased supply chain complexity.

- Exposure to trade policy risks, rising technology-driven competition, and dependence on volatile customs revenue threaten sustainable margins and future earnings stability.

Catalysts

About C.H. Robinson Worldwide- Provides freight transportation and related logistics and supply chain services in the United States and internationally.

- Acceleration in AI-driven automation across the full lifecycle of shipments is driving evergreen productivity and efficiency gains, enabling the company to decouple headcount from volume growth and deliver sustained gross margin and operating margin expansion, supporting higher long-term earnings and net margins.

- Scaling of proprietary digital capabilities and deployment of automated, self-serve logistics tools improves data-driven pricing, rapid quote response, and customer supply chain visibility, leading to market share gains and higher wallet share, positively impacting future revenue growth.

- The increasing complexity of global supply chains, driven by tariff volatility and trade uncertainties, is elevating customer demand for integrated, data-rich solutions-areas where C.H. Robinson is investing and expanding-resulting in strong customer retention and a more resilient recurring revenue base.

- Expansion of advanced automation and real-time optimization tools to global forwarding operations is expected to unlock additional productivity and gross margin gains outside the core North American business, supporting further top-line growth and improved overall margins.

- Persistent industry shift toward outsourcing logistics and supply chain management, alongside customer "flight to quality" amid volatility, positions C.H. Robinson to capture incremental market share and deliver above-market revenue and earnings growth as demand recovers.

C.H. Robinson Worldwide Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

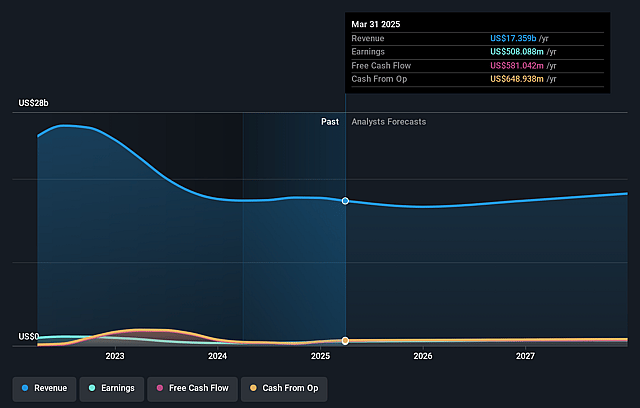

- Analysts are assuming C.H. Robinson Worldwide's revenue will grow by 5.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.7% today to 4.8% in 3 years time.

- Analysts expect earnings to reach $906.0 million (and earnings per share of $8.28) by about June 2029, up from $599.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.1 billion in earnings, and the most bearish expecting $791.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.0x on those 2029 earnings, down from 35.2x today. This future PE is greater than the current PE for the US Logistics industry at 19.6x.

- Analysts expect the number of shares outstanding to decline by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.92%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The ongoing uncertainty and volatility in global trade policy, including elevated tariffs and trade negotiations, is making planning and forecasting more difficult for C.H. Robinson and its customers, which could dampen net revenue growth and drive unpredictable earnings volatility if these trade frictions persist or worsen.

- There is increasing democratization of freight brokerage technology-smaller brokers now have easier access to advanced digital tools, which could intensify competition, limit differentiation based on technology, and potentially erode C.H. Robinson's market share and gross margin over time.

- While current profitability gains are supported by process automation and AI-driven workforce reductions, any failure to keep pace with rapid advances in AI, agentic AI, or autonomous supply chain technology (especially if rivals out-innovate C.H. Robinson) could lead to higher operational costs and compress net margins in the longer term.

- Strong recent financial results are partly reliant on the elevated complexity in customs and tariffs, which may be transitory rather than structural; any simplification of global trade or resolution of tariff disputes could reduce the high-margin customs revenue stream, negatively impacting future operating income and earnings quality.

- C.H. Robinson's non-asset-based model limits its control over underlying carrier quality and cost structure; during elongated industry downturns or tightening regulatory environments (e.g., emissions, labor standards), this exposes the company to greater rate volatility and cost inflation that could compress net margins and reduce earnings resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $196.79 for C.H. Robinson Worldwide based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $230.0, and the most bearish reporting a price target of just $90.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $19.1 billion, earnings will come to $906.0 million, and it would be trading on a PE ratio of 32.0x, assuming you use a discount rate of 7.9%.

- Given the current share price of $178.65, the analyst price target of $196.79 is 9.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on C.H. Robinson Worldwide?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.