Last Update 22 Jun 26

Fair value Decreased 0.078%SUI: UK Exit And Buybacks Will Support Cleaner REIT Upside

The analyst price target for Sun Communities has been adjusted slightly lower from $142.11 to $142.00 as analysts update their models to reflect the announced sale of the company’s U.K. assets and its impact on valuation assumptions.

Analyst Commentary

Recent research updates on Sun Communities cluster around the announced sale of the U.K. assets, with analysts refining their models and price targets to reflect the new footprint and capital allocation plans.

Bullish Takeaways

- Bullish analysts view the U.K. platform sale as a clean-up of the portfolio that can support a clearer valuation framework focused on the core business.

- Some see the exit from the U.K. as removing an overhang on the stock, which they argue had been weighing on how investors value Sun Communities.

- Where targets are trimmed, bullish analysts generally tie the adjustments to model updates around asset sales rather than a broad shift in stance on execution or long term growth potential.

- Upgrades and Overweight or Outperform ratings indicate confidence that Sun Communities can execute on capital recycling, including the mix of potential buybacks, acquisitions and debt reduction mentioned in recent notes.

Bearish Takeaways

- Bearish analysts highlight the impairment related to the Park Holidays UK portfolio and factor this into lower price targets, framing it as a headwind for near term earnings and valuation.

- Underperform and Hold ratings show concern around execution risk as the company transitions away from the U.K. assets and redeploys capital.

- Target cuts into the low to mid US$130s suggest caution on how quickly Sun Communities can translate the simplified portfolio into stronger financial metrics.

- Some commentary points to dilution from the sale as a key issue, even if partially offset by capital allocation plans, which keeps a lid on how aggressive bearish analysts are willing to be on valuation multiples.

What's in the News for Sun Communities

- Sun Communities, Inc. announced a share repurchase program authorizing the company to buy back up to US$1,000 million of its shares, with the program running through May 27, 2027. (Source: Buyback Transaction Announcement)

- The Board of Directors authorized a new buyback plan on May 27, 2026, providing further capacity for Sun Communities to repurchase its stock over time. (Source: Buyback Transaction Announcement)

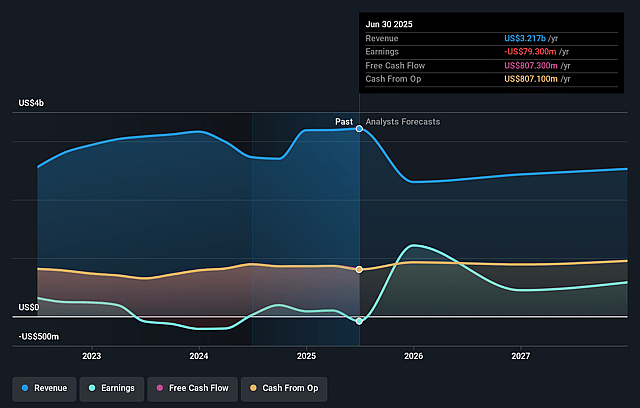

- For the second quarter ending June 30, 2026, Sun Communities provided earnings guidance for diluted EPS attributable to the consolidated portfolio in a range of US$0.62 to US$0.70, and for full year 2026 in a range of US$2.16 to US$2.36. (Source: Corporate Guidance)

- Between January 1, 2026 and March 31, 2026, Sun Communities repurchased 475,147 shares, representing 0.38% of shares outstanding, for US$59.9 million, bringing total repurchases under the May 6, 2025 buyback to 4,766,407 shares, or 3.78%, for US$598.96 million. (Source: Buyback Tranche Update)

- On March 23, 2026, the Audit Committee approved Deloitte & Touche LLP as Sun Communities' new independent registered public accounting firm for the fiscal year ending December 31, 2026, and decided to dismiss Grant Thornton LLP following completion of its current engagement for the period ended March 31, 2026. (Source: Auditor Changes)

Valuation Changes for Sun Communities

- Fair Value: The model fair value has edged down slightly from $142.11 to $142.00 per share, reflecting a very small adjustment to underlying assumptions.

- Discount Rate: The discount rate has been reduced marginally from 7.20% to 7.17%, a move that slightly increases the present value of future cash flows in the model for Sun Communities.

- Revenue Growth: The long term revenue growth assumption is effectively unchanged, moving from 2.32% to 2.32% with only a minimal numerical adjustment.

- Net Profit Margin: The projected net profit margin has been refined from 15.32% to 15.32%, indicating only a very small technical update rather than a shift in outlook for Sun Communities.

- Future P/E: The assumed future P/E multiple has eased slightly from 53.35x to 53.27x, indicating a modestly lower valuation multiple applied in the refreshed model.

Key Takeaways

- Strong housing demand and high barriers to entry drive stable occupancy, rent growth, and predictable long-term cash flow in core manufactured housing and RV segments.

- Operational efficiencies, leadership changes, and a stronger balance sheet enhance earnings and financial flexibility, enabling strategic expansion in high-demand markets.

- Growth prospects are challenged by halted developments, acquisition constraints, geographic risks, rising expenses, and persistent weakness in the RV segment threatening long-term revenue stability.

Catalysts

About Sun Communities- Established in 1975, Sun Communities, Inc.

- Structural U.S. housing affordability issues and persistent high home prices continue to drive record-high occupancy (97.6%) and rent growth within Sun's manufactured housing communities, resulting in resilient revenue growth and stable, long-term cash flow.

- The growing population of retirees and seniors, combined with high barriers to entry in the manufactured housing segment, positions Sun to capture sustained demand and rental rate increases-supporting reliable NOI growth and higher net operating margins.

- Streamlined operations, organizational restructuring, and expanded cost-saving initiatives (e.g., procurement standardization, payroll efficiency) have already delivered more than $17 million in annualized expense reductions, which are set to further enhance net margins and boost recurring earnings.

- The appointment of a new, experienced CEO alongside the company's strengthened balance sheet (substantial debt paydown, credit upgrades, ample financial flexibility) positions Sun to capitalize on selective acquisition and expansion opportunities in supply-constrained, high-demand markets, underpinning future revenue and asset value growth.

- The ongoing shift toward long-term annual RV residents, higher penetration of rental homes, and continued focus on converting transient sites to annual rentals create stable, high-quality recurring income streams and reduce volatility, thereby supporting predictable earnings and supporting future FFO growth.

Sun Communities Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Sun Communities's revenue will grow by 2.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -2.6% today to 15.3% in 3 years time.

- Analysts expect earnings to reach $383.9 million (and earnings per share of $3.07) by about June 2029, up from -$60.8 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $459.2 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 53.6x on those 2029 earnings, up from -240.1x today. This future PE is greater than the current PE for the US Residential REITs industry at 29.9x.

- Analysts expect the number of shares outstanding to decline by 1.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.17%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company is no longer pursuing new greenfield developments in the U.S. or U.K., which could limit organic growth opportunities in their core manufactured housing and RV segments, potentially constraining long-term revenue and asset value expansion.

- Elevated cap rates for acquisitions of high-quality communities are at the lower end of the 4–5% range, and the company notes increased selectivity and fewer accretive opportunities, which may compress future return on invested capital and earnings growth as acquisition multiples rise across the industry.

- Geographic concentration remains high in the Sunbelt and select states (e.g., Florida, Arizona), leaving Sun Communities exposed to region-specific risks such as adverse weather, climate events, or regulatory changes, which could increase volatility in expenses or cause property damage, impacting net margins.

- Expense headwinds are apparent, including rising payroll, utilities, and property operating costs, which-despite recent savings-may escalate further due to inflation, higher labor costs, and property tax increases in primary markets, threatening long-term margin expansion and FFO per share.

- The RV segment, particularly transient RV revenue, continues to face persistent declines (projected 9% full-year revenue drop), raising concerns about sustained demand in this segment; the shift toward annual RV conversions and reliance on cost discipline may not fully offset potential longer-term declines in this business, potentially pressuring overall revenue and stable cash flows.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $142.0 for Sun Communities based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $155.0, and the most bearish reporting a price target of just $127.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.5 billion, earnings will come to $383.9 million, and it would be trading on a PE ratio of 53.6x, assuming you use a discount rate of 7.2%.

- Given the current share price of $118.46, the analyst price target of $142.0 is 16.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Sun Communities?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.