Last Update 24 Jul 26

Fair value Decreased 4.86%RMD: Sleep Health Demand And GLP 1s Will Support Post MatrixCare Upside

ResMed's analyst price target has been revised lower, with the fair value estimate moving from about $260.60 to roughly $247.93 as analysts factor in FY27 headwinds tied to Astral ventilator component constraints, higher costs of goods, and potential competitive pressure from a possible Philips Respironics re entry.

Analyst Commentary

Recent research on ResMed reflects a split view, with bullish analysts still seeing long term growth drivers in sleep and respiratory care, while more cautious voices focus on near term execution risks, valuation reset, and competitive questions around 2027.

Bullish Takeaways

- Bullish analysts still see room for upside in ResMed, even after multiple price target cuts, with several targets in the low to mid US$200s and Goldman Sachs flagging conviction on the stock with an A$46.70 target.

- Some research highlights ongoing CPAP and obstructive sleep apnea patient activity, with demand linked to GLP 1 therapies and consumer wearables. This supports the view that ResMed's core therapy market remains supported.

- The sale of MatrixCare is framed by some bullish analysts as cleaning up the RCS portfolio by exiting a business that was detracting from overall growth. This could simplify the story and focus capital on core sleep and respiratory assets.

- Despite near term caution, some research argues that ResMed still has a medium to longer term opportunity in its core markets, with current valuation resets partly reflecting timing and competitive assumptions rather than a change in the long term thesis.

Bearish Takeaways

- Bearish analysts point to a clear downshift in expectations, with multiple downgrades from more positive ratings to neutral or sector perform and price targets moving from the high US$200s toward the low US$200s. This reflects concerns about execution and earnings visibility.

- FY27 is a focal point of caution, as several reports highlight headwinds tied to Astral ventilator component scarcity, prioritization of existing machines over new builds, and associated EPS pressure that could weigh on growth expectations.

- Research points to supply constraints, higher costs of goods, and potential EPS dilution from the Noctrix acquisition, with at least one estimate citing US$0.32 of expected dilution. This collectively introduces more uncertainty into near term profitability.

- Analysts also flag the potential re entry of Philips Respironics into the U.S. device market in 2027 as a key risk, with concerns that increased competition could pressure ResMed's device sales and keep some investors on the sidelines until there is more clarity.

What’s in the News for ResMed

- ResMed agreed to sell its MatrixCare post acute care software business to Frazier Healthcare Partners for US$490 million in cash, with plans to focus more tightly on sleep and respiratory health and to use part of the proceeds for an accelerated share repurchase program and general corporate purposes. (Primary news)

- Recent commentary highlights that ResMed’s share price is down more than 23% over the past year and is described as trading roughly 25% to 30% below some intrinsic value estimates, with discussion around GLP 1 therapies, supply constraints, recurring revenue from consumables, and digital health platforms such as AirView. (Primary news)

- UBS notes that ResMed is expected to report strong fiscal Q4 earnings growth supported by an 8.6% rise in sales, while also flagging gross margin pressure from input cost inflation and ventilator supply chain issues that could affect fiscal 2027. (Primary news)

- ResMed has been dropped from several Russell growth benchmarks, including the Russell 1000 Growth, Russell Midcap Growth, Russell 1000 Growth Defensive, Russell 3000E Growth, and Russell 3000 Growth indices, which may influence how certain index linked funds and mandates treat the stock.

- ResMed announced a partnership with Oura that connects Oura Ring sleep and wellness data with ResMed sleep health resources, aimed at helping more users identify possible sleep issues and access care pathways, and reported ongoing share repurchases and an upcoming CFO transition from Brett Sandercock to Aaron Bloomer in May 2026.

Valuation Changes for ResMed

- Fair Value: revised lower from $260.60 to $247.93, a reduction of about 4.9% that reflects updated assumptions in the model.

- Discount Rate: adjusted slightly from 7.49% to 7.42%, a small move that suggests only a modest change in assessed risk or required return.

- Revenue Growth: reduced from 7.21% to 5.41%, indicating a more cautious stance on ResMed's projected top line expansion.

- Net Profit Margin: trimmed from 28.16% to 27.50%, pointing to slightly lower expected profitability on future $ revenue.

- Future P/E: nudged higher from 23.75x to 24.29x, implying that the updated fair value still assumes a similar, slightly higher earnings multiple on ResMed's projected profits.

Key Takeaways

- Strategic acquisitions, innovation, and digital health adoption are broadening market reach, deepening customer retention, and driving resilient revenue and margin growth.

- Operational efficiencies and increased awareness in sleep health strengthen competitive advantages, fueling long-term earnings expansion and greater profitability.

- Competitive, regulatory, and market shifts threaten ResMed's pricing power, market share, and profitability, especially as its hardware-focused model faces digital disruption and rising compliance costs.

Catalysts

About ResMed- Develops, manufactures, distributes, and markets medical devices and cloud-based software applications for the healthcare markets.

- Strategic investments in expanding the diagnosis and treatment funnel-including acquisitions like VirtuOx, Ectosense, and Somnoware-are improving patient flow from screening to therapy, positioning ResMed to capture a larger share of the substantial underpenetrated global sleep apnea and respiratory market, supporting long-term revenue growth.

- Increased global awareness of sleep health issues, amplified by direct-to-consumer marketing campaigns and education programs for primary care physicians, is driving higher diagnosis and treatment rates, translating to elevated demand for ResMed's products and sustained top-line revenue growth.

- Acceleration in adoption of home-based, cloud-connected therapy solutions and digital health platforms (including software like Brightree and AirView) enhances recurring high-margin revenue streams and increases both user retention and net profit margins over time.

- Ongoing innovation in product development-including new releases of CPAP devices, mask interfaces, and integration of AI-driven features-strengthens ResMed's competitive differentiation and supports premium pricing power, driving both revenue and margin expansion.

- Optimization initiatives in procurement, manufacturing, and logistics-along with the build-out of the U.S. manufacturing footprint-are structurally improving gross margins, which, when combined with operating leverage from global scale, are expected to boost overall earnings and free cash flow.

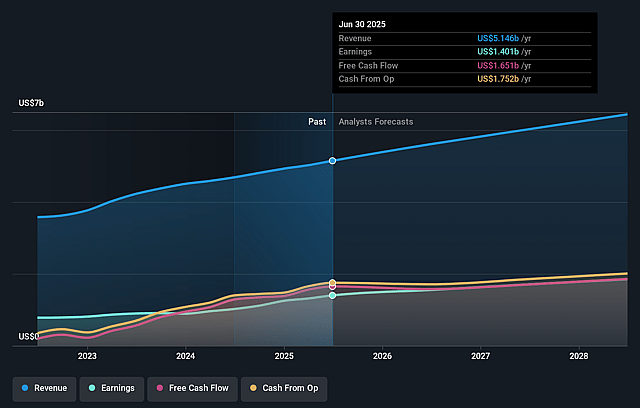

ResMed Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming ResMed's revenue will grow by 5.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 27.4% today to 27.5% in 3 years time.

- Analysts expect earnings to reach $1.8 billion (and earnings per share of $13.86) by about July 2029, up from $1.5 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 24.3x on those 2029 earnings, up from 18.2x today. This future PE is lower than the current PE for the AU Medical Equipment industry at 26.4x.

- Analysts expect the number of shares outstanding to decline by 0.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.42%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The potential resumption or tightening of CMS competitive bidding programs in the US could pressure pricing and reimbursement rates for ResMed's core devices, leading to reduced revenue growth and compressed net margins.

- Intensifying competition in the sleep apnea and respiratory market-including from alternative therapies such as GLP-1 drugs and hypoglossal nerve stimulators-may slow device adoption and erode ResMed's market share, negatively impacting topline revenue and margins.

- Heavy dependence on positive secular trends (aging population, home-based care, and sleep disorder prevalence) exposes ResMed to risk if healthcare cost containment or stricter reimbursement policies emerge globally, which could limit growth and pressure earnings.

- The accelerating transition toward digital and preventative health, as well as commoditization of respiratory medical equipment, may lower average selling prices and challenge ResMed's hardware-centric business model, impacting net margin expansion and longer-term profitability.

- Rising regulatory and compliance demands-especially related to data privacy, cybersecurity, and evolving healthcare software oversight-could increase R&D and SG&A costs, pose legal risks, and potentially delay new product launches, putting pressure on future earnings and operating leverage.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $247.93 for ResMed based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $325.0, and the most bearish reporting a price target of just $180.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $6.5 billion, earnings will come to $1.8 billion, and it would be trading on a PE ratio of 24.3x, assuming you use a discount rate of 7.4%.

- Given the current share price of $191.89, the analyst price target of $247.93 is 22.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ResMed?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.