Last Update 07 Jul 26

Fair value Decreased 15%CNXC: Reset Expectations And Index Shift Will Support Future Upside Potential

Analysts have lowered the Concentrix fair value estimate from $41.25 to $35.25, reflecting reduced long term revenue growth assumptions. Profit margin expectations and the future P/E input also shift in response to updated models following recent Q2 results and guidance.

Analyst Commentary

Street research on Concentrix points to a mixed setup, with most analysts cutting price targets after fiscal Q2 but drawing different conclusions on how the stock should be valued against its long term earnings and revenue potential.

Bullish Takeaways

- Bullish analysts maintain positive ratings even after lower price targets, indicating they still see upside relative to current levels despite trims to valuation assumptions.

- Several models continue to project meaningful non GAAP EPS into FY26 and FY27, which supports the view that Concentrix can still build an earnings base that may justify higher P/E multiples over time if execution stays on track.

- Some bullish views frame the Q2 reset as already reflected in recent share price weakness, suggesting that part of the guidance cut and client specific issues may be priced into current valuations.

- Revised targets in the US$30 to US$45 range imply that, even with more conservative modeling, Concentrix is being valued on expectations of continued profitability rather than a turnaround or distress case.

Bearish Takeaways

- Bearish analysts highlight macro and client specific pressures following Q2, which have led to lower FY26 and FY27 revenue and EPS forecasts and, in turn, reduced fair value estimates.

- A cut in guidance that now points to steadily decelerating growth as the year closes has raised questions about the durability of Concentrix growth profile and the level of P/E the stock should command.

- The move in one major price target down to US$26 signals caution that earnings risk may still exist if client headwinds persist, limiting near term room for valuation expansion.

- Across the research, successive target cuts cluster around a lower band than before Q2, reinforcing the view that Concentrix is now being modeled with more conservative assumptions on growth, margins and execution consistency.

What’s in the News for Concentrix

- Concentrix reported fiscal Q2 2026 results with a very large, roughly 4x year over year increase in iX Suite contract signings and record cash flow from operations, alongside a US$0.36 quarterly dividend and plans to more than double iX Suite revenue to over US$120 million in annual recurring revenue, according to recent earnings coverage.

- Despite solid Q2 earnings metrics and expanding AI focused services, Concentrix stock has fallen about 85% over recent years and dropped a further 24% after the latest report before recovering 11.9%. This reflected market reaction to a weaker outlook and tempered expectations for future growth, per multiple news sources.

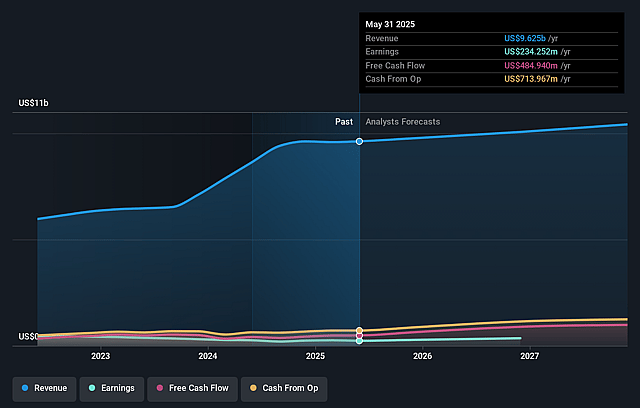

- Q2 2026 revenue of US$2.46b, 1.9% higher year over year, came with margin pressure and restructuring tied to severance for about 20,000 employees. Management also lowered full year 2026 revenue guidance by 1.3% and adjusted EPS guidance by 6.5% to US$10.83 to US$11.18, according to earnings reports.

- Concentrix completed a multi year share repurchase program totaling 8,512,734 shares for US$557.41 million and plans to sell a non core business for about €15 million, recognizing a US$6.9 million loss on held for sale assets, based on recent company disclosures.

- Index changes have reshaped Concentrix’s footprint in equity benchmarks, with the stock dropped from several Russell 1000 and S&P 400 indexes and added to the Russell 2000, Russell 2000 Value, Russell 2000 Dynamic and S&P 600, according to index provider updates.

Valuation Changes for Concentrix

- Fair Value, reduced from $41.25 to $35.25, has fallen by about 14.5%, reflecting lower long term assumptions in the revised model.

- Discount Rate, held steady at 12.46%, remains unchanged and indicates no adjustment to the assumed risk profile for Concentrix cash flows.

- Revenue Growth, lowered from 2.28% to 0.56%, has fallen significantly. The updated forecast now implies roughly one quarter of the prior annual growth assumption.

- Net Profit Margin, increased from 16.03% to 18.56%, has risen moderately and suggests expectations for a higher share of revenue to convert into earnings over time.

- Future P/E, reduced from 1.89x to 1.46x, has moved lower and points to a more conservative earnings multiple applied to Concentrix in the updated valuation work.

Key Takeaways

- Integrating AI solutions and iX Hello products is expected to drive revenue growth and earnings by enhancing client offerings and operational efficiency.

- The Webhelp acquisition synergies, capital allocation, and share repurchases aim to improve margins and EPS, supporting profitability and shareholder returns.

- Concentrix's growth and profitability are at risk due to modest revenue growth, integration challenges, currency risks, high debt, and client concentration issues.

Catalysts

About Concentrix- Designs, builds, and runs integrated customer experience (CX) solutions worldwide.

- Concentrix is focusing on integrating AI solutions across its operations and client offerings, which is expected to drive revenue growth as it becomes a trusted provider for AI solutions in the market. The adoption of its GenAI platforms is positioned to increase revenue by expanding the share of wallet with current clients.

- The company is monetizing its iX Hello products, designed to be accretive to earnings by the end of fiscal 2025. The transition from pilot phases to deployments is expected to positively impact earnings growth.

- Concentrix is experiencing revenue growth from partner consolidation. By expanding its business solutions and becoming a leading provider of integrated AI and business services, it is positioned to capture more client spending, impacting revenue and potentially improving net margins due to increased efficiency.

- The synergies from the Webhelp acquisition and integration are expected to yield margin expansion, with anticipated savings boosting non-GAAP operating margins over time. This contributes to both profitability and cash flow improvements.

- Concentrix’s capital allocation strategy involves share repurchases, which are likely to enhance EPS as the company takes advantage of perceived undervaluation. This strategy also includes investing for long-term growth while managing debt, enhancing net margins, and maintaining shareholder returns.

Concentrix Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Concentrix's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from -13.2% today to 18.6% in 3 years time.

- Analysts expect earnings to reach $1.9 billion (and earnings per share of $30.59) by about July 2029, up from -$1.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $2.1 billion in earnings, and the most bearish expecting $1.2 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 1.5x on those 2029 earnings, up from -1.1x today. This future PE is lower than the current PE for the US Professional Services industry at 21.1x.

- Analysts expect the number of shares outstanding to decline by 3.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Although Concentrix experienced a modest revenue growth of 1.3% year-over-year, a low growth rate could indicate potential challenges in maintaining or accelerating revenue growth, particularly if macroeconomic conditions do not improve, impacting future revenues.

- The pressure to integrate and harmonize Webhelp's operations and synergies could lead to increased costs and potential disruptions if not managed effectively. This could impact operating margins and net income if anticipated synergies are not realized timely.

- Concentrix faces potential currency exchange rate risks, with ongoing revenue guidance assuming up to a 135 basis point negative impact on full-year results. This could affect both reported revenues and net earnings.

- The company has a significant debt burden, with total debt standing at $4.9 billion. Rising interest rates or refinancing challenges could increase interest expenses, affecting net income and cash flow available for dividends or reinvestment.

- Dependence on a limited number of top clients, whose revenue growth outpaces the rest of the business, presents concentration risk. Any downturn in a major client's business could materially affect Concentrix's revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $35.25 for Concentrix based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $45.0, and the most bearish reporting a price target of just $26.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $10.2 billion, earnings will come to $1.9 billion, and it would be trading on a PE ratio of 1.5x, assuming you use a discount rate of 12.5%.

- Given the current share price of $23.42, the analyst price target of $35.25 is 33.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Concentrix?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.