Last Update 17 Jun 26

MKL: AI And Specialty Focus Will Meet Activist And Execution Tests

Analysts have lowered their price target on Markel Group stock by $150, citing updated views reflected in recent Neutral ratings and target revisions. They have left key long term valuation inputs essentially unchanged, including fair value, discount rate, revenue growth, profit margin, and future P/E.

Analyst Commentary

Recent research on Markel Group stock points to a more cautious stance, with the lower price target and Neutral ratings reflecting a reassessment of near term expectations while keeping the long term framework largely intact.

Bullish Takeaways

- Bullish analysts are maintaining their long term fair value and P/E assumptions, which signals continued confidence in Markel Group’s underlying business model rather than a fundamental reset.

- The decision to keep revenue growth and profit margin inputs unchanged suggests that expectations for the company’s ability to execute on its current strategy remain intact despite the lower target.

- The unchanged discount rate implies that analysts are not assigning additional risk to Markel Group’s cash flows, which can be read as support for the company’s balance sheet and business stability.

- Neutral ratings, rather than outright negative calls, indicate that bullish analysts still see room for long term value if execution matches existing forecasts.

Bearish Takeaways

- Bearish analysts are using the US$150 price target cut to signal that, at recent trading levels, Markel Group may already reflect much of the value implied by current fair value models.

- The Neutral stance points to concerns about near term upside, with investors potentially needing clearer catalysts on growth, underwriting results, or investment returns before reassessing valuation.

- The fact that key long term inputs are unchanged while the target is lower suggests caution around shorter term execution risks or market conditions that could cap the stock’s re-rating.

- Some bearish analysts appear wary that, without revisions to revenue or margin assumptions, there may be limited room to raise estimates, which can weigh on sentiment toward Markel Group stock in the near term.

What’s in the News for Markel Group

- Markel Insurance CEO Simon Wilson outlined Markel Group’s focus on specialty insurance, faster execution, stronger customer trust, and the use of AI in underwriting and operations. He also reiterated that the recent US$150 analyst price target cut reflects updated assumptions rather than a changed long term thesis. (Source: recent CEO commentary)

- Activist investor JANA Partners urged Markel Group’s board to divest the Markel Ventures segment and pursue a US$2b share tender offer, arguing that Ventures has diluted valuation and that the board should prioritize shareholder outcomes. (Source: JANA Partners letter)

- Markel International partnered with hyperexponential to roll out an Environmental rating capability in Canada, aiming to streamline underwriting workflows and create a centralized rating layer that can support more complex products and AI enabled processes over time. (Source: company client announcement)

- Markel Group reported buybacks of 63,237 shares for US$127.66m in the first quarter of 2026, bringing total repurchases under the November 13, 2024 authorization to 334,240 shares for US$630.07m. (Source: buyback tranche update)

- Markel Group proposed an amendment to its Amended and Restated Articles of Incorporation for shareholder approval at the May 20, 2026 AGM, signaling governance related changes under consideration. (Source: AGM materials)

Valuation Changes for Markel Group

- Fair Value: Model fair value remains unchanged at $2,005.4 per share, indicating no adjustment to the core valuation anchor for Markel Group stock in this update.

- Discount Rate: The discount rate is effectively unchanged at 7.108%, suggesting the risk profile and required return assumptions are consistent with prior work.

- Revenue Growth: Forecast revenue growth is essentially stable at 3.29%, with only a very small numerical refinement, so top line expectations are effectively the same.

- Net Profit Margin: Projected net profit margin remains aligned with the previous input at about 11.72%, with only a minor rounding difference in the updated figure.

- Future P/E: The future P/E multiple assumption is effectively unchanged at 14.30x, indicating no material shift in how earnings are being capitalized in the Markel Group valuation model.

Key Takeaways

- Decentralization, operational restructuring, and digital transformation aim to boost underwriting results, efficiency, and support higher long-term profitability in core specialty insurance.

- Expansion of non-insurance ventures and redeployment of freed capital improve earnings diversification, reduce volatility, and position for stable, compounded growth.

- Persistent legacy risks, operational challenges, and industry headwinds threaten profitability, revenue growth, and market position amid organizational changes and increasing competition.

Catalysts

About Markel Group- Through its subsidiaries, engages in the insurance business in the United States and internationally.

- The restructuring and re-segmentation of Markel's insurance operations, including decentralizing decision-making and aligning accountability with clear P&L ownership, is expected to drive expense efficiency and strengthen underwriting performance, likely improving overall net margins and earnings as operational improvements take hold.

- Exiting underperforming lines and moving the subscale, loss-making reinsurance business into runoff frees up capital for more profitable specialty insurance opportunities, while enabling a strategic focus on high-growth, high-demand specialty markets. This shift should enhance risk-adjusted ROE and support more stable long-term revenue and earnings growth.

- The expansion and success of Markel Ventures, marked by recurring cash flow from non-insurance businesses and recent contributions from new stable-growth units (like EPI and Valor), provide stronger earnings diversification and are expected to reduce volatility in consolidated net income and margins.

- Ongoing digital transformation-coupled with Markel's decentralization, autonomous business unit structure, and adoption of advanced analytics in risk assessment-is anticipated to result in superior risk selection, pricing accuracy, and improved loss ratios, driving better profitability and supporting future revenue expansion.

- The company's focus on allocating released capital-both from runoff businesses and growing investment income on reserves-into higher-return opportunities, including public equities and strategic acquisitions, is poised to accelerate intrinsic book value per share and long-term compounded earnings, especially as the specialty insurance and programs market expands alongside global asset growth.

Markel Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Markel Group's revenue will grow by 3.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.9% today to 11.7% in 3 years time.

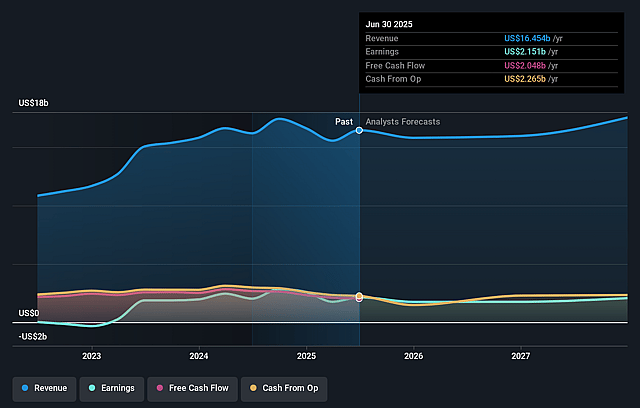

- Analysts expect earnings to reach $2.1 billion (and earnings per share of $203.79) by about June 2029, up from $1.7 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.4x on those 2029 earnings, up from 13.5x today. This future PE is greater than the current PE for the US Insurance industry at 11.3x.

- Analysts expect the number of shares outstanding to decline by 1.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Significant legacy exposure and ongoing reserve strengthening in discontinued lines (U.S. and European risk-managed D&O, Global Reinsurance, and CPI) suggest persistent risk of further adverse loss development or reserve deficiencies, which could negatively impact net earnings and combined ratios in future periods.

- The runoff and exit from the Global Reinsurance business will generate a gradual decline in gross written premiums and limit near-term revenue growth, while the full release of associated capital and earnings accretion from this move will not materialize for several years, potentially leading to a revenue and returns drag.

- Integration and management focus risks are heightened by the ongoing reorganization and decentralization of Markel Insurance and Ventures operations; if leadership cannot successfully execute, extract efficiencies, or maintain underwriting discipline, expense ratios may remain elevated, pressuring net margins and long-term profitability.

- The company remains exposed to industry-wide secular headwinds such as escalating litigation (particularly social inflation in casualty and D&O), intensifying regulatory oversight, and potential increases in capital requirements, all of which could further elevate loss costs, compliance expenses, or constrain capital available for growth and shareholder returns.

- Specialty market segments targeted by Markel may become increasingly commoditized or attract larger, better-capitalized competitors and insurtech disruptors, leading to downward pressure on pricing and market share-risking slower revenue growth and margin compression over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $2005.4 for Markel Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $17.6 billion, earnings will come to $2.1 billion, and it would be trading on a PE ratio of 14.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of $1879.85, the analyst price target of $2005.4 is 6.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Markel Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.