Last Update 18 Jun 26

Fair value Increased 44%AGX: AI Power Demand And Backlog Strength Will Meet Execution Risks

Argan's updated analyst fair value estimate has shifted from about $473 to roughly $680, as analysts point to a premium P/E assumption, a slightly lower discount rate, and modestly higher revenue growth expectations that are only partly offset by a lower projected profit margin.

Analyst Commentary

Recent Street research on Argan centers on higher fair value estimates and rating changes that reflect how analysts view the balance between the stock's execution, growth outlook, and current valuation.

Bullish Takeaways

- Bullish analysts are assigning a premium P/E multiple to Argan, citing what they see as a unique market position that, in their view, can support a higher valuation relative to peers.

- Several recent price target increases, including the move to US$600 and a separate US$119 uplift, indicate that these analysts see room for the stock price to align more closely with their higher fair value work.

- The pipeline of new projects is highlighted as a key support for Argan's revenue outlook, with bullish analysts pointing to it as a driver behind their more constructive targets.

- Following what is described as a strong Q4 report, JPMorgan upgraded Argan to Overweight, indicating greater confidence in the company’s execution and earnings power.

Bearish Takeaways

- At least one firm maintains a Hold rating even after lifting its price target to US$600, suggesting that some analysts see the stock price as already reflecting much of Argan's execution and project pipeline.

- The use of a premium multiple implies that Argan’s valuation is sensitive to any change in assumptions around its market position or project pipeline, which could weigh on the risk and reward profile if those assumptions are revised.

- Incremental price target increases, such as the US$50 adjustment, show that not all analysts are making large upward revisions, which can point to a more cautious stance on how much upside is embedded in Argan shares at current levels.

- While JPMorgan and Goldman Sachs have become more constructive, the presence of ongoing Hold ratings indicates that there is still disagreement across the Street about how much investors should be willing to pay for Argan’s growth story.

What’s in the News for Argan Stock

- Argan, Inc. reported record Q1 fiscal 2027 results, with revenue of US$291 million and net income of US$46.1 million, and adjusted EPS of US$3.24 that was described as ahead of analyst expectations, supported by strength across all three segments, especially Power. Source: Q1 FY27 earnings coverage, published January 1, 2025.

- The company’s project backlog was reported at about US$2.77b in Q1 fiscal 2027, with management indicating expectations of securing several additional projects over the following 10 to 18 months. This was described as reflecting ongoing activity in energy infrastructure and data center related work. Source: Q1 FY27 earnings coverage, published January 1, 2025.

- For fiscal 2026, Argan reported record revenue and net income and ended the year with a consolidated project backlog near US$2.9b, including roughly US$2.5b of new contracts tied to AI data centers, EVs, and manufacturing. Source: FY26 earnings coverage, published May 28, 2026.

- Argan increased its quarterly dividend multiple times over recent periods, including Q1 fiscal 2027, and extended and expanded its share repurchase authorization to US$200 million through January 31, 2030, with the company reporting completed repurchases of about 2,768,876 shares for US$113 million since 2020. Sources: Q1 FY27 earnings coverage, May 28, 2026 earnings coverage, company buyback updates dated April 8, 2026 and January 31, 2026.

- Management has signaled interest in acquisitions or investments that could add to existing capabilities or widen Argan’s geographic reach, with M&A described as an ongoing area of evaluation on the fiscal 2026 earnings call. Source: Fiscal 2026 earnings call commentary.

Valuation Changes for Argan Stock

- Fair Value: The updated analyst fair value estimate has moved from about $473.20 to roughly $679.80, a sizable upward reset in the valuation anchor used for Argan.

- Discount Rate: The discount rate has edged down slightly from 8.81% to about 8.77%, indicating a modestly lower required return in the refreshed model.

- Revenue Growth: Assumed revenue growth has shifted from roughly 20.50% to about 21.00%, reflecting a slightly higher top line outlook for Argan.

- Net Profit Margin: The expected net profit margin has eased from around 13.58% to roughly 13.17%, a small reduction in projected profitability.

- Future P/E: The forward P/E multiple has increased from about 38.0x to roughly 50.4x, implying a higher earnings multiple being applied to Argan stock in the latest analysis.

Key Takeaways

- Diversified project backlog and strong industry trends position Argan for multi-year revenue and margin growth, with expanded capabilities in energy, water, and recycling sectors.

- Robust financial health enables strategic investments and project execution advantages, supporting continued earnings growth and improved long-term profitability.

- Heavy dependence on large gas power projects and centralized infrastructure exposes Argan to significant risks from sector decarbonization, project volatility, and shifts in regulatory or market trends.

Catalysts

About Argan- Through its subsidiaries, provides engineering, procurement, construction, commissioning, maintenance, project development, and technical consulting services to the power generation market in the United States, Republic of Ireland, and the United Kingdom.

- The aging North American power infrastructure and rising electricity demand-driven by widespread electrification and the proliferation of AI data centers-are resulting in record project backlog and robust pipeline visibility for Argan. This is likely to drive sustained top-line revenue growth for several years.

- Strong secular investment momentum in grid modernization and the ongoing energy transition is accelerating the need for new construction of both natural gas-fired and renewable energy facilities. Argan's diversified capabilities position it to capitalize on this trend, potentially expanding its addressable market and supporting revenue growth.

- Record backlog and continued project wins across gas, renewables, water treatment, and recycling plants provide multi-year revenue visibility, indicating potential for increased operating leverage and higher gross margins as larger projects are executed successfully.

- Argan's reputation for on-time, on-budget project delivery and its expanded workforce enable it to handle more and larger projects than competitors, which is likely to support earnings growth and improve net margin stability over time.

- The company's strong balance sheet and consistently high net cash position allow it to pursue strategic M&A and invest in team expansion, enabling further scale and resilience, which can enhance earnings consistency and long-term profitability.

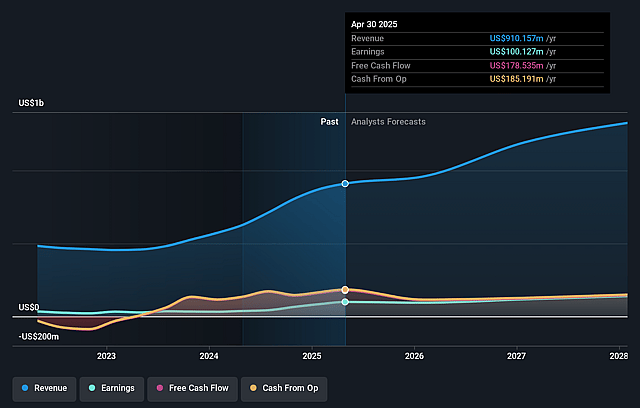

Argan Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Argan's revenue will grow by 21.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 15.5% today to 13.2% in 3 years time.

- Analysts expect earnings to reach $243.0 million (and earnings per share of $16.89) by about June 2029, up from $161.3 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $319.7 million in earnings, and the most bearish expecting $217.8 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 52.8x on those 2029 earnings, down from 62.5x today. This future PE is greater than the current PE for the US Construction industry at 45.8x.

- Analysts expect the number of shares outstanding to grow by 1.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.77%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Argan's backlog is heavily weighted toward natural gas-fired projects (61%), and management expects this trend to continue, exposing the company to long-term risk if the energy sector accelerates its transition to renewables and shifts away from gas plants; this could reduce project opportunities and future revenue over time.

- The company relies on a relatively small universe of large, complex EPC (Engineering, Procurement, Construction) projects, meaning any major project delays, cost overruns, or cancellations could lead to significant variability or declines in quarterly and annual earnings and net margins.

- While gross margins have recently improved due to strong project execution, management notes the margins are "lumpy" and cautions that sustainability at current levels is uncertain, particularly if competitive pressures intensify or project execution challenges arise; this may introduce volatility or downward pressure on long-term profitability.

- Despite record backlog and current industry demand, Argan's growth is tied to the cyclical nature of infrastructure and power-plant spending, which depends on favorable macroeconomic and regulatory conditions; shifts in government budgets, permitting, or utility investment cycles could cause unpredictable swings in revenue and net income.

- Although Argan is expanding its workforce and capacity, its business model remains concentrated in large-scale centralized power projects; a secular trend toward distributed generation, modular energy solutions, or more rapid decarbonization efforts could erode its core markets and lead to long-run revenue declines.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $679.8 for Argan based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $860.0, and the most bearish reporting a price target of just $500.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.8 billion, earnings will come to $243.0 million, and it would be trading on a PE ratio of 52.8x, assuming you use a discount rate of 8.8%.

- Given the current share price of $719.52, the analyst price target of $679.8 is 5.8% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Argan?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.