Last Update 23 Jun 26

Fair value Increased 0.074%YUMC: Brand Ownership And Store Expansion Will Support Future Re Rating

Analysts have nudged their fair value estimate for Yum China Holdings slightly higher to about $61.22, citing supportive views on the Pizza Hut brand acquisition in Mainland China as a positive earnings contributor within a still measured valuation framework.

Analyst Commentary

Analysts covering Yum China Holdings are weighing the Pizza Hut brand acquisition in Mainland China against broader execution and valuation questions, giving investors a mix of optimistic and cautious signals to consider.

Bullish Takeaways

- Bullish analysts describe the US$1.2b Pizza Hut brand acquisition as strategically positive for Yum China, arguing that direct brand ownership can support clearer decision making around product, marketing and long term investment.

- Some view the transaction price as reasonable, seeing the deal terms as aligned with a measured valuation framework rather than a stretch purchase for the company.

- Street commentary highlights expectations that the deal will be accretive to diluted EPS starting in 2026, with projections for mid single digit EPS accretion in 2027 and 2028, which bullish analysts see as supportive for earnings quality.

- Inclusion of Yum China on major institutional conviction lists, such as Goldman Sachs’ APAC Conviction List, signals confidence from some large research desks in the company’s ability to execute on its growth plans.

Bearish Takeaways

- Bearish analysts are cautious around the timing of earnings benefits, noting that the expected EPS accretion from the Pizza Hut deal does not begin until 2026, which leaves execution risk over the integration period.

- The US$1.2b cash outlay raises questions for some about capital allocation and future flexibility, especially if operating conditions or investment needs change before the deal fully contributes to earnings.

- Where price targets have been trimmed, it reflects concern that prior expectations for Yum China’s growth or execution may have been too optimistic, with analysts adjusting assumptions to reflect a more measured outlook.

- There is also a cautious view that Pizza Hut brand ownership alone does not guarantee improved performance, with future results likely to depend on how effectively Yum China manages menu, store economics and brand positioning after the transaction closes.

What’s in the News for Yum China Holdings

- Yum China is set to acquire Pizza Hut’s Mainland China operations from Yum! Brands for US$1.2b in cash as part of a broader US$2.7b sale of the global Pizza Hut business, with private equity firm LongRange Capital buying operations outside Mainland China, according to recent deal announcements.

- The transaction is expected to close in the third quarter of 2026 and will end Yum China’s royalty payments to Yum! Brands for Pizza Hut in Mainland China. Commentary around the deal links this change to potential margin improvement and faster earnings contribution once integration is underway.

- Yum China plans to expand Pizza Hut in Mainland China to more than 6,000 stores by 2028 and to double operating profit by 2029, based on company targets cited in the transaction summary from Yum! Brands.

- Yum! Brands has authorized a US$4b share repurchase program funded in part by net proceeds from the Pizza Hut sale, according to deal disclosures that outline capital return plans on the seller’s side.

- Separately, Yum China reported that from January 1, 2026 to March 31, 2026 it repurchased 4,122,000 shares for US$214.36m, bringing total buybacks under the program announced on February 7, 2017 to 103,041,696 shares, or 26.34% of shares, based on company filings.

Valuation Changes for Yum China Holdings

- Fair Value: Updated slightly higher from $61.17 to $61.22, reflecting a very small adjustment in the valuation model.

- Discount Rate: Adjusted upward from 9.39% to 9.61%, which implies a modestly higher required return in the updated assumptions.

- Revenue Growth: Held effectively steady at about 6.62%, with only a minimal numerical change in the projected growth rate.

- Net Profit Margin: Raised from 8.54% to 8.70%, indicating a small uplift in expected profitability for Yum China Holdings.

- Future P/E: Trimmed slightly from 18.29x to 18.09x, indicating a marginally lower earnings multiple in the updated valuation.

Key Takeaways

- Aggressive expansion in lower-tier cities and digital ecosystem investments fuel revenue growth, enhance customer engagement, and boost operational efficiency.

- Innovation in menu offerings and improved supply chain efficiency support market share gains, higher profitability, and resilience against increasing competition.

- Escalating costs, intensifying competition, and shifting consumer preferences may constrain sales growth, compress margins, and challenge Yum China's ability to sustain long-term earnings expansion.

Catalysts

About Yum China Holdings- Owns, operates, and franchises restaurants in the People’s Republic of China.

- Continued aggressive expansion into lower-tier Chinese cities and new store formats (including KCOFFEE Cafes and Pizza Hut WOW), combined with healthy new store payback periods, supports ongoing top-line revenue growth and market share gains by tapping into rising urbanization and a broadening middle class.

- Deepening digital ecosystem investments (e.g., Super App, Mini programs, AI-driven end-to-end digitization, frontline innovation fund) enhance customer engagement, drive higher frequency of transactions, and improve operational efficiencies-positively impacting both revenues and net margins.

- Rapid growth of the delivery business, with delivery now 45% of total sales and all brands available on major platforms, expands the addressable market and supports sustainable same-store sales growth, mitigating competition by leveraging scale and cross-channel synergies.

- Ongoing innovation in menu offerings (e.g., KFC product launches, Pizza Hut's new pizzas, value-driven "All-You-Can-Eat" campaigns, and branded collaborations) enables Yum China to capture evolving consumer preferences for branded, safe, and experiential dining, driving incremental transactions and pricing power.

- Supply chain improvements, store automation, and lower CapEx per store (alongside a growing franchise store mix) drive down cost ratios and G&A expense, enabling sustainable margin expansion and higher operating profits even in the face of labor cost pressures.

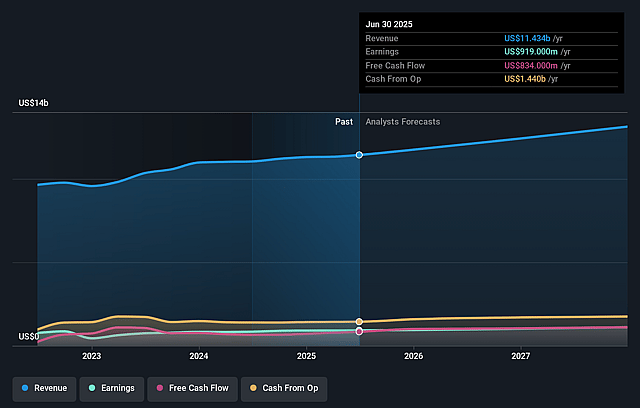

Yum China Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Yum China Holdings's revenue will grow by 6.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.8% today to 8.7% in 3 years time.

- Analysts expect earnings to reach $1.3 billion (and earnings per share of $3.95) by about June 2029, up from $946.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.4 billion in earnings, and the most bearish expecting $1.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 18.1x on those 2029 earnings, up from 15.2x today. This future PE is lower than the current PE for the US Hospitality industry at 23.1x.

- Analysts expect the number of shares outstanding to decline by 6.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.61%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition and aggressive discounting on delivery platforms, especially from digital-native and local Chinese QSR brands, could erode market share and limit Yum China's pricing power, resulting in downward pressure on same-store sales growth and net margins.

- The ongoing shift to a higher delivery mix, while expanding sales reach, is structurally increasing rider costs as a percentage of sales, which may compress restaurant margins and limit operating profit growth if labor cost inflation persists.

- Mix shift toward smaller-ticket orders (e.g., beverages, breakfast), and aggressive expansion into lower-tier cities with inherently lower ticket averages, may dilute average check size and restrain top-line revenue growth, even if transaction volumes increase.

- Reduced tailwind from commodity price declines, coupled with rising labor and delivery costs, may result in margin headwinds and create challenges in maintaining value-for-money offerings, limiting potential earnings expansion.

- Reliance on Western core brands (KFC, Pizza Hut) and slower testing or scaling of innovative formats (like Pizza Hut WOW) exposes the company to shifting consumer preferences towards healthier, more local, or niche QSR options, increasing the risk of stagnating same-store sales and impacting long-term revenue and profit stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $61.22 for Yum China Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $77.0, and the most bearish reporting a price target of just $54.2.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $14.7 billion, earnings will come to $1.3 billion, and it would be trading on a PE ratio of 18.1x, assuming you use a discount rate of 9.6%.

- Given the current share price of $41.53, the analyst price target of $61.22 is 32.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Yum China Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.