Last Update 25 Jun 26

CPK: Dividend Hike And Steady Execution Will Support Future Re Rating

The analyst price target for Chesapeake Utilities has changed by $2, with analysts citing recent neutral coverage and updated valuation views as key reasons for the adjustment.

Analyst Commentary

Recent Street research on Chesapeake Utilities highlights a mix of optimism about the company’s execution and valuation, alongside a more neutral stance on how much upside is currently reflected in the stock.

Bullish Takeaways

- Bullish analysts point to the updated price target as recognition that current fundamentals and execution support a modestly higher valuation for Chesapeake Utilities.

- The price target adjustment signals confidence that the company’s existing projects and operations can sustain its current profile, which some see as reasonably aligned with the new valuation views.

- Supportive commentary around the stock suggests that, at the updated target, Chesapeake Utilities is seen as fairly positioned in its peer group based on available information about its business mix and risk profile.

- The initiation of coverage, even with a neutral stance, indicates that Chesapeake Utilities is now more firmly on the radar of institutional research teams, which some investors view as helpful for liquidity and visibility.

Bearish Takeaways

- Bearish analysts maintain a neutral rating, which implies that, in their view, the current share price already reflects much of the available information on Chesapeake Utilities, limiting the perceived upside at this stage.

- Neutral coverage also suggests ongoing caution around how much investors are willing to pay for the company relative to its current earnings profile and growth opportunities, given the data available to the Street.

- Commentary around valuation indicates that, while the target moved by US$2, some analysts remain hesitant to take a more positive stance without clearer evidence on execution or new growth drivers.

- The absence of a more positive rating, despite the adjusted target, signals that some research views Chesapeake Utilities as more of a hold than a clear opportunity, based on present information.

What’s in the News for Chesapeake Utilities

- Chesapeake Utilities declared a quarterly dividend of US$0.7350 per share, with a stated payable date of July 6, 2026, and an ex dividend and record date of June 15, 2026. (Source: Key Developments)

- The company reaffirmed earnings guidance for 2028, with an EPS range of US$7.75 to US$8.00 per share. (Source: Key Developments)

- At a board meeting scheduled for May 6, 2026, Chesapeake Utilities planned to consider and approve a change in the quarterly cash dividend on common stock from US$0.685 per share to US$0.735 per share. (Source: Key Developments)

Valuation Changes for Chesapeake Utilities

- Fair Value: Model fair value remains unchanged at $145.80 per share, indicating no adjustment in the central valuation estimate.

- Discount Rate: The discount rate is effectively stable at 7.11%, with only an immaterial rounding difference versus the prior figure.

- Revenue Growth: Forecast revenue growth is essentially unchanged at 4.52%, suggesting no revision to Chesapeake Utilities’ top line assumptions in the model.

- Net Profit Margin: Projected net profit margin is steady at 18.10%, reflecting consistent expectations for future profitability.

- Future P/E: The future P/E assumption remains around 22.0x, indicating no material shift in the valuation multiple applied to Chesapeake Utilities’ forward earnings.

Key Takeaways

- Modernizing energy infrastructure and expanding into high-growth regions positions Chesapeake Utilities for sustained revenue and margin growth.

- Strategic diversification into alternative fuels, along with regulatory successes and operational efficiencies, enhances earnings stability and long-term profitability.

- Heavy capital spending and geographic concentration, coupled with regulatory and decarbonization risks, threaten future margin expansion and expose the company to operational and financial vulnerability.

Catalysts

About Chesapeake Utilities- Operates as an energy delivery company in the United States.

- Substantial capital investment in energy infrastructure modernization (~$213M in first half 2025 and increased annual guidance to $375M–$425M) positions Chesapeake Utilities to capture growing demand and supports durable future rate base growth, directly boosting long-term revenue and earnings potential.

- Accelerating customer and population growth in high-expansion regions such as Florida and the Delmarva Peninsula (Q2 2025 residential customer growth of 4.2% in Delmarva, 3% in Florida) increases natural gas demand and enables incremental margin growth from customer additions, supporting revenue and net margin expansion.

- Strategic pipeline and RNG/alternative fuels projects (e.g., data center-related pipeline in Ohio, three new RNG transportation projects) broaden service offerings and tap into decarbonization trends, allowing for new revenue streams and improved margin mix over time.

- Favorable regulatory outcomes and constructive relationships (recent rate case approvals in Maryland, Delaware, Florida; successful interim FERC approvals for major projects) reduce earnings volatility and enable timely recovery of infrastructure investments, supporting steady net income and improved cash flow visibility.

- Ongoing business process improvements and ERP/IT upgrades drive operational efficiencies and cost management, amplifying the positive impact of revenue growth on adjusted net income and supporting higher future margins.

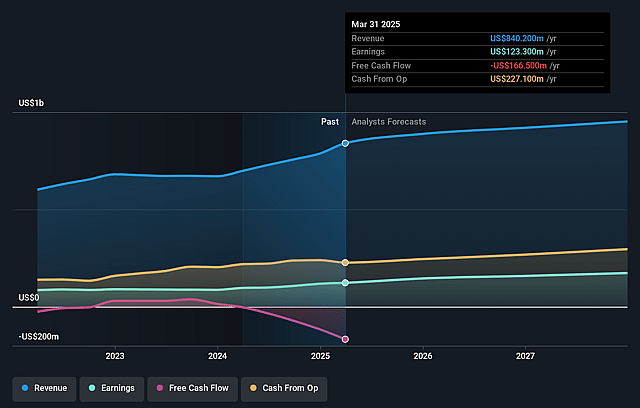

Chesapeake Utilities Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Chesapeake Utilities's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.1% today to 18.1% in 3 years time.

- Analysts expect earnings to reach $203.4 million (and earnings per share of $8.05) by about June 2029, up from $148.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 22.4x on those 2029 earnings, up from 19.7x today. This future PE is greater than the current PE for the US Gas Utilities industry at 17.3x.

- Analysts expect the number of shares outstanding to grow by 1.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Elevated capital spending requirements-such as the projected $1.5–$1.8 billion 5-year capital plan and recent $50 million increase in annual CapEx guidance-may necessitate higher debt and equity issuance, increasing financial leverage and diluting returns, which could compress net margins and earnings.

- Continued dependence on growth in specific service regions (Delmarva, Florida) and heavy investment in infrastructure for natural gas delivery may expose Chesapeake Utilities to geographic concentration risk, leaving revenue and customer growth vulnerable to adverse regulatory actions or demographic/economic shifts in these areas.

- Sustained margin growth assumptions rely on customer adoption of natural gas for new developments, but accelerating secular decarbonization and electrification trends (e.g., public policies or shifts toward all-electric construction) could reduce long-term demand, jeopardizing future revenues and project returns.

- A successful outcome in the Florida City Gas depreciation study is assumed in 2025 full-year EPS guidance; failure to secure this regulatory approval, or regulatory pushback elsewhere, could result in higher ongoing depreciation expense and reduced net income, impacting earnings targets.

- Partial offset of strong transmission/distribution margins by rising O&M, depreciation, and financing expenses-as highlighted by cost overruns in projects (e.g., the LNG storage facility)-suggests operational or construction execution risk, which could erode projected margin/earnings growth if costs continue to rise or if regulatory cost recovery is delayed or denied.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $145.8 for Chesapeake Utilities based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.1 billion, earnings will come to $203.4 million, and it would be trading on a PE ratio of 22.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of $122.04, the analyst price target of $145.8 is 16.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Chesapeake Utilities?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.