Last Update 24 Jun 26

Fair value Increased 1.42%AMH: Leasing Momentum And Housing Act Revisions Will Shape Balanced Forward Outlook

The updated analyst price target for American Homes 4 Rent edges higher by about $0.50, with analysts pointing to slightly stronger revenue growth assumptions, a modestly lower discount rate, and a small uplift in projected profit margins and future P/E.

Analyst Commentary

Recent Street research on American Homes 4 Rent points to a mix of optimism and caution, with several firms adjusting price targets in a relatively tight range and revisiting their views on single family rental real estate investment trusts and broader REIT subsectors.

Bullish Takeaways

- Bullish analysts highlight American Homes 4 Rent as part of the single family rental group where they see a lower hurdle to meet blended rent outlooks in the second half of 2026. They view this as supportive for earnings execution over time.

- Some bullish analysts point to early reads for 2027 that suggest the single family rental group could offer better growth potential versus apartments. They frame AMH as a way to gain exposure to that theme if it plays out.

- There is an upgrade to an Outperform rating with a US$35 price target. The analyst cites signs that single family rental leasing demand is accelerating, which they see as constructive for occupancy and revenue visibility.

- Supportive commentary around recent housing legislation, where a revised bill is described as more industry friendly and removes a provision on forced dispositions while allowing continued purchases from homebuilders, is viewed by bullish analysts as reducing policy risk around AMH's growth approach.

Bearish Takeaways

- Some cautious analysts maintain Neutral views and keep price targets around the low to mid US$30s. They signal that they see American Homes 4 Rent as fairly valued relative to its current execution and growth profile.

- There are references to REIT valuations being less attractive following a strong start to the year. This contributes to more restrained positioning on AMH even where price targets move slightly higher.

- A small reduction in a price target to US$32 from US$33 reflects a more measured stance from bearish analysts, who appear wary about paying up for the stock without clearer upside to earnings or cash flow.

- The comment that sector views on some REIT subsectors have been lowered to Marketweight due to relative valuation, while not specific only to AMH, reinforces a broader caution that could limit how aggressively some investors are willing to price American Homes 4 Rent.

What’s in the News for American Homes 4 Rent

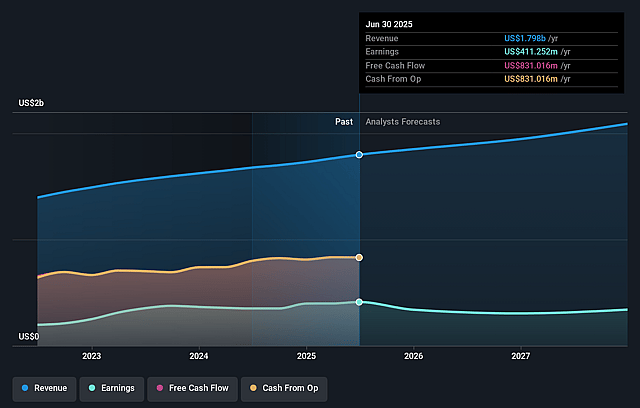

- American Homes 4 Rent reported Q1 2026 funds from operations of $0.48 per share, in line with estimates and up from $0.46 a year earlier, with revenues of about $472 million that were slightly above consensus expectations. Source: Recent Q1 2026 earnings coverage.

- The company delivered more than 500 newly constructed, energy efficient homes and sold over 700 non core properties, generating roughly $200 million in proceeds as part of a capital recycling program, while maintaining full year 2026 guidance. Source: Recent Q1 2026 earnings coverage.

- Management highlighted record March leasing volumes, higher occupancy, increased rents, and 3.7% same home core net operating income growth, indicating steady demand for single family rentals and a focus on disciplined capital allocation. Source: Recent Q1 2026 earnings coverage.

- American Homes 4 Rent repurchased around $360 million of common stock over six months and separately completed a tranche of 3,200,000 share repurchases for $94 million between February 1 and April 30, 2026, under a previously announced buyback. Source: Company buyback update.

- The company has an at the market follow on equity program filed for up to $1 billion and has completed an offering of approximately $246.3 million of Class A common shares across multiple tranches at prices in the mid US$36 to US$37 range. Source: Follow on equity offering filings.

Valuation Changes for American Homes 4 Rent

- Fair Value: Updated estimate has risen slightly to $35.77 from $35.27.

- Discount Rate: Assumed rate has edged lower to 7.32% from 7.35%, which implies a modestly higher present value for projected cash flows.

- Revenue Growth: Modeled long term revenue growth has ticked up to 3.45% from 3.38%.

- Net Profit Margin: Forecast margin has moved slightly higher to 10.50% from 10.47%.

- Future P/E: Assumed forward P/E multiple has increased modestly to 67.60x from 67.04x.

Key Takeaways

- Elevated development and maintenance costs from tariffs and material fluctuations may compress net margins if not passed to renters.

- Competition and shifting consumer preferences in key markets could challenge revenue growth and impact expectations negatively.

- Strong demand, strategic diversification, and a unique development program position American Homes 4 Rent for stable revenue growth and improved financial resilience.

Catalysts

About American Homes 4 Rent- AMH (NYSE: AMH) is a leading large-scale integrated owner, operator and developer of single-family rental homes.

- The increase in homeownership costs, driven by high mortgage rates and increased insurance expenses, may lead to a further gap between renters and homeowners. This could reduce demand and impact revenue growth as fewer families choose to rent (revenue).

- American Homes 4 Rent's continuation of its lease expiration management strategy could result in short-term increases in turnover, potentially raising operating expenses and affecting net margins adversely (net margins).

- Potential new tariffs and fluctuations in labor and material costs could elevate development and maintenance costs, leading to compressed net margins if these cost increases cannot be passed through to renters (net margins).

- Potential headwinds in the macroeconomic environment, such as job market fluctuations, may disrupt the leasing dynamics, ultimately affecting occupancy rates and revenue growth (revenue).

- The company's current strategy and geographic footprint focus, particularly in markets like North Florida and Texas, where competition from public builders is increasing, may challenge revenue growth expectations if consumer preferences shift or supply becomes saturated (revenue).

American Homes 4 Rent Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming American Homes 4 Rent's revenue will grow by 3.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 24.4% today to 10.5% in 3 years time.

- Analysts expect earnings to reach $216.5 million (and earnings per share of $0.73) by about June 2029, down from $455.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $295.8 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 67.7x on those 2029 earnings, up from 25.7x today. This future PE is greater than the current PE for the US Residential REITs industry at 30.5x.

- Analysts expect the number of shares outstanding to decline by 2.78% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- American Homes 4 Rent (AMH) is experiencing strong demand due to a persistent supply and demand imbalance in the U.S. housing market, positioning the company for continued revenue growth.

- AMH's unique in-house development program allows them to deliver new inventory to an undersupplied market, which can provide a strong foundation for sustained, future revenue and earnings.

- The company benefits from a high resident retention rate, exceeding 70%, and has an industry-leading customer experience, reflected by a national Google score of 4.7 out of 5 stars, contributing to stable and potentially consistent revenue streams.

- The positive revision of AMH's credit rating by S&P Global suggests improved access to capital markets and a stronger financial position, potentially stabilizing or improving net margins and earnings.

- AMH's strategic focus on high-quality markets and intentional geographic diversification within its portfolio limits its exposure to localized economic downturns, therefore maintaining stable or potentially improving financial results across varying market conditions.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $35.77 for American Homes 4 Rent based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $32.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.1 billion, earnings will come to $216.5 million, and it would be trading on a PE ratio of 67.7x, assuming you use a discount rate of 7.3%.

- Given the current share price of $32.46, the analyst price target of $35.77 is 9.3% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on American Homes 4 Rent?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.