Last Update 15 Jul 26

Fair value Decreased 13%FDX: Network 2.0 Execution And Freight Spin Will Drive Future Repricing

The updated analyst price target framework for FedEx now centers around approximately $351, down from about $402. Analysts are factoring in slower projected revenue growth alongside slightly higher margin and profitability expectations under the company's post Freight spin structure and Network 2.0 plan.

Analyst Commentary

Recent Street research around FedEx reflects a mix of confidence in the company’s execution on its post Freight spin structure and Network 2.0 plan, alongside questions about timing, complexity and valuation. The spread of price targets, which now cluster around the mid US$300s with outliers on both the high and low end, highlights how differently analysts are framing the risk and reward.

Bullish Takeaways

- Bullish analysts point to FedEx’s multi lever transformation, including Network 2.0, DRIVE cost initiatives and tighter capex oversight, as a key reason to back management’s ability to support margins and earnings over time.

- Several research updates describe the Freight spin and calendar year shift as clarifying the parcel focused story, with FedEx seen as well positioned to benefit from an improving industrial backdrop and disciplined capital returns via buybacks and dividends.

- Positive commentary around recent earnings highlights strong execution, with some analysts viewing earlier than expected profitability and a sizable earnings framework as supportive of higher valuation multiples.

- Upgrades and resumed positive ratings, including from firms such as JPMorgan, emphasize that structural improvements in the core FedEx business are becoming more visible and that long term targets are viewed as credible by supportive analysts.

Bearish Takeaways

- Bearish analysts focus on the complexity surrounding the Freight spin, calendar year transition and new reporting structure, seeing a risk that near term results and guidance are harder to interpret and that execution could be uneven as disclosures roll out.

- Some price target cuts frame the stock as more balanced, with macro conditions and cost savings already reflected in estimates, which limits upside if FedEx does not consistently deliver against its earnings and margin goals.

- Commentary highlighting softer performance in certain segments and expectations for margin pressures to outweigh stable revenue trends in specific periods points to concern that profitability may prove more volatile than the current valuation implies.

- The presence of at least one underweight rating alongside reduced targets in the low US$300s and near US$160 illustrates that not all analysts are comfortable with the transformation risk, especially while investors wait for full standalone visibility into the parcel and Freight businesses.

What’s in the News for FedEx

- FedEx stock recently rose about 3.3% after double upgrades from Barclays and Stephens and approval of a new collective bargaining contract covering roughly 5,000 pilots, which removed a key operational uncertainty for the company (source: FedEx double upgrade and pilot contract story).

- CMA CGM agreed to acquire FedEx Supply Chain, the company’s third party logistics unit, for US$1.4b in cash in a transaction expected to close in 2026. FedEx is focusing on core express and ground operations and plans multi year commercial agreements with CMA CGM for air and ocean freight services (source: CMA CGM to acquire FedEx Supply Chain story).

- FedEx reported fiscal Q4 2026 adjusted EPS of US$6.31 and revenue of US$25.01b, both above consensus estimates, alongside completion of the FedEx Freight spin off that delivered a US$4.1b cash dividend. Shares fell 5% to 6% after hours on a cautious fiscal 2027 earnings outlook and recent insider selling of about US$18.6m (source: FedEx Q4 earnings and Freight spin off story).

- FedEx launched cash tender offers for up to US$4.15b of outstanding notes, funded in part by the US$4.1b dividend from FedEx Freight, as part of an effort to manage debt levels and maintain a leverage neutral balance sheet (source: FedEx debt tender offer story).

- FedEx is facing fresh competitive pressure as Amazon Shipping targets FedEx and UPS customers with aggressive pricing and waived surcharges, which has been linked to share price pressure on traditional parcel carriers (source: Amazon going after FedEx and UPS customers story).

Valuation Changes for FedEx

- Fair Value: The updated FedEx fair value estimate has fallen meaningfully from about $401.89 to roughly $351.49, reflecting a lower central price target level.

- Discount Rate: The discount rate has risen slightly from about 8.63% to around 8.87%, implying a modestly higher required return on FedEx shares.

- Revenue Growth: The revenue growth assumption has fallen significantly from roughly 4.63% to about 1.01%, indicating a more muted top line outlook for FedEx in the model.

- Profit Margin: The net profit margin has edged up from around 5.53% to roughly 5.66%, signaling a small improvement in expected profitability for FedEx.

- Future P/E: The future P/E multiple has eased slightly from about 21.76x to around 21.01x, pointing to a modestly lower valuation multiple applied to FedEx earnings.

Key Takeaways

- Cost-saving initiatives and network optimization projects are set to enhance FedEx's margins and earnings through improved efficiency and reduced expenses.

- Strategic investments and technological enhancements, including in Europe, aim to drive revenue growth and improve customer experiences.

- Various external and internal challenges, including contract expiration, economic pressures, and restructuring risks, threaten FedEx's revenue stability, margins, and future profitability.

Catalysts

About FedEx- Provides transportation, e-commerce, and business services in the United States and internationally.

- FedEx's DRIVE initiative is achieving significant cost savings, with a target of $2.2 billion for FY '25 and a total of $4 billion compared to the FY '23 baseline. This initiative is expected to enhance net margins through structural cost reductions.

- The Network 2.0 project aims to optimize 50 U.S. stations, streamlining operations to improve efficiency. By enabling about 12% of FedEx's daily global volume to flow through optimized facilities by the end of FY '25, this initiative should positively impact operating margins and earnings.

- The Tricolor strategy improves asset utilization by optimizing aircraft density and leveraging the surface network. Progress in this area has already increased payloads and density in the air network, which should lead to revenue growth and enhanced net margins.

- FedEx's strategic initiatives in Europe, including a simplified technology platform, have led to improved operational efficiency and better customer experiences. This progress is expected to drive profitable share growth and improve revenue from the European market.

- The acquisition of RouteSmart Technologies will support FedEx's global route optimization, enhancing efficiency across the network transformation efforts. This is anticipated to reduce costs and enable better earnings performance.

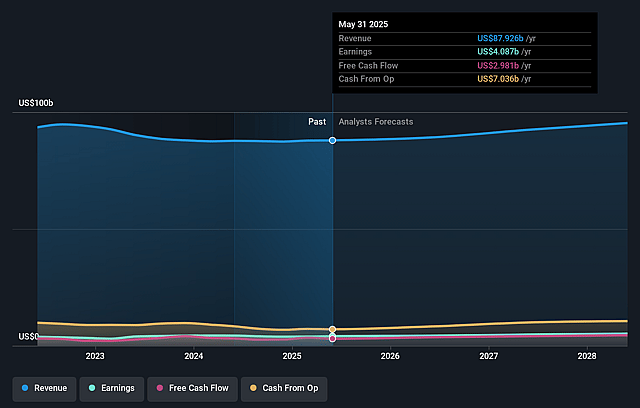

FedEx Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming FedEx's revenue will grow by 1.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.7% today to 5.7% in 3 years time.

- Analysts expect earnings to reach $5.5 billion (and earnings per share of $24.57) by about July 2029, up from $4.4 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.1x on those 2029 earnings, up from 16.9x today. This future PE is greater than the current PE for the US Logistics industry at 16.9x.

- Analysts expect the number of shares outstanding to grow by 2.16% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.87%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The expiration of the United States Postal Service contract and severe weather events are cited as significant headwinds, impacting adjusted operating income at Federal Express Corporation. This could create challenges for FedEx's revenue and earnings sustainability.

- Weakness in the industrial economy continues to pressure higher-margin B2B volumes, particularly affecting Freight, resulting in fewer shipments and lower weights, which could negatively impact FedEx’s revenues and net margins.

- The ongoing challenges in the global industrial economy, inflationary pressures, and the uncertainty surrounding global trade policies are leading to a reduction in FedEx's FY '25 adjusted EPS outlook. This could pressure future earnings.

- FedEx has experienced significant pricing and yield pressures in international shipping markets, which, compounded with increased demand for lower-yield deferred service offerings, could impact revenue quality and operating margins.

- The changes and eventual separation of FedEx Freight and the costs associated with restructuring initiatives may introduce execution risks and additional expenses, potentially affecting financial stability and future profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $351.49 for FedEx based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $479.0, and the most bearish reporting a price target of just $160.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $97.6 billion, earnings will come to $5.5 billion, and it would be trading on a PE ratio of 21.1x, assuming you use a discount rate of 8.9%.

- Given the current share price of $313.66, the analyst price target of $351.49 is 10.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on FedEx?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.