Last Update09 Oct 25Fair value Decreased 2.03%

The analyst price target for Tri Pointe Homes was lowered from $39.40 to $38.60. This change reflects concerns among analysts about near-term earnings declines following the company's reduced speculative home builds.

Analyst Commentary

Recent changes in analyst ratings highlight both optimism about Tri Pointe Homes' long-term potential and caution regarding near-term execution challenges.

Bullish Takeaways- Bullish analysts acknowledge that the company's shares are trading at a discounted valuation compared to peers, which could present upside for long-term investors.

- There remains confidence in Tri Pointe's overall strategic positioning within the homebuilding sector. This provides a foundation for future growth when market conditions improve.

- Opportunities for improved operating efficiency and a potential rebound in speculative builds are seen as possible future catalysts for earnings recovery.

- Bearish analysts are concerned that the reduction in speculative home builds will hinder near-term revenue streams and slow the pace of new orders.

- The interruption in the company's growth story is leading to forecasts of earnings declines over the next several quarters.

- There is increased caution regarding execution risk as the company navigates a shifting demand environment and adjusts its build strategy.

- Persistent uncertainty around housing market trends adds to the headwinds facing Tri Pointe's short-term performance and valuation.

What's in the News

- Tri Pointe Homes is launching sales at McCormick Trails in Port Orchard, introducing 30 new single-family homes surrounded by protected natural space and equipped with advanced HomeSmart technology. (Company announcement)

- The company is expanding in Utah with the opening of its first-ever community, Polaris at Terraine in West Jordan. This marks the start of five planned neighborhoods in the state. (Company announcement)

- In the Raleigh region, new communities The Townes at NoVi in Chatham Park and Summit at Homestead in Chapel Hill have been unveiled, offering modern townhome options and enhanced amenities. (Company announcement)

- Tri Pointe Homes is raising its equity buyback authorization by $50 million to a total of $300 million. Recent repurchases total $175.01 million to date. (Company announcement)

- Updated earnings guidance anticipates delivering 1,000 to 1,100 homes in the third quarter at an average price between $675,000 and $685,000. Projections call for 4,800 to 5,200 homes for full-year 2025. (Company guidance)

Valuation Changes

- Consensus Analyst Price Target has declined from $39.40 to $38.60, reflecting a moderate downward revision in perceived fair value.

- Discount Rate has risen slightly, moving from 9.16% to 9.23%. This indicates a marginal increase in the risk premium applied to future cash flows.

- Revenue Growth estimates remain essentially unchanged at approximately -7.48%.

- Net Profit Margin has edged down from 6.05% to 5.93%, suggesting a minor decrease in expected profitability.

- Future P/E ratio is nearly stable, increasing slightly from 18.79x to 18.82x.

Key Takeaways

- Expansion into high-growth regions and focus on sustainable, premium homes position the company to benefit from shifting demographic and consumer trends.

- Prudent land management, strong liquidity, and aggressive share buybacks enhance resilience, profitability, and long-term shareholder value.

- Heavy reliance on high prices, concentrated markets, and affluent buyers exposes Tri Pointe to local risks, shrinking demand, and margin pressures in softening housing conditions.

Catalysts

About Tri Pointe Homes- Engages in the design, construction, and sale of single-family attached and detached homes in the United States.

- Tri Pointe is positioned to benefit from the sustained U.S. housing supply-demand imbalance and favorable demographic trends, which are expected to provide a long runway for revenue growth as household formation continues to outpace new home supply.

- Ongoing expansion into high-growth Sun Belt and Southeastern markets (Florida, Coastal Carolinas, Utah) broadens Tri Pointe's geographic footprint and capitalizes on migration patterns and hybrid/remote work trends, which should support higher sales volumes and revenue visibility.

- Strategic discipline in land acquisition, strong liquidity ($1.4B), and active inventory management create a robust lot pipeline and flexibility to capitalize on growth opportunities, likely supporting steady backlog conversion, reduced risk of asset write-downs, and improved return on equity.

- Continued prioritization of a premium, energy-efficient product offering aligns with rising consumer demand for sustainable homes, which is expected to enable better pricing power and bolster net margins long-term as regulatory and buyer preferences shift.

- Aggressive share repurchases (over 5% share reduction YTD; trading below book value), along with digital sales/customer experience investments, are expected to drive long-term EPS growth and operating margin improvement, enhancing shareholder returns even if near-term conditions are challenging.

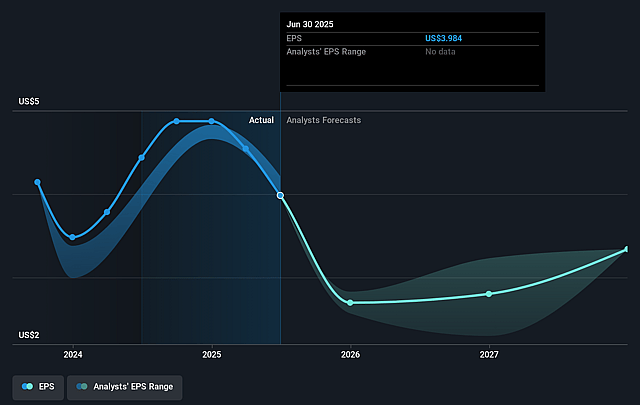

Tri Pointe Homes Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Tri Pointe Homes's revenue will decrease by 7.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 9.0% today to 6.0% in 3 years time.

- Analysts expect earnings to reach $193.6 million (and earnings per share of $3.34) by about September 2028, down from $365.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.8x on those 2028 earnings, up from 8.5x today. This future PE is greater than the current PE for the US Consumer Durables industry at 11.5x.

- Analysts expect the number of shares outstanding to decline by 6.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.16%, as per the Simply Wall St company report.

Tri Pointe Homes Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Tri Pointe's home orders declined 25% year-over-year compared to low single-digit declines for peers, indicating potential loss of market share or diminished demand relative to competitors, which could pressure future revenue and earnings growth.

- The company continues to prioritize price over sales pace, resulting in slower absorption rates and higher incentives, and with absorption trending toward the lower end of its target range (2.5 homes per community/month), this approach could compress gross margins if market demand remains weak and incentives must rise further.

- Geographic concentration in markets such as California and the Western U.S. (where regions like Northern California and Sacramento have shown softness and required inventory impairment charges) exposes Tri Pointe to outsized local risks and potential further margin and asset write-down impacts.

- Persistent affordability issues due to high home prices, increasing incentives, elevated interest rates, and dependence on well-off buyers (average household income $220,000), could limit the pool of potential buyers, diminishing volume growth and pressuring both revenue and net margins in the long term.

- Ongoing investment in land (with a significant portion owned rather than optioned) and the risk of inventory build-up or impairment in slower markets leave Tri Pointe vulnerable to cyclical downturns, which could result in further write-downs or depressed future returns on equity, impacting long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $39.4 for Tri Pointe Homes based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.2 billion, earnings will come to $193.6 million, and it would be trading on a PE ratio of 18.8x, assuming you use a discount rate of 9.2%.

- Given the current share price of $35.49, the analyst price target of $39.4 is 9.9% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.