Last Update 14 May 26

Fair value Increased 0.21%JNJ: Future Drug Cycle And Legal Outcomes Are Expected To Shape Returns

Analysts have nudged their average price target on Johnson & Johnson slightly higher to about $253, citing stronger momentum from new drugs like Icotyde and Inlexzo, along with increased confidence in the pipeline highlighted in recent research updates.

Analyst Commentary

Recent research on Johnson & Johnson clusters around the same core themes you are seeing in price target moves, with most commentary tied to execution on new products, confidence in the pipeline, and how the company is positioned within healthcare more broadly.

Bullish Takeaways

- Bullish analysts see Icotyde and Inlexzo as central to the story, with higher forecasts for these drugs feeding directly into higher revenue expectations and supporting higher valuation ranges.

- Several firms have raised their price targets, often linking those changes to updated views on near term pipeline assets such as Tecvayli and Inlexzo, and to the contribution from products like Tremfya in inflammatory bowel disease.

- Some research points to Johnson & Johnson as relatively insulated from some technology related disruption, with references to lower exposure to AI risk and the potential for healthcare stocks to attract investors when macro and geopolitical risks feel elevated.

- Coverage initiations and rating upgrades cited in the research flow suggest that, for bullish analysts, the product cycle is still in progress, and that execution on this cycle is a key reason to stay constructive on long term growth potential.

Bearish Takeaways

- Even within a generally positive backdrop, some firms maintain Neutral views, highlighting that a portion of the recent optimism is already reflected in current price targets and that further upside may depend on clean execution of the pipeline.

- References to an "uncertain macro backdrop" and rising geopolitical risk underline that broader market conditions could affect how much investors are willing to pay for Johnson & Johnson, regardless of company specific progress.

- Where analysts point to increasing out year revenue estimates, they also implicitly flag risk, since any disappointment on products like Tecvayli, Inlexzo, or Tremfya could weigh on sentiment if actual performance does not align with these higher expectations.

What’s in the News

- Johnson & Johnson is weighing a potential sale of its DePuy Synthes orthopedics unit, with reports suggesting the business could be valued at more than US$20b after generating US$9.3b in sales last year. Several private equity firms are said to be evaluating bids (Bloomberg).

- A California judge overturned a US$950m punitive damages award in a talc case, ruling that plaintiffs had not shown Johnson & Johnson acted with malice or concealed required information. Separate proceedings saw a Canada-wide talc class action certified and a Philadelphia jury award US$250,000 in an ovarian cancer case, highlighting ongoing legal complexity around legacy talc products (Reuters, Canadian court filing, Philadelphia Court of Common Pleas).

- The FDA approved ICOTYDE, described as the first targeted oral peptide that blocks the IL-23 receptor, for moderate to severe plaque psoriasis in adults and certain adolescents. This adds a new oral systemic option alongside ongoing ICOTYDE studies in psoriatic arthritis, ulcerative colitis and Crohn’s disease (company announcement).

- In multiple sclerosis adjacent immunology and autoimmune areas, Johnson & Johnson advanced nipocalimab with a supplemental Biologics License Application filed and later granted Priority Review for warm autoimmune hemolytic anemia. The company also secured Fast Track designation for systemic lupus erythematosus, indicating an expanding late stage pipeline in rare autoantibody driven diseases (company announcements).

- In oncology and hematology, the FDA approved TECVAYLI plus DARZALEX FASPRO for adults with relapsed or refractory multiple myeloma after at least one prior line of therapy, based on Phase 3 data showing a lower risk of progression or death versus standard regimens. The company also reported early clinical data for pasritamig in metastatic castration resistant prostate cancer and advanced bleximenib for acute myeloid leukemia under a new funding agreement with Blackstone Life Sciences (company announcements).

Valuation Changes

- Fair Value: The intrinsic value estimate has risen slightly from $252.42 to $252.96 per share, a move of about 0.2%.

- Discount Rate: The discount rate has edged higher from 6.98% to 7.11%, which can modestly reduce the present value assigned to future cash flows.

- Revenue Growth: The long term revenue growth assumption has been adjusted slightly, from 6.50% to 6.54%.

- Profit Margin: The projected net profit margin has eased fractionally from 23.13% to 23.10%.

- Future P/E: The assumed future P/E multiple has fallen from 29.46x to 27.83x, suggesting a lower valuation multiple applied to forward earnings in the model.

Key Takeaways

- Johnson & Johnson is poised for growth in immunology and oncology despite facing challenges from loss of drug exclusivity, leveraging next-gen therapies for strengthened revenue.

- Strategic investments in U.S. operations, acquisitions, and MedTech expansion aim to boost future earnings and efficiency, with potential restructuring in surgery to aid profitability.

- Loss of exclusivity for key products and tariffs could significantly threaten revenue and margins, while ongoing litigation poses financial risks.

Catalysts

About Johnson & Johnson- Engages in the research and development, manufacture, and sale of various products in the healthcare field worldwide.

- Johnson & Johnson anticipates accelerated growth in their portfolio and pipeline, particularly in the Innovative Medicine sector, despite the headwind from STELARA's loss of exclusivity. This is expected to bolster revenues through next-generation therapies and significant market share gains in oncology and immunology.

- The company's substantial investment of over $55 billion into manufacturing, R&D, and technology in the U.S. over the next four years is projected to expand capacity for advanced medicines and devices, potentially increasing operational efficiency and future earnings.

- Recent acquisitions, such as Intra-Cellular Therapies, are expected to contribute substantial revenue streams, with products like CAPLYTA potentially reaching over $5 billion in peak sales, positively affecting the company’s revenue and EPS in the future.

- Ongoing expansion within MedTech, highlighted by strong performance from acquired cardiovascular units Abiomed and Shockwave, as well as developments in robotic surgery, are expected to drive revenue growth and enhance adjusted income margins over time.

- The company plans significant restructuring in their surgery business within MedTech to streamline operations and improve efficiency, anticipated to have short-term revenue disruptions but expected to enhance long-term profitability and margin expansion.

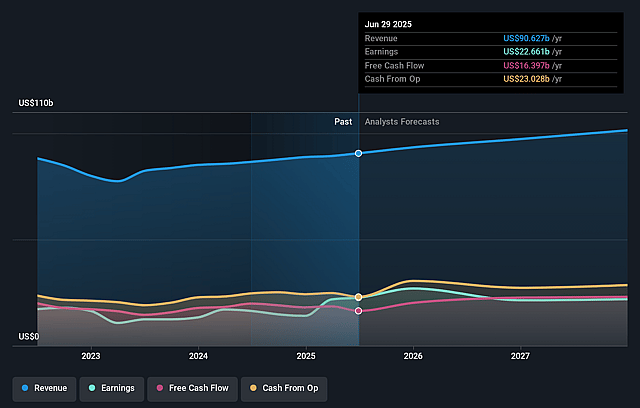

Johnson & Johnson Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Johnson & Johnson's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 21.8% today to 23.1% in 3 years time.

- Analysts expect earnings to reach $26.9 billion (and earnings per share of $11.45) by about May 2029, up from $21.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $22.4 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 27.8x on those 2029 earnings, up from 26.4x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 15.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Loss of exclusivity for STELARA and the impact of biosimilar competition could significantly erode revenue from one of Johnson & Johnson's major products. This could affect overall revenue and net margins, especially in the innovative medicine segment.

- Tariffs, particularly those related to exports to China, could increase costs and impact the net margins negatively, due to increased cost of goods sold from tariffs being relieved through the P&L in future periods.

- The ongoing litigation related to talc, though controlled for now, poses a continual risk to financial stability and could impact net earnings and cash flow, particularly if adverse judgments or settlements occur.

- The orthopedics segment faced headwinds, including competitive pressures and challenges in the spine and sports areas. Ongoing issues could impact revenue and earnings unless the planned innovations drive a turnaround.

- Potential dilution from acquisitions such as Intra-Cellular Therapies and the impact of tariffs could affect operating margin improvement efforts, challenging overall earnings and net margins despite robust sales growth in some areas.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $252.96 for Johnson & Johnson based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $285.0, and the most bearish reporting a price target of just $155.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $116.5 billion, earnings will come to $26.9 billion, and it would be trading on a PE ratio of 27.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of $230.42, the analyst price target of $252.96 is 8.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Johnson & Johnson?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.